Christopher Hogbin has been appointed CEO of Lazard Asset Management, effective December 2025, according to a press statement. He has 30 years of professional experience, including 20 years at AllianceBernstein, where he most recently served as Global Head of Investments and a member of its Executive Leadership Team. Hogbin succeeds Evan Russo, who after two decades of contributions to Lazard will step into an advisory role following the transition. Russo joined Lazard in 2007, and in addition to serving as CEO of Lazard Asset Management, he has held several leadership roles during his tenure, including Chief Financial Officer of Lazard and Co-Head of Lazard’s Capital Markets and Capital Structure Advisory practice.

Amjad Zoghbi has joined TRG Screen as Head of AI, a newly created position, according to a press release. He has more than 20 years of senior technology leadership and hands-on market data expertise. Zoghbi was previously Head of Solutions Engineering at TRG Screen, where he led the global pre-sales function across the company’s product portfolio — including spend and inventory management, usage monitoring, compliance.

James J. Moloney

The Securities and Exchange Commission (SEC) has named James J. Moloney Director of the agency’s Division of Corporation Finance, effective October, according to a press release. Cicely LaMothe, who has served as Acting Director, will return to her role as a Deputy Director of the Division. Moloney previously served at the SEC for six years prior to joining Gibson Dunn & Cutcher, where he has worked the past 25 years, ascending from corporate associate to equity partner. He has served as a longstanding co-chair of the firm’s securities regulation and corporate governance practice.

Zoe Tipper has joined Peel Hunt as an equity sales trader, the Desk reported. Based in London, she reports to Matt Reali, head of sales trading. Tipper has close to a decade of industry experience and joins the firm from HSBC, where she has been an associate director since 2023. Prior to this, she spent more than six years with JP Morgan Chase & Co as an analyst and equity sales trader.

Ultimus Fund Solutions has appointed John Lehner as President, Ultimus Public Fund Solutions, and Jay Martin as President, Ultimus Private Fund Solutions. In conjunction with the new hires, Jim Cass will transition to Vice Chairman of Ultimus, having previously served as President, Ultimus Private Fund Solutions. All three roles report to CEO Gary Tenkman. Lehner brings over 20 years of transformational executive leadership experience in investment management and technology-driven financial services. He joins Ultimus Fund Solutions from FundGuard, where he served as President. Martin has nearly four decades of experience in financial services, with expertise in large and complex sales opportunities, comprehensive client implementations, and global transformation efforts. Most recently, he served as President, Investment Services for U.S. Bank.

If you have a new job or promotion to report, let me know at alyudvig@marketsmedia.com

Regulation National Market System (NMS) Rule 611 a.k.a. Order Protection Rule (OPR) was adopted 20 years ago. The SEC is hosting a roundtable on September 18, 2025 with 3 panel discussions: (1) market participants’ experience with trade-through prohibitions; (2) a trade-through prohibition’s role in today’s market structure; and (3) forward thinking. Two Commissioners (one being the current SEC Chair Paul Atkins) had previously expressed their dissent on the OPR. Is it the right time to roll-back or modernize OPR? What changes to the OPR and other relevant provisions of the NMS would contribute to the furtherance of market efficiency without compromising market integrity? This article discusses the strategic possibilities.

Context Matters

The historical transition from principle-based “Intermarket Trading System” (ITS) that was launched in late 1970s to OPR, the SEC cited concerns and rationales in the past that included: “fairness across venues where investors receive inferior price because of trade-throughs; uniform rules reduce fragmentation and gaming of slower venues; and codify protection foster trust in NMS in the post-decimalization era given the rise of Electronic Communication Networks and Alternative Trading Systems (ATSs).” OPR was welcomed by retail, while it complicated the way institutional firms move trade blocks. OPR price protection in automated markets relies on a centralized Processor – SIP for market data. Best Execution (BestEx) requires a trade-by-trade review with consideration of liquidity priced better than the top-of-book National Best Bid and Offer (NBBO).

