As financial institutions approach the T+1 settlement change, determining the right affirmations model will be critical in getting the most out of the new deadline, according to Derek Coyle, European Custody Product Manager at Brown Brothers Harriman.

Derek Coyle

When it comes to how trades can be affirmed, there are two main options to consider, Coyle said: 1) the custodian supported confirm matching model and 2) direct affirmations, also known as self-affirmations.

He explained that for confirm matching, custodians will align the trade instructions against the broker-dealer confirmations to complete the affirmation steps ahead of the DTCC deadlines on Trade Date.

“The result of the affirmation is then communicated to Trade Suite and the trade becomes eligible to settle as an affirmed transaction,” he said.

Coyle added that Confirm Matching means that the custodian will be responsible for completing.

“Depending on the custodian, they can have a slightly earlier instruction deadline (ahead of the DTCC 9PM EST affirmation deadline) to give some buffer in case of any operational support being needed,” he said.

With Direct Affirmations, firms can choose to perform the matching steps themselves by aligning their instructions against the broker-dealers confirmation, Coyle said.

The affirmation is then completed in the DTCC systems, after which the custodian will receive the result of the affirmation that can act as a trade instruction for the custodian or be matched to a secondary trade instruction sent via standard means form the client to the custodian for further processing and settlement in the market, he said.

According to Coyle, direct affirmations can provide more control over the affirmation process, which can be “beneficial where firms have end-to-end oversight over reconciliations and so on”.

“Direct affirmations also give direct access to the visibility and reporting of successful affirmation and related timestamps,” he said, adding that this can be valuable for those Registered Investment Advisors (RIAs) who need to provide affirmation timestamp reporting.

Coyle told Traders Magazine that Registered Investment Advisor (RIA) firms with regulatory oversight from the SEC will need to be prepared to provide evidence of their activity in successful affirmations, with date and timestamp records of instruction activity needed to show efforts at meeting the DTCC 9PM EST affirmation deadlines on Trade Date.

He noted that the reporting requirements do not differ between the direct affirmation and custodian supported affirmation models – both require the date and timestamps to show actions taken and the responsibility to comply with the requirement under both models will remain with the RIA.

According to Coyle, timestamps showing date and time of the trade execution steps (allocation, confirmation and affirmation) leading to successful settlement are required.

“Firms can maintain this internally or ask a third party to support the recordkeeping requirement,” he said.

DTCC are also preparing a Trade Archival tool, which can be used to source SEC required timestamps, he added.

Coyle stressed that having a Tradesuite ID (TSID) in place to correctly be identified as a trading party is key.

“DTCC have been supporting requests to provide such IDs in the past weeks and months,” he said.

“After that – the main focus would be on adjusting the timing of trade instructions to be completed before 9PM EST on Trade Date, and then engaging with counterparties to understand their alignment to be ready to affirm and settle with you according to the new requirements from the end of May,” he said.

ACS Holdings/Global Liquidity Partners has formally announced the successful acquisition of Coda Markets Inc., an agency broker-dealer specializing in proprietary routing technology and auction market platforms.

With an esteemed team and a diverse client base, Coda has firmly established itself as a leader in its sector.

The acquisition brings with it new opportunities for growth and collaboration.

“We are confident that by combining Coda’s competencies with ACS Execution Services’ robust algorithmic capabilities and Comhar Capital Markets’ (COHR) market-making expertise we can further enhance the services available to our clients,” said Peter Cocuzza, Business Development – Client Relationships at ACS Execution Services – Global Liquidity Partners.

“At Global Liquidity Partners, we take great pride in our unique ability to provide solutions spanning a wide spectrum of equity execution, and this latest addition further enhances our capacity to address our clients’ needs.Coda will continue to operate as an independent company under ACS Holdings/Global Liquidity Partners,” he added.

About Coda Markets

Coda Markets is an agency broker-dealer specializing in proprietary routing technology and auction market platforms. Coda operates an innovative auction based alternative trading system (ATS) and smart order router that aims to optimize liquidity aggregation for all market participants. Additionally, Coda builds and deploys customized routing strategies to meet the needs and demands of subscribers and traders.

About ACS Global Holdings

ACS Global Holdings wholly owns ACS Execution Services, Comhar Capital Markets, and Global Liquidity Partners. ACS Execution Services is a FINRA regulated broker-dealer that provides execution services to other broker-dealers in U.S. listed equities. Their focus is on the algorithmic-based execution of larger, not-held orders where the client desires performance related to a common metric such as Arrival Price, VWAP, PWP, or custom logic. Comhar Capital Markets is a FINRA regulated broker-dealer that conducts business as a registered market-maker providing liquidity exclusively to other broker-dealers, with a focus on fulfilling IOC order flow. Global Liquidity Partners is a technology company that provides trading systems and support to its broker-dealer affiliates through the use of internally developed proprietary software.

James Kostulias, Head of Trading Services at Charles Schwab, speaks with Traders Magazine about the firm’s trading capabilities, challenges for retail brokers and the evolution of trading technology.

James Kostulias

Please tell us about Charles Schwab and its trading desk. What are your average daily trading volumes?

Schwab has an incredibly active and lively trading desk, and each day we facilitate about 6 million trades. Over the past few years we’ve seen – as has the whole industry – a tremendous growth in retail trading, particularly spurred by the flood of entrants who gravitated to the markets during the Covid-19 pandemic, and that has really changed the game.

What trading capabilities do you offer?

With Schwab, clients can trade stocks and ETFs, options (index and equity) futures, and forex. They can also invest in bonds and fixed income products, money market funds, mutual funds, index funds, international equities, and gain indirect access to cryptocurrency via related funds, crypto coin trusts, stocks, futures and spot Bitcoin ETFs.

