Fidelity International announces that, after five years leading Fidelity International as CEO, Anne Richards has decided to step down from her full-time executive role. She will remain with the company in the role of Vice Chair with an emphasis on helping the organisation with its key external relationships and strategic partnerships.

Anne will remain as CEO during a period of transition led by the Fidelity International Board that will take place over the coming months. Further details on succession will be communicated at a later date.

Commenting on Anne’s contribution to the business, Abby Johnson, Chair of Fidelity International said: “Over the last five years Anne has accomplished a tremendous amount for our organisation in service of our clients. She has spearheaded the build out of a wide range of new capabilities and services across multiple markets, as well as our firmwide approach to sustainability, setting us firmly on the path for the future. She made significant progress in building a more diverse and inclusive workplace, leading initiatives such as enhanced parental leave, carers leave and dynamic working, ensuring we are well placed to attract and retain the best talent in a post pandemic world.

“I look forward to working with her during this transition period and I am delighted she will stay with our business as Vice Chair, supporting us as we work together with our clients, employees and communities all around the world to build better financial futures.”

This year, we’re rerunning an article from last year’s STA Women in Finance newsletter on the importance of expressing gratitude in both professional and personal settings. On behalf of the STA WIF Committee, we wish you and your family a Happy Thanksgiving! – Inessa Ruffman, STA WIF Chair

For those of us in the U.S., on Thursday we will celebrate Thanksgiving. This is traditionally a day spent in the company of family and friends giving thanks and expressing sincere appreciation for the support and love we provide each other.

Yes, Thanksgiving is a wonderful day to be with those closest to us, but like all holidays it will come to an end and in the morning we will return to our daily routines, otherwise known as work: the place where we spend more hours with our colleagues in a week than we do with some aunts or uncles in a year.

“As we express our gratitude, we must never forget that the highest appreciation is not to utter words, but to live by them.” – John F. Kennedy

No matter what time zone we live in, our workday is long and filled with high stakes and critical decision making. We face an increasingly competitive landscape and unpredictable markets, yet our industry still provides much to be thankful for, beginning with the opportunity to forge meaningful and lasting relationships.

These relationships can be seen in many lenses: the client who becomes a close friend; the co-worker who feels like family and makes the day enjoyable; the mentor who gave a one-time pep talk over coffee or another who provided guidance over the course of a decade; the organization that allows us to network and build more relationships; and, the bosses and managers who support our careers every day.

But how often do we stop to show appreciation to all these people? And when we do, is the expression just an email or some other type of electronic communication?

John F. Kennedy said, “As we express our gratitude, we must never forget that the highest appreciation is not to utter words, but to live by them.” We should feel gratitude for being able to do what we enjoy and for those around us. But when we express gratitude, it should include an action on our part.

Beyond merely saying what you are grateful for, show it; live it. Be extra kind to your co-workers who bring you joy during the year. Mentor someone who could benefit from your experience and knowledge. Volunteer your time to the organizations that support your network. Give back in any way to this industry that gives us so much.

On behalf of the entire STA Board, STA Affiliates and the STA Women in Finance Committee, we wish you, your families and your colleagues, a safe and Happy Thanksgiving!

TECH TUESDAY is a weekly content series covering all aspects of capital markets technology. TECH TUESDAY is produced in collaboration with Nasdaq.

‘Tis the season – for workplace volunteering.

While Thanksgiving, Giving Tuesday and holiday toy drives are familiar end-of-year opportunities for companies and their employees to give back, corporate volunteerism is in fact on the rise year-round.

According to a recent survey by the Association of Corporate Citizenship Professionals (ACCP), 61% of firms reported that participation in employee volunteer activities increased in 2023. This growth is driven by companies offering a greater variety of options and time off to volunteer in groups, in person and individually.

Nasdaq enables employee volunteerism through its GoodWorks program, through which the company provides all full and part-time employees two paid days a year to volunteer in 2023. Along with the Nasdaq Foundation and Nasdaq Entrepreneurial Center, the GoodWorks program supports Nasdaq’s Purpose to “Advance Economic Progress for All.”

Jailan Griffiths, Nasdaq

“Volunteerism and community involvement are integral parts of Nasdaq’s Purpose, and through GoodWorks we’re giving our employees the opportunity to make a direct impact in the communities they live and work in,” Jailan Griffiths, Vice President and Global Head of Purpose at Nasdaq told Traders Magazine.

“Nasdaq GoodWorks provides a framework for finding, creating and leading volunteer projects,” said Raven Bolding, Corporate Purpose Specialist at Nasdaq, noting that the initiative’s volunteer week in April of this year drew more than 200 volunteers from 15 Nasdaq offices, to support more than 25 different organizations.

