By Greta Zhou, Vice President, APAC AES Product, Credit Suisse, and Andy Cheung, Head of APAC AES Sales, Credit Suisse

Our reliance on smart machines has never been greater. Data scientists believe the adoption of artificial intelligence (AI) is exhibiting exponential growth as businesses and individuals are increasingly leveraging the high processing speed of machines for analysis and decision making. Even the best chess players in the world are now teaming up with machines to compete with other human/machine pairings. Against this backdrop, it would be wise for electronic trading desks to assess novel ways to leverage machine learning for the benefit of their clients.

RISE OF THE ALGO WHEEL

The importance of this game-changing technology is both demonstrated and perpetuated by the rising penetration of the algo wheel. By definition, the algo wheel is an automated order router to assign the best-performing strategy and parameter settings to performance based on specified trading benchmarks. Within the last four years, the number of buy-side firms with algo wheels in Asia Pacific has increased by 47%.Its user base has become increasingly diverse, ranging from long-only asset managers to long/short hedge funds and quantitative traders. In addition, wheel evaluation mechanisms have become more sophisticated: buy-side firms now employ machine learning models to measure and predict the best matching broker algo for a given type of order flow.

Currently, the prevailing wheel benchmark is Implementation Shortfall (IS), or arrival-price based. Historically, to perform well against the IS benchmark, brokers have either used a pre-planned trading trajectory with optimal execution rate to balance the market impact and time risk; or explicitly determined a trading rate range and executed in line with market volume opportunistically based on trading signals. Both approaches have their merits and demerits. The development of a hybrid approach, leveraging machine learning models to adjust trading trajectory dynamically, can allow an algo to harness the strengths of both while avoiding some of the pitfalls.

ADAPTING TO CHANGING MARKET CONDITIONS

When targeting an IS benchmark, the client’s order size, its potential to impact the market price, and stock characteristics should influence the baseline speed and overarching trajectory that an algo uses to execute. Overlaying that baseline, the algo should intelligently perceive and adapt to real-time market conditions. Amongst the many data points that an algo must consider, three key factors are crucial for high-quality execution: expected liquidity, intra-day volatility, and price alpha.

When anticipating lower volume for the remaining day, the algo should increase the participation rate in order to complete. When the intra-day volatility spikes, it should speed up to cut its exposure to the risk of uncertain price movement over time. Finally, it should respond to reliable price alpha signals to improve tactical execution performance over short time horizons. This is precisely where the power of machines comes into play, with their ability to use massive data sets and analytics to diagnose situations and make decisions in microseconds. At Credit Suisse, we have been investing in machine learning models to enable real-time predictions of market volume, volatility and price movement. Specifically, for the IS wheel, these real-time quant signals have augmented the algo to be more adaptive to the ever-changing market environment.

VOLATILITY HAS AMPLIFIED THE NUMBER OF DATA INPUTS

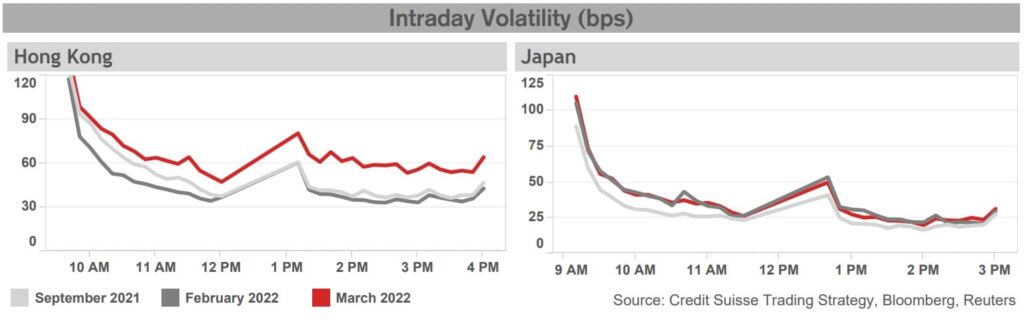

We have seen heightened volatility globally in the past two years, with extreme price swings intra-day. As seen in Figure 1 it is evident that prices fluctuate wildly intra-day, usually hovering around the higher levels during the opening and closing auctions, and spiking in the afternoon open in markets like Hong Kong and Japan. In addition, we also witnessed a further significant increase in volatility in March in Hong Kong. While simple historical volatility illustrates a trend, it is not a valid proxy for what traders actually experience during a trading day.