Schwab offers its trading experience under the brand “Schwab Trading Powered by Ameritrade™,” which reflects its unique heritage. Schwab announced its intention to purchase Ameritrade in 2019, and we’ve spent the better part of the last four years combining the best of the Schwab and Ameritrade to create something exceptional. With Schwab Trading Powered by Ameritrade, we’ve tied together the award-winning thinkorswim trading platforms with Schwab’s trading capabilities on Schwab.com and Schwab Mobile, alongside extensive trading education and specialized service.

What retail trading trends/themes do you see?

Right now, we’re seeing strong retail engagement with the markets; as of our Q1 ’24 earnings, trading volumes and margin balances were up 15% and 9%, respectively, from the previous quarter.

One way we keep a pulse on retail trading trends is through our monthly Schwab Trading Activity Index™, or STAX, report. What sets the STAX apart from other indicators is that it’s based on behavior; each month, we analyze retail investor portfolios and trading activity from Schwab’s millions of client accounts to illuminate what investors were actually doing and how they were positioned in the markets. From that analysis, we come up with a score for the month, and the up-or-down movement in that behavioral score serves as a gauge for retail investor sentiment.

For example, in our April STAX report, the score fell into the moderate-low range compared to historical averages. Schwab clients net bought equities, but they were discerning with the names they bought, gravitating towards companies with strong fundamentals and especially those with compelling generative AI solutions. AI-related names continue to rank near the top of our client buy lists.

Finally, a trend that we’ve seen (as has the industry in general) over the past few years is the rise in derivatives among retail traders. People turn to derivatives for a number of reasons – increasing leverage, controlling their risk, etc. But derivatives can also be an avenue for providing strategic exposure, particularly for accounts that can benefit from the capital efficiency these products offer. Because derivatives come with unique risks, we have made them a significant area of focus within our education offer. Between the improvements in platforms and education that surround options, there’s never been more to support the retail trader.

What are the current challenges for retail brokers?

We all live in the information age, and the impact of the internet and social media on our daily lives can’t be over-stated. The same can be said for investing. But while there’s a glut of information and guidance out there when it comes to investing and the financial markets, it’s not all created equal, and finding trustworthy information from expert sources has never been more important.

So, for brokers, it’s critical for us and for the financial well-being of our clients that we serve that role and help investors cut through the noise. I am immensely proud of Schwab’s education offer, which is beyond extensive. In addition to exclusive market commentary from our experts at the Schwab Center for Financial Research (SCFR), we offer a wide array of articles, videos, client-exclusive courses and learning pathways, coaching, live and virtual events, podcasts, email newsletters and even the Schwab Network, our media affiliate offering broadcast market commentary, analysis, and insights from industry professionals.

This rich education ecosystem empowers our clients to learn about the topics they want to know more about, in the ways and via the channels that suit them best.

What is your view on the evolution of trading technology and the impact of AI? / How does your team adapt to new technologies?

AI is something we are keeping a careful eye on. There are various ways AI may be useful for our clients and we are already doing some testing-and-learning to see what might be possible.

For example, AI may be able to help answer questions like: How can we enable our front-line associates to serve clients faster? Or better yet, how can we answer clients’ questions proactively, so they don’t have to call in at all? The answers would be informed by factors like current market activity or real-time insights into what are clients calling in about. Armed with that kind of knowledge, we could probably serve up relevant content within the hour.

Another example is education. Based on what we see clients searching for or trading, we can eventually help guide clients to the best next steps in their investing by serving up educational resources on trading strategies or by making service recommendations.

But the benefit of these projects won’t just be the content we serve up, the revolutionary piece will be the speed of delivery – how quickly can we serve up relevant information that leads to insightful trade ideas. For example, most market commentary happens ahead of the market of after, can we identify trends during the day? That’s the kind of thing that will make a big difference for our clients when the time comes.

What is you view on the electronification of the markets? / What trends do you see emerging or advancing?

The more we can democratize investing and educate investors to take control of their financial futures, the better, and electronification plays a big role in that. It is better for our clients – and better for the marketplace – when there are more participants.

We’re seeing younger participants in the market these days, which is a great thing. Trading and market education is becoming much more common in universities. It’s also easier to open and fund an account than ever before. All of this is helping younger folks learn their way into participating in the market, where more learning and education awaits them.

With the evolution of technology, market structure, and pricing I fully believe there has never been a better time to be an individual trader and/or investor.

What automation themes are you seeing, and what could drive more electronic trading?

At Schwab, we offer our Trader API, which allows developers to access market data and trade electronically without having to engage with the thinkorswim application every day. We love thinkorswim and feel it’s the best platform out there for traders, but we’re big supporters of choice. And we know it takes time to log in everyday, load a trade ticket, click send etc. Schwab’s Trader API allows clients to back-test strategies, set their own alerts, and execute trades based on the signals they identify as meaningful. We also offer a Schwab Developer Portal that anyone can sign up for.

Looking ahead to the future of electronic trading, the developments of your teams and how they look to enhance their skill sets. What work is being done to prepare the trading desk of the future from a sell-side perspective?

Our guiding principle is “through clients’ eyes,” which means we always frame our thinking around what the client needs, what will they need to grow their investments and how they can protect them. We are focused on adding capabilities to our apps without disrupting their current experience. We are looking to simplify processes, reduce the noise, and serve up information faster in a way that any investor or trader, from novice to expert, can consume. With the largest brokerage firm integration in history nearly behind us, we on the Trading Services side of the business are focused on innovating for clients in ways that reflect traders’ needs – which are far from one-dimensional. Traders are investors, too. They also engage in long-term investing with things like managed accounts and 401Ks. We want to serve the whole client, ALL their needs.

Is there anything else you would like to add?

In many ways, there’s never been a better time to be a retail trader. With the array of access, education, tools, ease, and low or eliminated barriers to entry that shape the trading experience now, we’ve come such a long way since I began my career two decades ago. Schwab was founded around the philosophy of creating greater access to investing and trading, so it’s exciting to see where we are today.