“Nasdaq has always been a purpose-driven organization. Initiatives like GoodWorks have enabled us to make it easier than ever for our employees to get involved – whether that’s through charitable giving, nonprofit board service, or even organizing office-wide opportunities for teams to volunteer in their communities.”

Raven Bolding, Nasdaq

As part of its mission, Nasdaq’s Purpose team recognizes employees who demonstrate exemplary commitment to service and have found unique ways to integrate Purpose into their work lives.

This year, Nasdaq has named six Purpose Champions from various regions, most recently Margareta Baxén, Executive Assistant at Nasdaq in Stockholm. Baxén’s engagement has included volunteering at the Ronald McDonald House in Huddinge, Sweden; organizing gift collections for underprivileged children; and engaging in community environmental cleanups.

“We want to ensure that all our employees have an opportunity to make a meaningful difference while supporting the causes that matter to them the most,” Griffiths added. “I want to give a special congratulations to all of Nasdaq’s Purpose Champions, who were recognized by their colleagues for going above and beyond in their efforts to advance Nasdaq’s Purpose.”

A Nasdaq Purpose volunteer event in Boston.

Other large and influential capital markets firms with volunteer initiatives include Morgan Stanley, whose employees have provided more than 2.8 million volunteer hours in June alone since establishing it as its Global Volunteer Month in 2006; BlackRock, whose Gives Network enables employees to work collectively to address needs of their communities via local nonprofits; and Virtu Financial, whose 10-year-old Give Back program has had employees clean up harbors in Los Angeles, run for charities in Hong Kong and donate blood in Melbourne.

“Employee giving and volunteerism programs increase engagement and tangibly align corporate values with those of employees,” ACCP President and CEO Carolyn Berkowitz said in a November 15 release. “In today’s highly competitive talent market, employee volunteerism and giving are essential strategies for recruiting, engaging and retaining staff. A recent IBM study showed that 70% of job seekers are more likely to apply for and accept an offer from socially responsible companies.”

Creating tomorrow’s markets today. Find out more about Nasdaq’s offerings to drive your business forward here.

(This article first published as Beyond Liquidity on Markets Media. Beyond Liquidity is produced in collaboration with Liquidnet.)

In December last year the Securities and Exchange Commission made four proposals to change US market structure. The proposals that were put out for comment included updating Rule 605 which covers data disclosure enhancements for all market participants; changing tick sizes and access fees; achieving best execution; and increasing competition for orders.

The Financial Markets Quality Conference, hosted by the Psaros Center for Financial Markets and Policy at Georgetown University, on 15 November included a panel discussion on these proposals.

James Angel, Georgetown University McDonough School of Business

Jim Angel, associate professor of finance at Georgetown University McDonough School of Business, said on the panel that the problem with the SEC’s proposed reforms is that nobody is looking at how they all go together. He added: “It’s really too much, too fast.”

Sapna Patel, head of Americas market structure & liquidity strategy at Morgan Stanley, agreed on the panel that the four SEC proposals are interconnected, and so they cannot be looked at in isolation.

“The question that I ask when you see a fundamental change, like the one contemplated, is what problem are we trying to solve because our markets are fairly efficient,” she added. “I think we should take a step back and be careful about breaking something that works for investors.”

Patel was working at the SEC during the last major changes to US market structure with the introduction of Reg NMS in 2005 when the regulator had been trying to solve the move from fractions to decimals, the rise of electronic trading and Nasdaq filing for exchange status. At that time the SEC engaged with the industry as it recognised its proposals were all interconnected. The regulator held a public hearing for the industry and then changed the proposed rules before gradually rolling them out.

“Today we have four individual proposals without any thought given to how they impact each other,” said Patel.

Hope Jarkowski, NYSE

Hope Jarkowski, general counsel at New York Stock Exchange, continued on the panel that there is broad support for Rule 605, which will add transparency, and the best execution rule but the other two proposals are controversial.

Jeffrey O’Connor, head of market structure, Americas, at Liquidnet, said in a report in October that there is an overabundance of negativity around the proposals, from all walks of the industry. He highlighted that during Gary Gensler’s time as chairman of the SEC, there have been 47 proposals versus 19 and 22 during the two previous administrations.

O’Connor said: “The current aggressiveness is leaving most market participants perplexed, citing lack of purpose or justification.”

Tick size reform

Jeff Davis, Nasdaq

Jeffrey Davis, senior deputy general counsel at Nasdaq, said on the panel that a consensus seems to be developing around tick size reform and allowing a half penny tick size, which Nasdaq has been advocating for a long time.

“We have continuously said it should be done in an incremental and careful way,” he added. “Our concern was that the proposal went too far and too fast.”

Patel agreed that allowing tick sizes below a penny addresses a market structure problem.

Davis continued that tick size reform is the only proposal that focuses on strengthening and deepening the NBBO (National Best Bid and Offer), which is critical for all aspects of market performance.