In Asia, our algo quant team has introduced an intra-day volatility prediction model that considers a range of quantitative metrics, including order book, volume, volatility, spread, and price returns, to capture real-time dynamics. With more accurate intra-day volatility prediction, we can map out the optimal trading rate to perform versus the IS benchmark, adjusting according to whether the same order arrives pre-open or intra-day. Similarly, a trade plan made hours ago may not be the most optimal plan as market conditions fluctuate. As intra-day volatility predictions evolve based on real-time conditions, the IS algo reexamines its plan and adjusts its target participation accordingly in real time.

A RAPID FEEDBACK LOOP TO IMPROVE PRICE PREDICTION

Long-term price signals are scarce and hard to get right consistently. On the other hand, a reliable short-term signal is more achievable and can provide a means of enhancing the trade plan to improve performance. We have further built out our price prediction to incorporate trades and order events into order book imbalance, and introduced a self-correction mechanism, such that if the actual price deviates from previous predictions, the next calculation adjusts for that error and rectifies future forecasts. Based on back-testing results, the overall precision of the new price prediction model is over 65%.

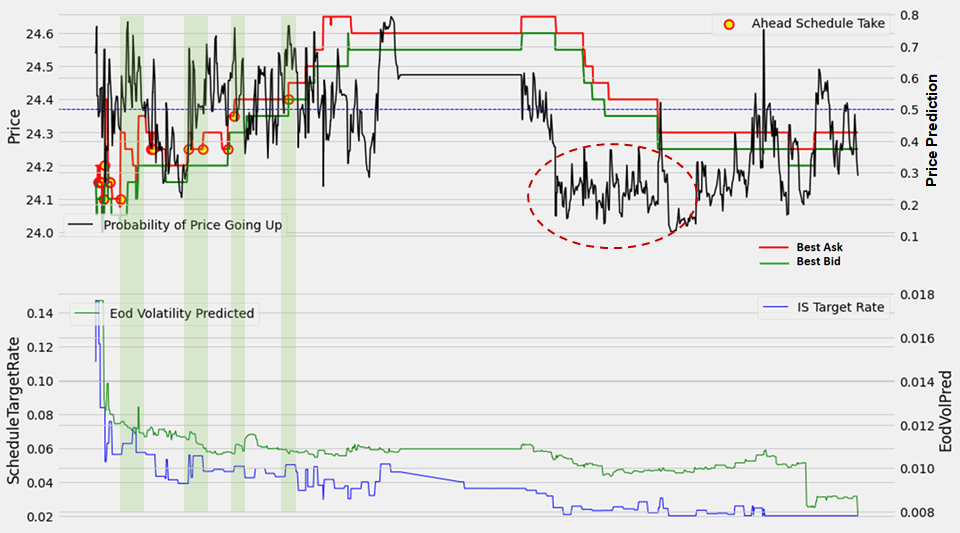

Figure 2 is an illustration of a Hong Kong buy order, demonstrating how the IS algo adjusts trade planning based on real-time quant signals. The intra-day volatility prediction (green line in the bottom) is trending downward in general, resulting in a higher participation in the early morning, and gradual decaying towards the afternoon. The price prediction (black line) matches with the morning rally and correctly predicts the early afternoon drop (dotted circle). The adverse move prediction in the morning triggers a target rate bump up (in shaded green) ahead of schedule to seize liquidity before the market moves away.

Provided with a reasonably wide participation band, the algo is empowered with discretion to vary the pace and timing of its execution and is given the leeway to adapt to an ever-changing market environment in its quest to meet its goal.

Conclusion: Machine driven predictive analytics provide advanced capabilities for both the buy side and sell side to make highly informed trading decisions. When developed well, the machines are the perfect partner to analyze the order book, dynamically fine-tune the strategy, and predict the best performing algo for a given order profile and benchmark. The immense competitive advantage that this technology provides is undeniable. Our new enhancement for the IS wheel is a tangible example of how these great advances are being put to use to solve our clients’ practical trading challenges in the here and now.

Please follow the attached link to important disclaimers:

credit-suisse.com/asiapac/legal/marketcommentary

This article first appeared in the 2022 Q2 issue of GlobalTrading, a Markets Media Group publication.

{kind=link}