And you can expect Schwab to continue to be a leader in the trading space, especially coming out of the historic integration with Ameritrade and our ability to deliver the best features and functionality from both the Schwab and Ameritrade platforms to meet the needs of all kinds of traders, from very experienced and sophisticated to those just starting out.

It is tricky to think of another industry where speed and accuracy are of such paramount importance. It is, therefore, even harder to work out why the banking sector is still so reliant on slow, antiquated processes when it comes to payment reconciliations.

Next month marks five decades since midsized German bank Herstatt experienced a sudden collapse due to its involvement in risky FX speculation. The bank had received payments in various currencies from counterparties in different time zones, only to then fail to make corresponding payments in other currencies before it was closed down by rule makers.

The trouble is, fifty years on, the banking sector has ballooned in terms of its importance to the global economy. Many estimates place the banking sector at around 20-25% of the world economy (source: Research and Markets – Financial Services Global Market Report 2021: COVID-19 Impact and Recovery to 2030). Therefore, when stresses to the system emerge, the knock-on effects can be severe. When a globally systemically important bank like Credit Suisse is identified as facing liquidity challenges, as was the case last year, the prevalent use of outdated post-trade processes across capital markets, such as reconciling payments one or more days after settlement, can have serious ramifications. This means, if a full-blown crisis emerges, counterparties can’t determine how exposed they are, because they lack the critical information needed to identify which payments have been sent and received so far that day. A situation, like what happened to Credit Suisse and has also happened to smaller institutions, underscores the urgency for a significant shift towards real-time payment reconciliation systems. Failure to act doesn’t only jeopardise individual firms, but can also propagate systemic risk, leading to catastrophic consequences reminiscent of past financial crises.

When market speculation mounts into tangible threats of liquidity crunches, financial institutions naturally resort to safeguarding their interests. Payment controls are instituted to mitigate settlement risks, albeit in a fragmented and, in some cases, manual manner. This decentralised approach, often controlled at the individual business level, fosters inconsistencies, and could potentially introduce loopholes for errors, posing financial, operational, liquidity and reputational risks. Moreover, a lack of oversight could trigger future systemic instability, amplifying the gravity of the situation.

Central to the issue is the timeliness and accuracy of payment reconciliations. The existing practice of initiating the reconciliation processes only at the very end of each day (once the US dollar market is closed), leaves institutions operating in the dark regarding their exposure. This delay, while seemingly innocuous, can have dire implications – particularly in times of financial stress. The inability to ascertain real-time payment status not only undermines confidence but also perpetuates a cycle of uncertainty, compounding the risks for all parties involved. In certain scenarios, banks may hold all outgoing payments using their manual and fragmented controls. However, the dilemma lies in discerning which payments they’ve received from the counterparty throughout the day, hindering their ability to release funds appropriately. Without real-time reconciliation, firms may understandably take a cautionary approach and withhold outbound payments to the at-risk counterparty until reconciliation (generally delayed by at least a day, as outlined above) confirms which ones are safe to proceed with.

In addressing this pressing, and frankly longstanding, concern, the imperative is clear: real-time payment insight is non-negotiable. The convergence of business, risk, treasury, and operations necessitates a seamless flow of information, devoid of manual interventions and time lags. By embracing automated, real-time reconciliation processes, institutions can empower decision-makers with the information needed to navigate turbulent waters confidently.

Imagine a scenario where payment reconciliations occur seamlessly and continuously throughout the day. Armed with real-time information, institutions can accurately assess their exposure and make informed decisions regarding the release of outbound payments. This proactive approach not only averts potential defaults but also fosters market stability by honouring commitments and mitigating systemic risks. However, achieving this transformation requires a departure from complacency. The notion of ‘if it isn’t broke, don’t fix it’ is no longer tenable in a fast-moving and inter-connected banking world marred by uncertainties. Financial institutions must acknowledge the inherent flaws in outdated processes and embrace technological advancements to stay ahead of the curve.

Ultimately, the need for real-time payment reconciliations transcends mere operational efficiency — it is a matter of systemic and regulatory resilience. By prioritising the adoption of automated, real-time reconciliation systems, financial institutions can fulfil their obligations, mitigate risks, and contribute to a more stable and orderly market. The time for action is now; the stakes are too high to delay.

Xceptor has announced the availability of the Xceptor Data Automation Platform for financial markets in the Microsoft Azure Marketplace, an online store providing applications and services for use on Azure.

Dan Reid

“The collaboration with Microsoft to make the Xceptor platform available on the Azure Marketplace brings us closer to our clients as well as organizations who seek convenient, accessible tools to manage their intricate data management and automation needs. This simplifies the purchasing process and expedites onboarding, thereby allowing clients to focus on what matters and realize benefits quickly,” said Dan Reid, Chief Technology Officer, Xceptor.

Xceptor customers can now take advantage of the productive and trusted Azure cloud platform, with streamlined deployment and management.

With a focus on flexibility and customization, Xceptor offers its clients and prospects the option to either select pre-packaged solutions or collaborate on tailored options.

Chosen solutions are then seamlessly integrated by Xceptor.

Following integration, Xceptor’s swift onboarding process kicks in, promising a quick return on investment for clients who need their data to be ingested, standardized, normalized, and validated before it becomes trusted and ready for workflows.

“Through Microsoft Azure Marketplace, customers around the world can easily find, buy, and deploy partner solutions they can trust, all certified and optimized to run on Azure,” said Jake Zborowski, General Manager, Microsoft Azure Platform at Microsoft Corp. “We’re happy to welcome the Xceptor platform to the growing Azure Marketplace ecosystem.”

The Azure Marketplace is an online market for buying and selling cloud solutions certified to run on Azure. The Azure Marketplace helps connect companies seeking innovative, cloud-based solutions with partners who have developed solutions that are ready to use.