Volume tiered pricing

Another proposal that has generated controversy is banning exchanges from offering tiered pricing based on trading volumes for customer flow, although it would be allowed for proprietary flow.

Sapna Patel, Morgan Stanley

Patel said the SEC seems to believe that brokers are conflicted and routing to the exchanges in their own interest rather than their customers, and pocketing the money, and that smaller brokers and exchanges cannot compete. However, firms such as Morgan Stanley pass on fee rebates to their customers and smaller broker-dealers that are not able to be members of every venue use Morgan Stanley’s scale and connectivity for market access.

Davis argued that volume-based pricing is a universally accepted economic principle.

“It is rational economic behavior and one of our best tools for creating the NBBO by incentivizing market participants to display liquidity,” he added. “We are very concerned that we can’t compete on price with off-exchange venues.”

21st November 2023: Paris, France – Horizon Software (Horizon), a global leader in electronic trading solutions and algorithmic technology, today announces the launch of a new research paper orchestrated by Yadh Hafsi, supported by Horizon, titled: “Uncovering Market Disorder and Liquidity Trends Detection”. The paper introduces a cutting-edge methodology for detecting significant changes in liquidity within order-driven markets.

The primary goal of this research is to enhance the way we identify fluctuations in liquidity within financial markets. In essence, liquidity reflects how easy or difficult it is to buy or sell assets like stocks without causing significant price fluctuations. Recognizing when the market’s liquidity is changing is essential for traders, investors, and financial institutions.

Horizon Software has supported and helped Yadh in his research and are subsequently integrating his findings into their product offerings. The signals will be visible to end users during their trading decision and also integrated into Horizon’s algos to improve the executions. Horizon is discussing with clients and users on how best to leverage the research for their specific use cases, to further enhance the technology benefits afforded by adopting the methodology.

According to Olivier Masdebrieu, Chief Technology Officer, Horizon adds that:

“It is great to see this paper available to all and even better that Horizon was able to support Yadh Hafsi in his research, utilizing our platform ‘Horizon Extend’, a cross-asset electronic platform for principal and agency trading. We are excited to integrate these features, which will improve execution performance, and are very keen to present the usability of these findings to our global client bases. We’re looking forward to supporting the development of Yadh’s next paper, as part of our commitment to utilizing all avenues, academic and industry-based, to developing forward-thinking market insights to feed into our products.”

Yadh Hafsi, PhD Candidate at Université Paris-Saclay and Leader of the Research Project, comments:

“This paper contributes significantly to our understanding of liquidity dynamics in financial markets. My professors and my colleagues have been very helpful, and we will continue working on this domain in the next year.”

Sylvain Thieullent, CEO at Horizon Software says:

“Horizon Software is committed to pushing the boundaries of innovation in the financial technology sector. Our collaboration on this research paper reflects our dedication to providing cutting-edge solutions that empower market participants to navigate liquidity fluctuations with greater precision and confidence. By leveraging advanced methodologies, we aim to equip our clients with the tools they need to make informed decisions and thrive in dynamic market environments.”

About Horizon Software:

Horizon, a global leading vendor in Market Making, Agency Trading, and Algo Trading Technology, has empowered capital market players for over two decades by building powerful algorithmic technology into its electronic trading platform and offering trading opportunities through direct connectivity to more than 80 exchanges worldwide. Horizon, a B Corp certified company, enables clients to quickly create, test and implement automated trading strategies in real-time, in line with its ‘Trade Your Way” philosophy. Its platform can be easily integrated with rich APIs and allows proprietary strategies to be built while keeping traders’ code confidential.

By Greg Hotaling, Regulatory Content Manager, Confluence

Corporate lawyers and compliance personnel who update regulatory reports about their firms’ large holdings in American public companies – which is possibly the world’s least romantic endeavor – call it the “Valentine’s Day filing”. They are due to the SEC 45 days after the end of each calendar year: February 14th.

In a new Rule officially published last week, the SEC has taken aim at that deadline, and several other aspects of filings made by shareholders with stakes of at least 5%. In its first major changes to these disclosure requirements in decades, the SEC reaches into its regulatory quiver to target deadlines, security types, filing methods, group aggregation and more. For shareholding firms, it’s especially the stricter deadlines that will require them to act urgently across their compliance, operations and legal departments.

A uniquely complicated regime

Among the one hundred or so countries that impose “major shareholder” filing obligations, the American requirements are the most complex (as illustrated for example by the SEC’s legalistic term for such holdings, “beneficial ownership”). No other regime in the world establishes as many conditions affecting filing triggers, thresholds, deadlines and forms, as does the SEC.

On one hand, this can be helpful to shareholders on U.S. markets, enabling them to qualify for a shortened form (Schedule 13G rather than Schedule 13D) or forgiving deadlines (e.g. Valentine’s Day) in several different ways.

