Jeffrey Sprecher, chairman and chief executive of ICE, said US equity market structure is flawed and hopes it will be reviewed by the Securities and Exchange Commission under the new administration.

Sprecher said an earnings call last week that when ICE acquired the New York Stock Exchange they had been vocal about the need to change US equity market structure.

“We tried to negotiate a grand bargain but we were unsuccessful,” he added.

Late last month, a record number of US equities were traded as retail investors bought shares in retailer GameStop, which had been shorted by some hedge funds, following posts on social media platform Reddit. This led to extreme volatility in some stocks and Robinhood, the app that many investors had used for trading, temporarily suspended activity in some shares which led to outrage from customers. Robinhood said in a blog that its clearinghouse-mandated deposit requirement had increased ten-fold.

Sprecher said: “The current market structure paralyses the industry and stifles innovation in my view.”

He continued there is an opportunity for change under Gary Gensler, who has been nominated as the new head of the SEC. Sprecher said Gensler is well informed about market structure as he previously worked at Goldman Sachs and was formerly head of the Commodities Futures Trading Commission.

“There is an opportunity for a new clear vision,” Sprecher added. “We need another grand bargain where we give up some unique positioning to improve innovation, transparency and the growth of capital markets.”

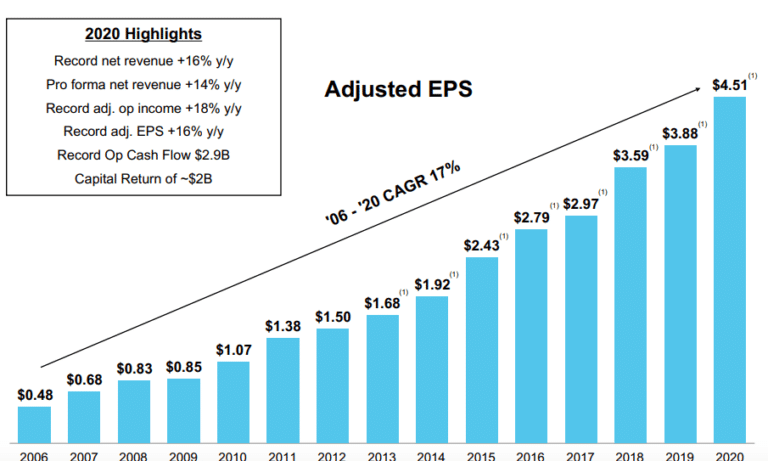

ICE reported 2020 record net revenues of $6bn, a 16% year-on-year increase.

Growth initiatives

Ben Jackson, president of ICE, highlighted growth initiatives including the launch of ICE Futures Abu Dhabi next month with the Abu Dhabi National Oil Company and nine of the world’s largest energy traders.

IFAD is due to start and trading in ICE Murban Crude Oil Futures on March 29, subject to the completion of regulatory approvals.

Jackson continued that ICE will continue to provide services for the exchange-traded fund industry.

“Assets in fixed income ETFs have grown by 25% over the past five years,” he said. “As well as providing key pricing data, we are the second largest fixed income indices provider.”

In 2019 the firm launched ICE ETF Hub to standardize and simplify the process for creating and redeeming ETF shares. The platform currently supports US listed domestic equity and fixed income ETFs.

Last year ICE launched a FIX API to allow authorized participants to connect to the platform. Bank of America was the first user and the API provided an end-to-end, fully electronic workflow between the bank’s order management system and ETF issuers’ platforms.

ICE ETF Hub’s custom basket negotiation technology allows primary market participants to negotiate and assemble custom basket proposals in an automated environment. ICE Chat functionality was also added to support communication throughout the custom basket workflow and now has more than 100,000 users.

Jackson added that ICE would continue use its expertise in analysing unstructured data to create new data services such as for environmental, social and governance strategies and mortgages.

This month ICE said Bakkt Holdings, the digital asset marketplace launched in 2018, is going to be acquired by a special purpose acquisition company sponsored by Victory Park Capital and listed on the New York Stock Exchange. ICE is expected to have a 65% economic interest and a minority voting interest in the combined company, valued at $2.1bn.

Sprecher said: “The combination means adding incremental capital, increasing growth potential as the NYSE listing will add to brand recognition and unlocking value for ICE shareholders.”

Libor transition

This month the firm launched ICE Term SONIA Reference Rates as a benchmark for use in financial instruments by licensees to support financial markets in benchmark transition.

After the financial crisis there were a series of scandals regarding banks manipulating their submissions for setting benchmarks across asset classes, which led to a lack of confidence and threatened participation in the related markets. As a result, regulators have increased their supervision of benchmarks and want to move to risk-free reference rates based on transactions, so they are harder to manipulate and more representative of the market.

The FCA has already said it will not compel panel banks to submit Libor beyond 2021 and the market should switch to Sonia, the risk-free rate chosen by the UK authorities.