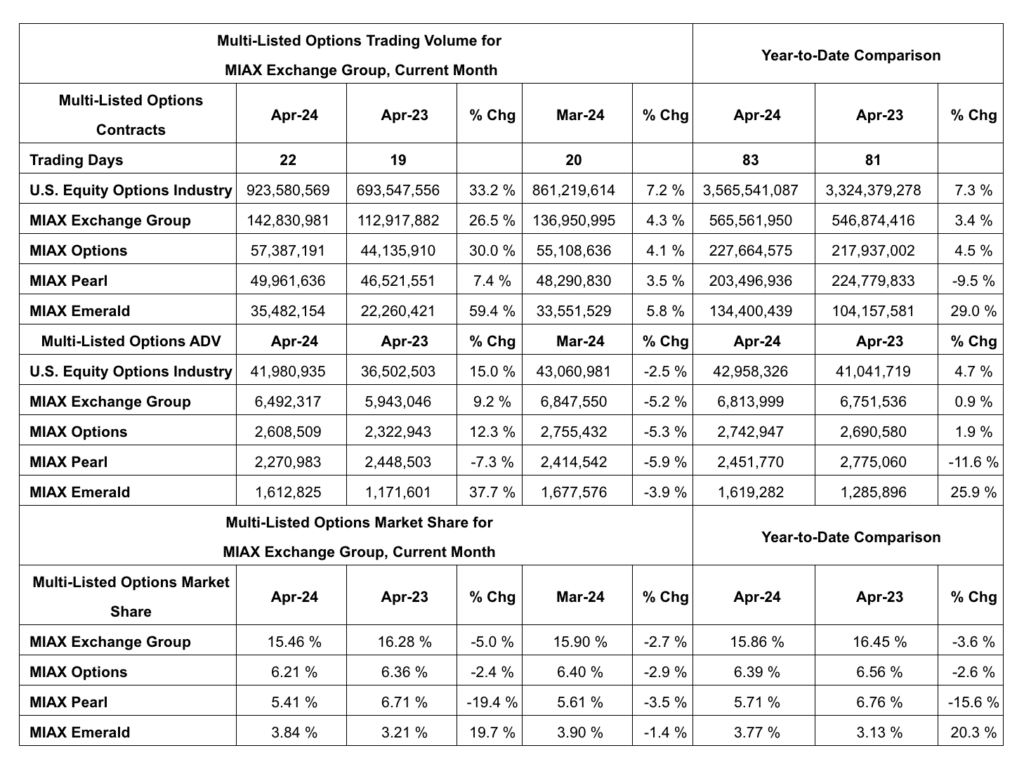

PRINCETON, N.J., May 8, 2024 /PRNewswire/ — Miami International Holdings, Inc. (MIH), a technology-driven leader in building and operating regulated financial markets across multiple asset classes and geographies, today reported April 2024 trading results for its U.S. exchange subsidiaries – MIAX®, MIAX Pearl® and MIAX Emerald® (together, the MIAX Exchange Group), and Minneapolis Grain Exchange (MGEX™).

April 2024 and Year-to-Date Trading Volume and Market Share Highlights

Total multi-listed options volume for the MIAX Exchange Group reached a monthly total of 142.8 million contracts, a 26.5% increase year-over-year (YoY) and representing an increase of 4.3% from March 2024. Average daily volume (ADV) reached 6.5 million contracts, a 9.2% increase YoY. April 2024 market share reached 15.5%, a 5.0% decrease YoY. Total year-to-date (YTD) volume reached a record 565.6 million contracts, a 3.4% increase from the same period in 2023.

MIAX Options reached a monthly volume of 57.4 million contracts, a 30.0% increase YoY and representing a monthly ADV of 2.6 million contracts, a 12.3% increase YoY. Total YTD volume reached a record 227.7 million contracts, a 4.5% increase from the same period in 2023.

MIAX Pearl Options reached a monthly volume of 50.0 million contracts, a 7.4% increase YoY and representing a monthly ADV of 2.3 million contracts, a 7.3% decrease YoY. April 2024 market share reached 5.4%, a 19.4% decrease YoY. Total YTD volume reached 203.5 million contracts, a 9.5% decrease from the same period in 2023.

MIAX Emerald Options reached a monthly volume of 35.5 million contracts, a 59.4% increase YoY and representing a monthly ADV of 1.6 million contracts, a 37.7% increase YoY. April 2024 market share reached 3.8%, a 19.7% increase YoY. Total YTD volume reached a record 134.4 million contracts, a 29.0% increase from the same period in 2023.

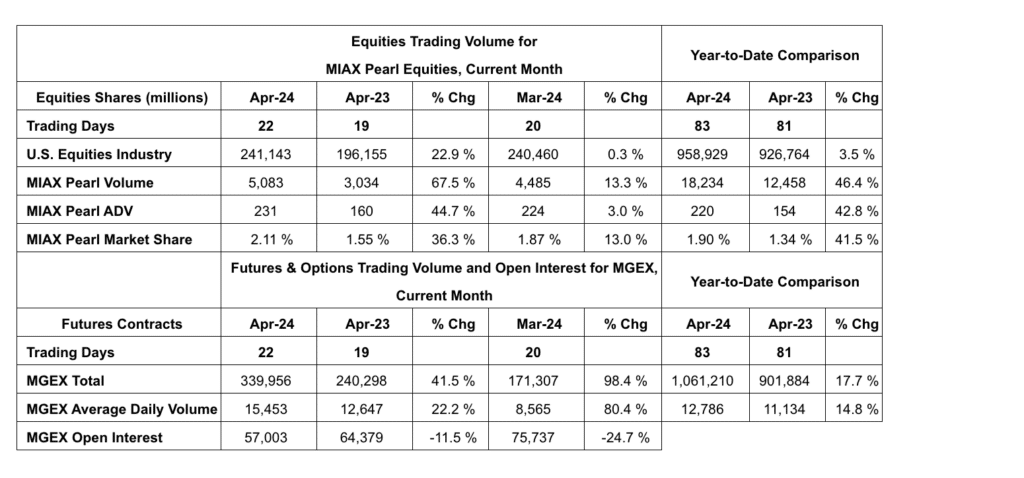

In U.S. equities, MIAX Pearl Equities™ reached a monthly volume of 5.1 billion shares, a 67.5% increase YoY and representing a market share of 2.11%, a 36.3% increase YoY. Monthly ADV reached 231.0 million shares, a 44.7% increase YoY. Total YTD volume reached a record 18.2 billion shares, a 46.4% increase from the same period in 2023. YTD market share reached a record 1.9%, an increase of 41.5% from the same period in 2023.