On the other hand, the numerous permutations for satisfying Regulation 13D-G require a learning curve for which many firms are ill equipped. For example, a Schedule 13D filer that experiences a “material change” in its beneficial ownership must file an amended 13D. According to the SEC a material change includes a 1% swing in ownership, but can also include changes in the shareholder’s funding sources, its purpose or other circumstances, which often require analysis by legal counsel. Moreover, the 13D amendment is due “promptly” according to current SEC rules. This can mean within one business day or up to 10 days, depending on the situation.

Eligibility for the shorter form, Schedule 13G, can also require legal analysis. Generally institutional investors (“QIIs”) qualify to submit a 13G, as long as they are passive investors. When first surpassing 5%, such investors may wait until the following year’s Valentine’s Day to file. Passive non-QIIs may use 13G as well, but they must file more immediately (within 10 days). For either purpose, defining a “passive investor” can be a legal question subject to interpretation. (As seen in a high-profile submission in 2022, when Elon Musk controversially announced his 9.2% stake in Twitter on Schedule 13G as a “passive investor”.)

The new requirements

The new SEC Rule’s “modernization” aspect is reflected in a new filing method and tighter deadlines, both of which the SEC justifies in part by citing investors’ access to modern technology. Under the changes, transmitting the disclosures will require “13D/G-specific XML”, it being a machine-readable, structured data language (unlike HTML and ASCII currently used for filings).

As for the deadlines, the SEC points out that among the initial 13D filings made in 2022, that were timely filed within the 10-day deadline, 41% of those were filed within just 5 business days. Hence the SEC’s logic for imposing a new, 5-business day deadline for 13D filings: shareholders can, and many already do, satisfy it without undue burden.

Some of the key deadlines being tightened:

Schedules 13D and 13D/A (amendment)

Form

Current deadline

New deadline

Schedule 13D (initially crossing 5%)

10 calendar days

5 business days

Schedule 13D/A (material change)

“Promptly”

2 business days

Schedules 13G and 13G/A (amendment)

Form

Current deadline

New deadline

Schedule 13G (initially crossing 5%), for QIIs and Exempt Investors

45 days after next calendar year

45 days after next calendar quarter

Schedule 13G (initially crossing 5%), for Passive Investors

10 calendar days

5 business days

Schedule 13G/A (material change)

45 days after next calendar year

45 days after next calendar quarter

Investors will welcome the clarity brought by certain of these changes, such as replacement of the “promptly” deadline with a more straightforward time limit of 2 business days. Meanwhile other deadlines, when surpassing a 10% stake, are being tightened as well. With respect to all of the deadlines, the SEC modified Regulation S-T, to change the “cut-off” time for filing on the relevant deadline dates from 5:30pm to 10:00pm U.S. Eastern time, providing some relief for filers.

The SEC also set forth new guidance, both on the inclusion of cash-settled derivatives under certain circumstances, and on shareholders acting together who thus may be deemed a “group”. Either of these assessments can significantly affect a firm’s total holdings amount for the purpose of triggering filings.

How firms should respond

The changes will require significant action by investment firms globally, across their compliance, operations and legal departments. The disclosure rules apply to shareholders wherever they may be based across the world, and complying with them requires an understanding of data and legal nuances relating to the interests held, corporate affiliations, investment discretion, and other characteristics of the shareholding entity.

The first order of business for firms is to mark out the key compliance dates:

SEC amendment

Compliance date

Filing deadlines – Schedule 13D

5 February 2024

Filing deadlines – Schedule 13G

30 September 2024

Structured data submission format

18 December 2024 (voluntary submissions start 18 Dec 2023)

Investment firms will need to examine and adjust their processes, both across their internal compliance and operations teams, and in lockstep with external counsel and any vendor support they receive such as post-trade monitoring systems. The shorter deadlines especially, of 2 and 5 business days, will leave little margin for delay or complacency here.

Meanwhile Valentine’s Day will lose some of its enamoredness, yielding its status as the annual date for eligible 13G filers, to take a lesser place as one of four quarterly filing deadlines. Firms will therefore need to translate their annual 13G-related workflows into quarterly processes.

The SEC also made it clear that 1% swings are “material”, for the purpose of needing to amend a 13D or 13G (in the current rules this is made explicit only for 13D amendments). Shareholding firms should adjust their systems accordingly, to ensure an alert is triggered for 1% swings in ownership for both 13D and 13G amendment purposes.

As for the SEC’s new guidance on derivatives and group consolidation, firms should draw on legal expertise to know exactly where they stand under the SEC’s approach. (They should likewise do so for the purpose of any “insider” disclosures they might be required to submit under Section 16 of the Exchange Act, which relies on the same definition of “beneficial ownership” for its filing trigger at 10%.) Operations and data personnel, as well as monitoring systems, will then need to ensure that any qualifying derivatives, and affiliated holdings within a “group”, are properly aggregated into the firm’s total “beneficial ownership” position for filing purposes.

