By Don Steinbrugge, CFA, Founder and CEO, Agecroft Partners

The hedge fund industry is dynamic, comprising numerous strategies that attract varying degrees of interest over time. Various factors, such as capital market valuations, economic growth expectations, inflation rates, market liquidity, and risk tolerance, significantly influence the demand for each strategy. Industry professionals spend a great deal of time analyzing these variables in order to identify which strategies are expected to offer the best opportunities for out-performance. One way to measure this is to ascertain which strategies are attracting current investor interest.

In this paper, we compare and analyze data submitted by investors from our November 2022 cap intro event with data recently compiled from the first 300 investors slated to attend our upcoming Gaining the Edge – Global Virtual Cap Intro 2024 event taking place from June 17th to 28th. During registration, investors complete a detailed survey outlining their preferences regarding strategy types and managers that are of current interest. This provides broad insights into both overall demand for each strategy as well as evolving trends in demand. Presented below is a comparative analysis of our survey findings, accompanied by commentary derived from feedback received from thousands of investors globally.

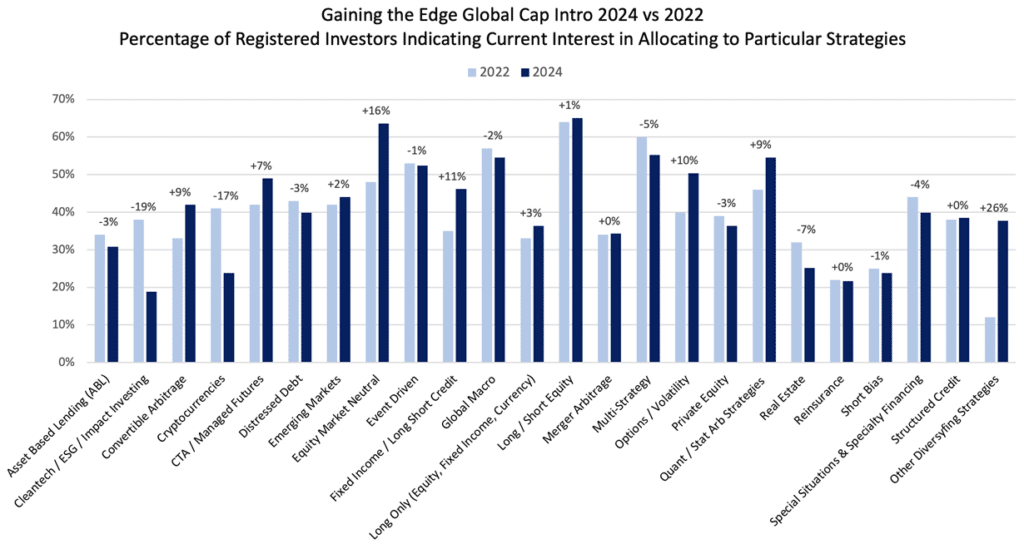

Long/short equity captured the interest of 65% of 2024 respondents, the largest share among all strategies. This slight uptick from 2022 (64%) indicates the continued positive change in investor sentiment regarding fund managers’ abilities to generate alpha via stock selection. It may also be attributed to higher equity valuations with the current bull market extending through Q1 of 2024, propelled largely by a small number of mega cap growth stocks. This rally has created wide valuation disparities between growth and value stocks along with large and small/mid-cap stocks. Many investors believe both are great environments for active managers. We expect increased demand for funds focused on value or small/mid-cap companies.

The three strategies that saw the largest increase in demand, included equity market neutral, fixed income/long short credit, and other diversifying strategies.

1. Equity market neutral increased by 16% due to investor concerns about equity valuations and favorable conditions for stock selection.

2. Fixed Income/long short credit increased by 11% due to significantly higher interest rates.

3. Other diversifying strategies increased by 26% which demonstrates that investors are broadly open to any strategy that will help diversify their portfolio away from the capital markets.

Strategies that saw the biggest decline in demand include Cleantech/ESG/Impact Investing and Cryptocurrencies. Both saw a complete reversal compared to their historical trends, but should be interpreted differently based on real-world investment flows.

1. Cleantech/ESG/Impact Investing enjoyed peak interest at our 2021 event at 48%, but declined to 38% in 2022 and 19% for 2024. The strategy drew significant attention from investors, but has not yet generated the asset flows that were expected. The criteria that determine what qualifies as an ESG strategy are broad and vary from one investor to the next. We expect ESG criteria to become more standardized across the industry over time, which should aid managers in the space.

2. Digital Asset and Cryptocurrency strategies saw a sharp decline from 41% in 2022 to 24% in 2024. Despite the decline, we believe this is a strategy that could see increased asset flows as the strategy has evolved from an educational product to one that allocators are giving serious consideration. The asset class continues to be viewed as less exotic/speculative and more institutional. Beyond the staggering returns, several factors are contributing to the increased recognition and demand, including a broader understanding of block chain technology and an increase in the size of the industry.

Since average pension fund allocations tend to be multiple times larger than those from other types of investors, their strategy preference has a disproportionate impact on industry flows. The data we shared from the surveys gave each investor equal weighting. Practically speaking, strategies with higher interest from pension funds, such as CTAs and reinsurance, will likely see much higher asset flows than the survey data would indicate. For CTAs, demand tends to be higher for short term trading oriented strategies versus medium-term trend, where many pensions already have exposure. Reinsurance is seeing increased demand from large pension funds due higher prices across the industry and its low correlation to the capital makers.

Other strategies showing high investor demand include Global Macro (55%), Quant (55%) and Multi-Strat (55%). A full list of results are posted in the chart below.

In addition to indicating strategies of interest, investors were also asked to indicate the minimum fund size to which they would consider making an allocation. Of the survey respondents, 28% would consider new fund launches with 52% open to funds with less than $100 million and only 1% requiring a fund to be $1 billion or larger. These results indicate that the minimum asset requirement for various investor types has reduced over time, especially in the past several years. This may be, in part, attributable to the significant investment large pension funds have made into improving their internal processes. A majority have built out their research staffs and, in so doing, have increased their confidence and comfortability with investing in smaller and emerging managers.

Another high-level trend includes the divergence, by investor type, in how hedge fund strategies are considered in the portfolio allocation process. Specifically, many pension funds have evolved their hedge fund allocation strategy from outperforming hedge fund indices to building portfolios of diversifying strategies. This has narrowed their interest across strategies to a focus on those with low correlation to the capital markets.

As we head into Q2 of 2024, this survey should provide good guidance on the strategies to which assets will flow. Additionally, as most investors and managers have become comfortable using Zoom and other virtual meeting providers as part of their ongoing due diligence process, we expect a high percent of meetings to take place virtually, continued acceptance of remote virtual work, and increased allocations to managers located outside of traditional hedge fund cities.

Gaining the Edge – Global Virtual Cap Intro 2024 is expected to be one of the largest virtual cap intro events in the industry and is complimentary for approved investors. If you would like to see more information on the event please visit: https://gteconferences.com/.