In U.S. futures, MGEX, a Designated Contract Market (DCM) and Derivatives Clearing Organization (DCO), reached a monthly volume of 339,956 contracts, a 41.5% increase YoY and representing a 98.4% increase from March 2024. ADV reached 15,453 contracts in April 2024, representing a 22.2% increase YoY.

Additional MIAX Exchange Group and MGEX trading volume and market share information are included in the tables below.

Source: MIAX

About MIAX MIAX’s parent holding company, Miami International Holdings, Inc., owns Miami International Securities Exchange, LLC (MIAX®), MIAX PEARL, LLC (MIAX Pearl®), MIAX Emerald, LLC (MIAX Emerald®), MIAX Sapphire LLC (MIAX SapphireTM), Minneapolis Grain Exchange, LLC (MGEX™), Ledger X LLC d/b/a MIAX Derivatives Exchange (MIAXdx), The Bermuda Stock Exchange (BSX) and Dorman Trading, LLC (Dorman Trading).

MIAX, MIAX Pearl and MIAX Emerald are national securities exchanges registered with the Securities and Exchange Commission that are enabled by MIAX’s in-house built, proprietary technology. MIAX offers trading of options on all three exchanges as well as cash equities through MIAX Pearl Equities™. The MIAX trading platform was built to meet the high-performance quoting demands of the U.S. options trading industry and is differentiated by throughput, latency, reliability and wire-order determinism. MIAX also serves as the exclusive exchange venue for cash-settled options on the SPIKES® Volatility Index (Ticker: SPIKE), a measure of the expected 30-day volatility in the SPDR® S&P 500® ETF (SPY).

MGEX is a registered exchange with the Commodity Futures Trading Commission (CFTC) and offers trading in a variety of products including Hard Red Spring Wheat Futures. MGEX is a Designated Contract Market (DCM) and Derivatives Clearing Organization (DCO) under the CFTC, providing DCM and DCO services in an array of asset classes.

MIAXdx is a CFTC regulated exchange and clearinghouse and is registered as a Designated Contract Market (DCM), Derivatives Clearing Organization (DCO), and Swap Execution Facility (SEF) with the CFTC.

BSX is a fully electronic, vertically integrated international securities market headquartered in Bermuda and organized in 1971. BSX specializes in the listing and trading of capital market instruments such as equities, debt issues, funds, hedge funds, derivative warrants, and insurance linked securities.

Dorman Trading is a full-service Futures Commission Merchant registered with the CFTC.

MIAX’s executive offices and National Operations Center are located in Princeton, N.J., with additional U.S. offices located in Chicago, IL and Miami, FL. MGEX offices are located in Minneapolis, MN. MIAXdx offices are located in Princeton, N.J. BSX offices are located in Hamilton, Bermuda. Dorman Trading offices are located in Chicago, IL.

Banks have made significant progress during the last decade in better managing market abuse risk, but bad actors continue to evolve their approaches in an attempt to fly under the radar of surveillance systems, according to Capco.

In its recent paper Trade & Communication Surveillance: Approaches to Vendor Selection, the authors Jonathan Lappage, Bea Simmons and Dan Young explore the evolving realm of market surveillance, emphasizing the critical impact of technologies such as artificial intelligence (AI) and machine learning on market regulation.

Over the last few years, market and regulatory drivers contributed to increased complexity that banks have to contend with, meaning greater investment in surveillance solutions.

Dan Young

However, this has at the same time racked up a significant amount of operational complexity, with many financial institutions operating anywhere from 5 -10 solutions, with some even more than that.

The paper mentioned that according to the FCA’s PATR, in 2021, 6.1% of trades during price sensitive announcements were anomalous; and the move to hybrid working also presents new challenges in monitoring the dissemination of inside information.

At the same time, in addition to the classic market abuse behaviours (e.g. insider trading, layering/spoofing, wash trades, marking the close/open), newer forms are emerging – these include pump and dump schemes led by social media ‘finfluencers’ and cybersecurity events (e.g. the hacking of regulator or newswire press releases prior to their publication to enable insider trading, and the dissemination and sale of confidential company information on the dark web), the paper said.

According to Capco, a typical bank analyses between one million and three million trade and comms alerts per year (an average of 3,000-10,000 alerts per day1).

“For each Suspicious Transaction Order Report (STOR) a bank raises, it will review anywhere from 15,000- 45,000 alerts, a vivid demonstration of the scale of false positives and potential to optimise alerting through effective alert calibration and analytics technologies,” the authors said.

To manage these high caseloads, banks have employed hundreds of on- and off-shore analysts – resulting in average annual surveillance spends, across technology and staff, of $10 million to $50 million per year, according to the findings.

“And despite this sizeable spend, instances of market abuse still slip through the net, only to be detected when the regulator comes knocking.”

“So whilst surveillance is not a profit-making activity, and today’s financial climate is very much focussed on cost-cutting, firms must exercise due caution in reducing investment levels,” the authors said.