By Hitesh Mittal, Founder & CEO, and Koushik Ganesan, Quantitative Analyst, BestEx Research

Higher participation rates in trading can indeed lead to greater market impact, but there are circumstances when trading at higher participation rates is justified. For example:

Hitesh Mittal

● In cases where investor redemptions result in larger trades

● When portfolio managers have strong convictions about a trade

● When the appetite for execution risk is low and a longer execution horizon is not feasible

● Trading small-cap stocks, where trading a high percentage of average daily volume is not necessarily equivalent to the same behavior in a large cap stock

While traders often have an intuitive sense of suitable participation rates for specific stocks and trade durations, such judgments can be somewhat arbitrary because they lack data-driven, empirical support. Interestingly, the SEC has proposed a rule (press release here) suggesting a predefined participation rate for mutual fund managers–irrespective of a stock’s market capitalization–in defining what constitutes a liquid or illiquid investment. The proposed rule updates the concept of “Reasonably Anticipated Trade Size” (commonly referred to as “RATS”) to classify investments as liquid or illiquid in a much more restrictive fashion. The proposal sets a fixed “value impact” threshold at 20% of the average daily volume for exchange-listed stocks, suggesting that trading any larger portion of daily volume would have a significant impact on the price of the stock. But a fixed, participation-based threshold for impact could have significant implications for mutual fund managers, particularly those with investments in small-cap securities.

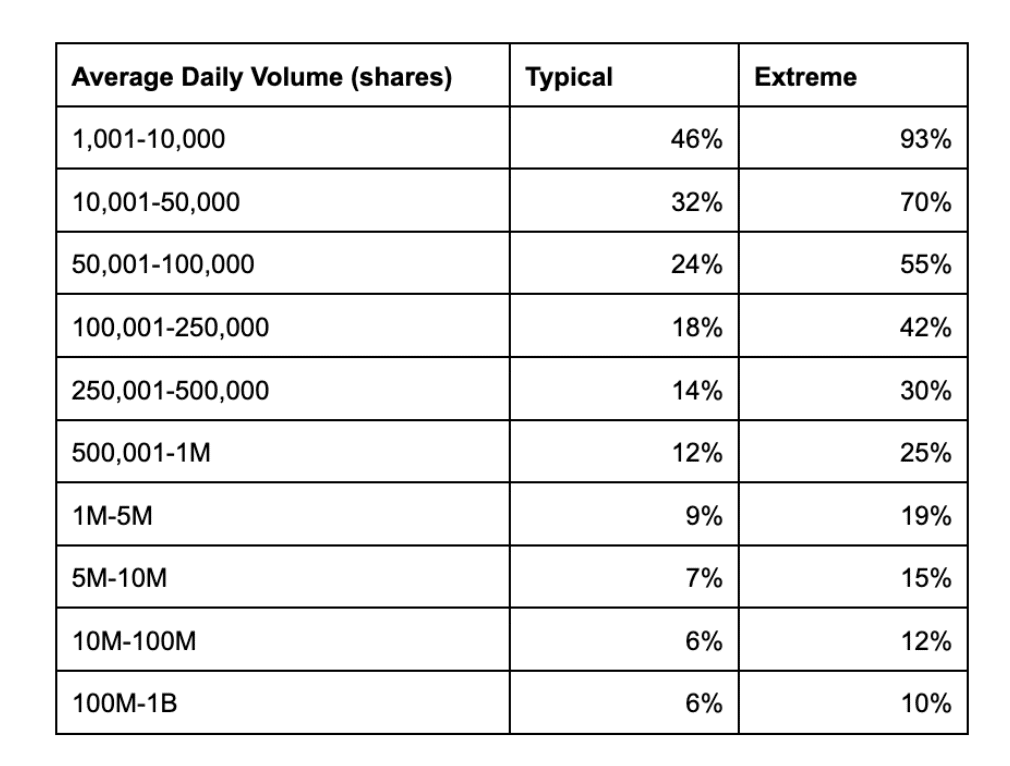

We propose an empirical approach using trade and quote data to determine appropriate participation rates based on what is commonly encountered in the market. To this end, we analyze aggregate buy-sell imbalances relative to trading volume (percent of volume) based on a quarter of trade and quote data. To calculate the buy-sell imbalance, we employ the Lee-Ready algorithm, assigning buy or sell indicators to trades based on their positioning around the midpoint of the bid and ask prices. The difference between buy and sell volumes provides the net trade imbalance for each period. We conduct this analysis for each trading day across all stocks in our dataset, observing both the median (referred to as “typical”) and the 95th percentile (referred to as “extreme”) of trade imbalance as a percent of volume.