Safe, trusted and compliant business encourages investment and attracts clients; the obverse can lead to regulatory enforcement actions with huge penalties and negative publicity, they said.

Firms can, however, still optimise their surveillance frameworks, without massively increasing investment levels, the authors said.

According to the paper, almost all major financial institutions utilise external vendors for the majority of their surveillance needs as it tends to be more cost-effective and dependable.

Nevertheless, given the size of the fragmented surveillance market it is not easy to navigate the market and select the right system to meet financial institutions (FIs)’ unique needs.

And depending on whether it is a sell-side or buy-side firm; or a market operator, there will be different solution needs.

According to the paper, vendors tend to have upwards of 100 ‘out of the box’ alert scenarios that are monitoring for different types of market abuse “FIs will select, often with assistance of the vendor, the subset of scenarios most relevant to their business, as identified through their risk assessments,” the paper said.

The authors said the market and regulatory drivers are reshaping firms’ approaches to surveillance, with key trends including cloud adoption, AI and machine learning, and a move to holistic surveillance – the ambition being to reduce costs, minimise false positives and better identify actual risks.

“Firms should assess vendor solutions based on these factors as well as others including vendors’ asset class coverage, data scalability, data normalisation approach, and, of course, price point,” they said.

“Once a shortlist of vendors has been identified – in collaboration with Compliance, IT and the Business – it is important you run Proofs of Concept so each option can be compared, including against any incumbent supplier solution,” the added.

“Implementing a new or replacing an existing solution can be a costly and time-consuming exercise; it is therefore vital you undertake thorough due diligence up-front to avoid mistakes which can take years to untangle,” they concluded.

MFA made recommendations for how the Commodity Futures Trading Commission (CFTC) should approach the use of artificial intelligence (AI) tools in derivatives markets in a comment letter. The letter is in response to the CFTC staff’s request for comment on the use of AI in CFTC-regulated markets.

The use of AI tools by alternative asset managers benefits derivatives markets, managers, and investors by reducing costs, improving market efficiency, and enhancing price discovery. The MFA AI recommendations are designed to protect markets and investors while not stifling innovation, competition, or the ability of alternative asset managers to generate returns for their investors, including pensions, foundations, and endowments. They also align with the CFTC’s traditional principles-based approach to financial regulation.

MFA recommends that when addressing any potential issues with the use of AI in derivatives markets the CFTC should:

Use existing regulations to address potential concerns posed by the use of AI tools

Remain technology-neutral and prioritize regulating market activities, not tools

Acknowledge that AI advancements have benefited markets, investors, and managers and are still developing and could unlock important benefits

“AI tools used by alternative asset managers enhance competition, reduce costs, and improve market efficiency. MFA’s AI recommendations will ensure the CFTC can address concerns it might have about the use of the technology without harming innovation, markets, or investors,” said Bryan Corbett, MFA President & CEO.

MFA’s comment letter also notes that the CFTC’s existing regulatory framework is well-designed to address the current and potential uses of AI tools.

“The CFTC’s technology neutral-framework appropriately addresses specific activities rather than technologies, and this approach has served the public interest well. While use-cases for AI are still evolving, the technology has demonstrated the potential to unlock important efficiencies and yield benefits. As a result, while the Commission must ensure its regulatory framework is adequate to govern the marketplace as it exists today, we urge the CFTC to avoid any potential actions that could unintentionally stymie the development of new technological tools that could augment human capabilities and ultimately amplify benefits to investors.”

More than 75% of surveyed asset managers are not likely to change their research process

More than 50% say the updates to MiFID II unbundling rules remove barriers to charging clients for research

Around 50% anticipate that the market will shift to operating an equal mix of client-funded and P&L-funded research within the next 2 years

London, 7 May 2024: Substantive Research, the research and market data discovery and spend analytics provider for the buy side, today publishes the results of its latest survey of the asset management community. The survey gauges the buy side’s appetite to make changes to investment research funding structures, following the latest consultation paper from the FCA: ‘Payment Optionality in Investment Research’, published on 10 April 2024.

The latest FCA Consultation Paper is in response to the July 2023 Investment Research Review led by Rachel Kent, which was published by the UK Treasury.

The review intended to address some of the unintended consequences of MiFID II’s ‘unbundling’ rules which, since implementation in 2018, have impacted competition amongst research providers, with larger firms being more able to absorb the costs of investment research on behalf of clients, whilst smaller firms and independent research firms struggled to do the same. The UK Treasury’s position is that MiFID II has had a negative impact on investment research coverage of SMEs and put the UK research funding rules at odds with the equivalent regulations in the US, adding challenging complexity for global asset managers consuming investment research from different jurisdictions.

The FCA Consultation Paper outlines potential changes to the research procurement process. In addition to providing optionality for asset managers to pay for their investment research on their own P&L, or bundled with execution fees, the Consultation Paper also states:

“The requirements on firms in relation to this new option would include them establishing: a formal policy on use of the approach; a budget for the amount of third party research to be purchased; ongoing assessments of research value and price; an approach to the allocation of costs across their clients; a structure for the allocation of payments across research providers; operational procedures for the administration of accounts to purchase research; and disclosures to clients on the firm’s approach to bundled payments, their most significant research providers, and costs incurred.”

The Substantive Research survey of buy side community found that:

The survey of 35 of the largest asset managers, representing AUM of more than $11 trillion, found:

76.5% of asset managers do not intend to make changes to their research process. (85% of the survey group currently operate on the P&L research funding model).

This shows that their actual research valuation processes can remain the same – many will have to change disclosure if they want to take advantage of new regulatory changes, but the message here is that the research procurement process is rigorous and comprehensive already.

55.9% believe that the suggested amendments to MiFID II will remove the operational barriers to allow them to once again charge their end clients for the investment research they consume.

Clients are still working out the precise implications of these rules and what needs to change, but it’s clear to many that they feel this won’t be a trivial undertaking.