The table below illustrates our findings for orders executed over a full trading day, categorized by varying levels of average daily volume.

Source: BestEx Research

Our analysis reveals that “extreme” imbalances are significantly higher for less liquid stocks, implying that less liquid stocks can accommodate a much higher percentage of average daily volume in terms of trade impact. For example, for a stock with an average daily volume of 100,000 shares per day, a 24% trade imbalance as a percent of average daily volume is typical, and 55% of average daily volume is extreme, in clear contrast with the most liquid category where 6% is typical and 10% is extreme.

This analysis suggests that the SEC should reconsider the proposed value impact threshold for mutual fund managers, as the percentage of average daily volume appropriately labeled “high impact” should be higher for less liquid stocks and lower for more liquid ones.

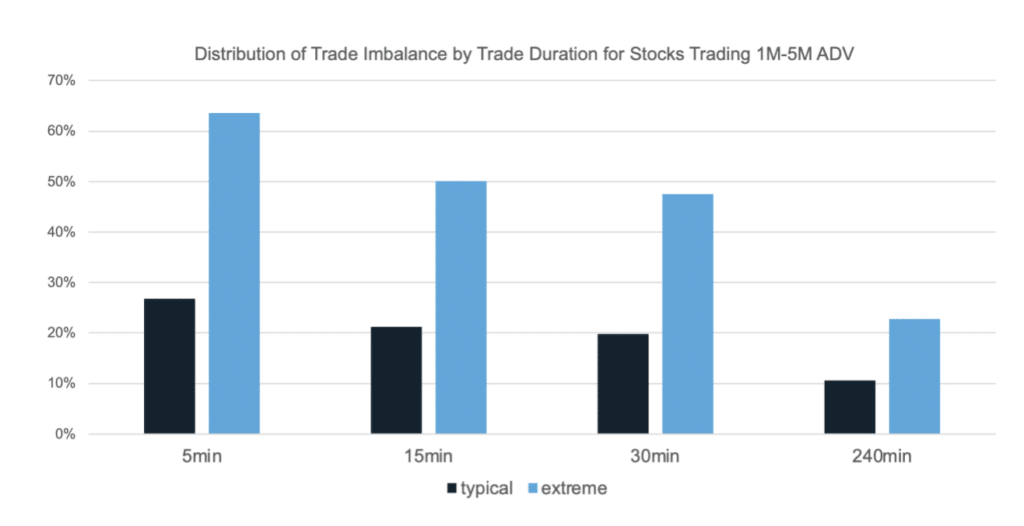

Moreover, we conducted this analysis for various trade durations, which has implications for how traders choose the speed of execution in urgent situations. Notably, both “typical” and “extreme” values can be substantially higher for shorter trade durations, aligning with market dynamics; markets tend to recover from temporary imbalances. The below image illustrates the set of typical and extreme values for stocks that typically trade between 1 million shares to 5 million shares per day. For example, for stocks with these liquidity characteristics, an imbalance of 11% is typical over a duration of 4 hours, while a typical imbalance for a duration of 5 minutes is much higher, at 27%. Extreme values are similarly disparate, with extreme imbalances over a 4-hour duration at 23% while 5-minute imbalances can be 64% at the extreme.

Source: BestEx Research

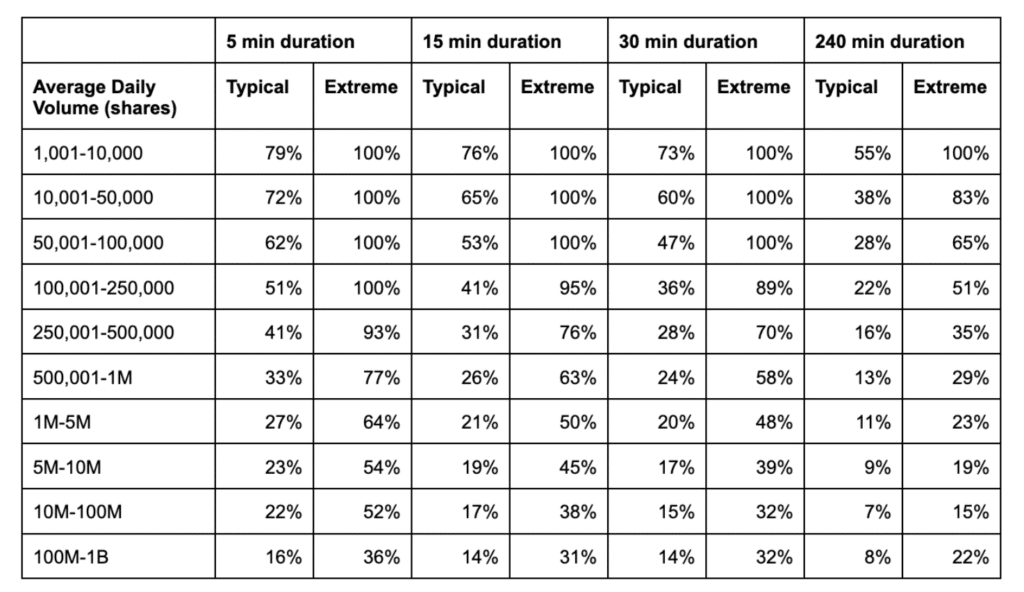

Details of imbalance distributions for all daily volume classifications can be found in the appendix.

It is important to note that the characteristics observed here aren’t exclusive to equities trading; similar principles apply to other markets, such as the futures market. We recently published a brief article on futures markets, reaching similar conclusions.

In summary, our data-driven approach provides insights into determining appropriate participation rates under varying conditions, offering potential guidance for regulatory decisions and helping traders determine participation rates based on order characteristics.

APPENDIX

The table below contains the typical and extreme imbalances for all average daily volume groupings based on the analysis described above.

Neptune Networks, a fixed income network for disseminating real-time axe data, has announced senior management changes at the firm. Following agreement by the Board, John Robinson will move to the role of Executive Chairman and Byron Cooper-Fogarty will become CEO on April 1, 2024. Robinson is currently CEO of Neptune, having joined the firm in November 2020. Current Neptune COO, Cooper-Fogarty has been at Neptune for seven years, and previously held the role of Interim CEO in 2020.

Francis Verpoucke

Mirova US has hired Stéphane Detobel and Francis Verpoucke, two highly recognized business professionals in the North American region. Having worked as a duo for over two decades, first at Amundi in Europe and North America for 12 years and more recently at TOBAM as both Managing Directors North America, Detobel and Verpoucke will initially promote Mirova’s global equity, global fixed income, energy transition infrastructure and private equity strategies. In the future, Mirova intends to open its natural capital expertise to North American investors as well.

Lisa Balter Saacks

Trillium Surveyor, a provider of post-trade surveillance and best execution software, has appointed Lisa Balter Saacks as President. Saacks joins the Trillium Surveyor team with a wealth of B2B, SaaS, and fintech expertise. Over the past 20 years, Saacks has held multiple sales and management roles in which she successfully built and executed on aggressive business growth plans. Prior to joining Trillium Surveyor, she was a Managing Director at Winning by Design, a B2B SaaS consulting firm, where she helped high-growth and Fortune 500 companies design, build, and scale their B2B revenue organizations.

The Financial Technology Association (FTA) has made Tom Manatos, Head of Federal Affairs at Block, as Chair of FTA’s Board of Directors. He brings over a decade of experience in government affairs and trade associations to his role as Board Chair, including previous positions as Vice President of Government Relations at Spotify and Vice President of Federal Government Affairs at the Internet Association.

BlueFlame AI, a generative AI platform for alternative investment managers, announced it has expanded its executive team with four strategic senior hires, including Justin Guthrie as Chief Financial & Strategy Officer, James Tedman as Head of Europe and Head of Information Security, Michael Donnelly as Head of Client Success and Mauri Lowery as Director of Executive Operations.

If you have a new job or promotion to report, let me know at alyudvig@marketsmedia.com

The Securities and Exchange Commission (SEC) has adopted new rules to improve the governance of all registered clearing agencies by reducing the likelihood that conflicts of interest may influence their boards of directors or equivalent governing bodies.

“I am pleased to support this adoption because it helps foster more resilient clearinghouses,” said SEC Chair Gary Gensler.

Gary Gensler, SEC

“Congress has said that the Commission has an important role relating to clearinghouses. This adoption seeks to enhance standards to achieve several goals: promote board independence, consider the views of relevant stakeholders, and reduce the potential for conflicts of interest with respect to the board and senior management. Taken together, these final rules benefit investors, issuers, and the markets connecting them.”

The new rules establish governance requirements regarding board composition, independent directors, nominating committees, and risk management committees.

The rules also require new policies and procedures regarding conflicts of interest, management of risks from relationships with service providers for core services, and a board obligation to consider stakeholder viewpoints.

The rules are being adopted pursuant to, among other statutory provisions, Section 765 of the Dodd-Frank Act, which specifically directs the Commission to adopt rules to mitigate conflicts of interest for security-based swap clearing agencies.

The rules improve the governance of registered clearing agencies by identifying certain responsibilities of the board, increasing transparency into board governance, and, more generally, improving the alignment of incentives among owners and participants of a registered clearing agency.

In support of these objectives, the rules establish new requirements for board and committee composition, independent directors, management of conflicts of interest, and board oversight.