Asset managers expectations for the funding of research across the industry in 2 years time comprises:

Majority of budgets move to client funded – 17.6%;

Existing P&L firms make no changes – 35.3%;

Broadly equal mix of client-funded and P&L-funded – 47.1%.

The majority of respondents expect change, but this points to an evolution rather than a rapid, large-scale move in the market.

‘Strategy Level’ disclosures and other requirements could mean a significant administrative burden and have deterred some firms from being early adopters.

Mike Carrodus, CEO of Substantive Research, said: “The buy side reaction to the FCA’s consultation paper is a three-way split, between those that want to transition to a client-funded research budget rapidly, those that will never do it unless they are literally the last P&L research payers left, and finally a large cohort that would be interested in reducing their own costs in a challenging market, but would like to watch this play out for a while. The key question remains: ‘How will end investor clients react to these returning costs, and how will asset managers’ adoption or avoidance of these new freedoms affect their competitive positioning?’”

He added: “What the buy side needs right now is a code – a set of standards that firms feel that they can sign up to. There will be different interpretations of the current wording of the FCA paper, and uncertainty on issues like what constitutes a ‘Strategy Level Budget’ and associated levels of disclosure. The buy side will want detailed frameworks to compare against, which the FCA can verify, ultimately providing more comfort to asset owners.”

Universe of firms covered by the research:

35 of the largest asset managers surveyed

AUM : > $11 Trillion

Geographic split: 19% N. America, 12% EU, 69% UK

Predominant Research Funding method in UK/Europe : 85%P&L, 12% Mixed P&L / client-funded, 3% client-funded

Notes to editors

Rachel Kent’sInvestment Research Review recommended that buy side firms that use investment research should:

Allocate the costs of research fairly between their clients, having regard to the obligation on regulated firms to treat their customers fairly;

Have a structure for the allocation of payments between the different research providers – such as Commission Sharing Agreements;

Establish and implement a formal policy regarding their approach to investment research and how it is paid for;

Periodically undertake benchmarking or price discovery in relation to the research that the firm uses.

The review was intended to urge asset managers to return to charging end investor clients for the external research they use, with the hope that this would drive more flexibility to pay for more research on SME and mid-cap companies which currently struggle for coverage and attention, as well as boost competition amongst research providers.

Substantive Research provides independent comparison and discovery on investment research, ESG and market data pricing and products, to financial institutions that represent a combined AUM of more than $18 trillion and total assets of over $25 trillion.

Via the Substantive Research platform, research and data consumers can compare their provider pricing, budget allocations and benchmark consumption habits versus their peers, to optimise their overall research and data spend.

In 2021, Substantive’s offering expanded to include an award-winning ESG Dashboard that provides a searchable database of more than 140 ESG providers, mapping out the ESG data market and showing the choices available. This gives customers the opportunity to discover and compare suppliers of ESG data all in one convenient place, as well as providing confidence that they are gaining accurate views of actual ESG performance. Substantive Research’s ESG Dashboard won the “Best ESG Data Initiative” Award at the WatersTech Inside Market Data Awards 2022.

TECH TUESDAY is a weekly content series covering all aspects of capital markets technology. TECH TUESDAY is produced in collaboration with Nasdaq.

Exchanges can trace their origins back to the Middle Ages. Since then, however, technology has transformed the global capital markets, and the speed of trading has accelerated with the adoption of computers to trade, mostly over the last 50 years. Today, quotes and trades travel over microwaves, lasers and optic fibers – often at close to the theoretical speed of light.

Fiber optics, microwaves and lasers replace trading pits

In today’s modern markets, orders, confirmations, quotes and trade data move digitally along a combination of cable, microwave, millimeter wave and, most recently, laser.

As with most aspects of trading, there is a tradeoff with each.

Chart 1: Different data transmission technology

Fiber is the most reliable and has the most bandwidth. Fiber optic cables work by sending light pulses along fiber or glass tubes. Because light slows down in the glass, fiber is “slower” than the alternatives, and it’s best to use it if you need to send a lot of data or detailed data.

In contrast, microwaves — millimeter waves and lasers — all move through the air. That makes them all faster than fiber but are more prone to signal disruptions due to natural events, such as the passage of clouds, rain, mountains. This phenomenon makes them unreliable for a split second or hours affecting market liquidity.

The curvature of the Earth is also a problem. Wireless transmitting requires frequent signal towers high enough to see over mountains and around the globe. In fact, the curvature of the Earth alone makes the Earth slope 100 feet every 25 miles.

Furthermore, wireless transmissions can’t hold as much data as fiber, and the signal tends to fade faster (needing more “repeater” stations to amplify and resend the signal. However, that is where tradeoffs between laser and radio waves begin.

Table 1: Benefits of different types of data transmission technology

*Anova system uses a combination of laser and mm wave

Both microwaves and millimeter waves are a type of radio frequency signal. Radio signals travel pretty close to the speed of light and around 50% faster than light can move down a fiber cable, so switching to using microwaves can really decrease how long it takes to find out when prices and markets elsewhere have changed (also called “latency”).

The main difference between microwaves, millimeter waves and lasers is their frequency and wavelength. This requires us to get into a little physics.

Frequency measures the number of waves that pass a point in a second; a higher frequency means more waves move in that second. Wavelength tells us how much energy the signal can carry; a larger wavelength has less energy and carries less data, while shorter wavelengths have more energy and carry more data. We can hear this with sound waves. Low tones have long wavelengths and sometimes are hard to hear. High notes have higher frequencies, and some can hurt our ears.

However, we are talking about electromagnetic waves – some of which we can see. Chart 2 shows how the wavelengths change and where they are useful.

Chart 2: Electromagnetic spectrum

Overall, the main latency (speed) difference is between wireless and fiber. Capacity (or bandwidth) then differentiates each of the technologies, too, with higher frequency, giving millimeter waves an advantage over microwaves, but at the cost of shorter distances between antennae.