The adopting release has been published on SEC.gov and will be published in the Federal Register. The compliance date is 12 months after publication in the Federal Register, except for the independence requirements for the board and board committees, for which the compliance date is 24 months after publication in the Federal Register.

FLASH FRIDAY is a weekly content series looking at the past, present and future of capital markets trading and technology. FLASH FRIDAY is sponsored by Instinet, a Nomura company.

It seems some of the hottest early-2020s trends in the institutional brokerage space have cooled.

SIFMA recently released its Annual Meeting Debrief, 2023, and there were some notable changes in what’s most prominent on brokers’ radar, versus just one year earlier.

The report starts at a high-level and works its way down into specific topics. The first question SIFMA asked hundreds of participants at its Nov. 6-7 meeting in Washington, D.C. was: What industry topics are top of mind for you?

The leading response, at a robust 76.7%, was “totality of the SEC agenda.” This was followed by “Cyber readiness” at 62.8%, “Transition to T+1 settlement” at 46.5%, and “Equity market structure reform” at 37.2%.

It’s notable that the top four topics are defensive in nature, i.e. they require brokers to allocate time, money and resources to comply with new regulations or to bolster cybersecurity.

The top-of-mind list looks quite different from the Annual Meeting Debrief, 2022, in which “Digital assets/cryptocurrencies” and “Equity market structure” were tied for 1st at 44.8%, followed by “ESG/Sustainable finance”, “Transition to T+1 settlement”, and “US Treasury market structure reform” in a three-way tie for 3rd at 41.4%. Next was “Cyber readiness” at 37.9% and “Decentralized finance (De-Fi)” at 34.5%.

So while regulation and cybersecurity were prominent in 2022, three of the top seven topics – digital/crypto, ESG/sustainable, and De-Fi – could be viewed as playing offense, in that they are opportunities for brokers to grow business and expand into new markets.

This year, digital/crypto fell from 1st to 5th, dropping 10 percentage points to 34.9% top of mind; ESG/ sustainable fell from T-3rd to 8th, dropping more than 20 percentage points to 20.9%; and DeFi fell from 7th to 12th, dropping 23 percentage points to 11.6%.

It seems there are two main takeaways from the top-of-mind changes: one, perhaps there’s less allure to new opportunities in digital assets, crypto, ESG, sustainable finance, and de-fi than there was a year ago; and two, exogenous forces (SEC, hackers) are forcing brokers to play defense.

Regardless of the shift in broker priorities, as well as ongoing economic uncertainty, there remains a backdrop for growth. The 2023 SIFMA report assessed the state of the industry as follows:

“As to how capital markets firms are weathering the challenging and ever-changing environment, one speaker noted the importance of diversification. He compared businesses to pistons on a car – corporate debt may go down while equity capital markets go up. That said, ‘stocks are going to trade, and bonds are going to trade’, regardless of the environment. Markets remain active, even as some capital markets businesses ‘peaked out’ in 2021.”

Giving Thanks for Relationships: A Thanksgiving Reminder

– Inessa Ruffman, STA WIF Chair

For those of us in the U.S., on Thursday we will celebrate Thanksgiving. This is traditionally a day spent in the company of family and friends giving thanks and expressing sincere appreciation for the support and love we provide each other.

Yes, Thanksgiving is a wonderful day to be with those closest to us, but like all holidays it will come to an end and in the morning we will return to our daily routines, otherwise known as work: the place where we spend more hours with our colleagues in a week than we do with some aunts or uncles in a year.

“As we express our gratitude, we must never forget that the highest appreciation is not to utter words, but to live by them.” – John F. Kennedy

No matter what time zone we live in, our workday is long and filled with high stakes and critical decision making. We face an increasingly competitive landscape and unpredictable markets, yet our industry still provides much to be thankful for, beginning with the opportunity to forge meaningful and lasting relationships.

These relationships can be seen in many lenses: the client who becomes a close friend; the co-worker who feels like family and makes the day enjoyable; the mentor who gave a one-time pep talk over coffee or another who provided guidance over the course of a decade; the organization that allows us to network and build more relationships; and, the bosses and managers who support our careers every day.

But how often do we stop to show appreciation to all these people? And when we do, is the expression just an email or some other type of electronic communication?

John F. Kennedy said, “As we express our gratitude, we must never forget that the highest appreciation is not to utter words, but to live by them.” We should feel gratitude for being able to do what we enjoy and for those around us. But when we express gratitude, it should include an action on our part.

Beyond merely saying what you are grateful for, show it; live it. Be extra kind to your co-workers who bring you joy during the year. Mentor someone who could benefit from your experience and knowledge. Volunteer your time to the organizations that support your network. Give back in any way to this industry that gives us so much.

On behalf of the entire STA Board, STA Affiliates and the STA Women in Finance Committee, we wish you, your families and your colleagues, a safe and Happy Thanksgiving!