What about satellites?

We’ve all heard of satellite TV. Why don’t we trade with satellite messages?

It turns out the distance from Earth to a satellite and back matters – and is longer than around the surface of the Earth. However, some say low Earth orbit satellites could work for long distances.

Even a very short distance, like the distance from Nasdaq to Secaucus (where dark pools sit, pegging peg prices to primary quotes), can matter to certain traders.

Via fiber, the theoretical fastest speed is around 162us (microseconds).

That might not seem like much (it is, after all, a fraction of one-thousandth of a second). But even in an Olympic race, a split second can be the difference between winning and second place – here, it might mean completing an arbitrage or being legged and exposed to losses.

Think of this a different way: There are about 35 million trades a day and only 23.4 million milliseconds during market hours. In short, microseconds can matter. And that’s before we discuss how most activity happens in 1% of the microseconds in the day. That’s why traders doing strategies where latency is important choose to use wireless technology. And the advantages and disadvantages of each are why millimeter wave, microwave and lasers exist.

But it’s also important to remember that to a human optic fiber is very fast, too – and it’s accurate and can handle large bursts of activity with less backlogs. That’s why it’s used for the SIP.

Just like for the past hundreds of years, it’s likely that the race for lower latency will continue. However, the reality is that if you’re using wireless now, you’re already pretty close to the theoretical limits of the speed of light, and you’re aware of the tradeoffs you’re already making to get there.

Phil Mackintosh is Chief Economist at Nasdaq.Nicole Torskiy, Economic Research Senior Specialist, contributed to this article.

Creating tomorrow’s markets today. Find out more about Nasdaq’s offerings to drive your business forward here.

From Herstatt to Credit Suisse: Banking’s Fifty-Year Call for Real-Time Reconciliation

By Alex Knight, Head of EMEA, Baton Systems

It is tricky to think of another industry where speed and accuracy are of such paramount importance. It is, therefore, even harder to work out why the banking sector is still so reliant on slow, antiquated processes when it comes to payment reconciliations.

Next month marks five decades since midsized German bank Herstatt experienced a sudden collapse due to its involvement in risky FX speculation. The bank had received payments in various currencies from counterparties in different time zones, only to then fail to make corresponding payments in other currencies before it was closed down by rule makers.

The trouble is, fifty years on, the banking sector has ballooned in terms of its importance to the global economy. Many estimates place the banking sector at around 20-25% of the world economy (source: Research and Markets – Financial Services Global Market Report 2021: COVID-19 Impact and Recovery to 2030). Therefore, when stresses to the system emerge, the knock-on effects can be severe. When a globally systemically important bank like Credit Suisse is identified as facing liquidity challenges, as was the case last year, the prevalent use of outdated post-trade processes across capital markets, such as reconciling payments one or more days after settlement, can have serious ramifications. This means, if a full-blown crisis emerges, counterparties can’t determine how exposed they are, because they lack the critical information needed to identify which payments have been sent and received so far that day. A situation, like what happened to Credit Suisse and has also happened to smaller institutions, underscores the urgency for a significant shift towards real-time payment reconciliation systems. Failure to act doesn’t only jeopardise individual firms, but can also propagate systemic risk, leading to catastrophic consequences reminiscent of past financial crises.

When market speculation mounts into tangible threats of liquidity crunches, financial institutions naturally resort to safeguarding their interests. Payment controls are instituted to mitigate settlement risks, albeit in a fragmented and, in some cases, manual manner. This decentralised approach, often controlled at the individual business level, fosters inconsistencies, and could potentially introduce loopholes for errors, posing financial, operational, liquidity and reputational risks. Moreover, a lack of oversight could trigger future systemic instability, amplifying the gravity of the situation.

Central to the issue is the timeliness and accuracy of payment reconciliations. The existing practice of initiating the reconciliation processes only at the very end of each day (once the US dollar market is closed), leaves institutions operating in the dark regarding their exposure. This delay, while seemingly innocuous, can have dire implications – particularly in times of financial stress. The inability to ascertain real-time payment status not only undermines confidence but also perpetuates a cycle of uncertainty, compounding the risks for all parties involved. In certain scenarios, banks may hold all outgoing payments using their manual and fragmented controls. However, the dilemma lies in discerning which payments they’ve received from the counterparty throughout the day, hindering their ability to release funds appropriately. Without real-time reconciliation, firms may understandably take a cautionary approach and withhold outbound payments to the at-risk counterparty until reconciliation (generally delayed by at least a day, as outlined above) confirms which ones are safe to proceed with.

In addressing this pressing, and frankly longstanding, concern, the imperative is clear: real-time payment insight is non-negotiable. The convergence of business, risk, treasury, and operations necessitates a seamless flow of information, devoid of manual interventions and time lags. By embracing automated, real-time reconciliation processes, institutions can empower decision-makers with the information needed to navigate turbulent waters confidently.

Imagine a scenario where payment reconciliations occur seamlessly and continuously throughout the day. Armed with real-time information, institutions can accurately assess their exposure and make informed decisions regarding the release of outbound payments. This proactive approach not only averts potential defaults but also fosters market stability by honouring commitments and mitigating systemic risks. However, achieving this transformation requires a departure from complacency. The notion of ‘if it isn’t broke, don’t fix it’ is no longer tenable in a fast-moving and inter-connected banking world marred by uncertainties. Financial institutions must acknowledge the inherent flaws in outdated processes and embrace technological advancements to stay ahead of the curve.

Ultimately, the need for real-time payment reconciliations transcends mere operational efficiency — it is a matter of systemic and regulatory resilience. By prioritising the adoption of automated, real-time reconciliation systems, financial institutions can fulfil their obligations, mitigate risks, and contribute to a more stable and orderly market. The time for action is now; the stakes are too high to delay.