To foster an ecosystem in racing toward constant refreshing of the NBBO with meaningful size of at least a round lot to execute a trade, OPR’s simultaneous routing requirement is: “when a trading center [Exchanges, ATSs, and other OTC market makers] receives an Intermarket Sweep Order (ISO), it may execute the order immediately – even if better-priced quotations exist elsewhere – provided that the ISO sender simultaneously routes additional ISOs to those other venues to execute against the full displayed size of any better-priced protected quotations.” Points of controversy include: technically difficulties during high-speed market events (e.g. Flash Surge, MEME); latency-sensitive traders exploited latency gaps between quote updates and ISO routing; logistical challenges, analogy to different travel sites offer varying top recommendations (i.e. fragmentation); and the time precision on what constitutes as “simultaneous”. We do NOT believe any trading centers lack the technical know-how to handle simultaneous routing, but whether they want to and to what degree it would be profitable for them.

The noumenon of NMS, where a single change to the components (OPR, Market Data, Tick Size, Access Fees, Payment for Order Flow, BestEx compliance, definition of Exchange / Dealer, etc.) can affect the entire system, market integrity, as well as the US competitiveness with foreign markets. Amid imperfection, “the US equity markets are the most robust in the world and continue to be among the deepest, most competitive, most liquid and most efficient.” Some feel comfortable with the current stage of equilibrium amid the NMS stock and listed options markets have as they evolved overtime. When formal rules do not yield the most optimized market efficiency, informal practices as “sub-system” emerge as a counter response.

What broken needs to be fixed

OPR did provide exceptions (e.g. non-automated quotes, flickering quotes, VWAP trades). Our observed counter responses to a less-than-optimal NMS include: ATSs together with all the TCA, BestEx compliance, liquidity sourcing, outsourced execution tools and smart order routers were developed to fabricate the fragmented markets that are underserved by exchanges. These tools are “bandages” and often profit from an ever more fragmented market. Market participants are required to comprehend various order types and functions of different lit and dark venues. More and more choose to collaborate with HFTs for outsourced execution capabilities rather than compete. Distorted rebates and other gimmicks to get ahead of others all favor the Elites. Smaller firms struggle to survive and merge away (number of FINRA registered firms has dropped from 4,000+ in 2014 to 3,249 at 2024-year end). Bandages-over-bandages of bureaucracy attributed to an upside-down smile curve and have widened the gap between the “haves” and “have-not.”

Market Data Infrastructure Rule (MDIR) modernizes how market data is collected and disseminated by introducing competing consolidators to create a decentralized, competitive market data infrastructure. It will ultimately replace the previous exclusive, exchange-run SIP model. MDIR is a step towards allowing competing market forces to reduce the government or centralized party involvement in the markets. However, the SEC currently has a partial stay of the amendments to §600(b)(89)(i)(F) of MDIR that requires “the primary listing exchange to provide an indicator … of the applicable minimum pricing increment… under the definition of regulatory data” with respect to OPR Rule 612, and Rule 610(c) regarding reduction in access fee cap.

Many smaller broker dealers depend on ATSs to counter the disadvantages they face with lit venues’ skewed privileges (32 mils super tier rebates, faster proprietary feed market data connections, DMM programs, etc.) provided to the elites. There are “onerous administrative obligations on data users, ambiguous language in the agreement, frequent unilateral amendments to the agreement, general lack of transparency on terms and conditions, excessive fees, increase of fees through penalties, and overly burdensome audits,” plus high switching and connectivity costs, as well as learning about nuances like trade-out, allocation, anti-gaming, adverse selection, pool vetting, etc. All drive up the cost of market transactions.

Within and among Exchanges, ATSs, Systematic Internalizers (SIs), Single Dealer Platforms (SDPs), there is already intense competition. Unhealthy competition in a low-latency arms race has made the trading community subservient to the telecom infrastructure. To address that, time-lock encryption should be adopted to make market data available securely in synchronized time. Another key issue to address is the LACK OF STANDARDS across different market centers’ rebate and incentive. A mechanism is needed to efficiently delineate the rights and obligations about WHO OWNS THE DATA.

US advantages over other jurisdictions

OPR does NOT put the US in a competitive disadvantage to its neighbors – Canada and Europe. Similar to the US, the enforcement of Canadian-style order protection focuses on trading venues’ responsibility. In contrast, the scope of the Canadian rule is applicable to all visible accessible quotes instead of the US top-of-book per CSA National Instrument 23-101. In Canada, OPR is a shared responsibility between marketplaces and participants, and directed action orders resemble ITS-era discretionary routing, allowing participants to bypass better-priced quotes without strict simultaneity.

The UK and EU have no OPR. They place substantial burden on investment firms to comply with best execution obligations under MiFID II and MiFIR. Amid Europe is catching up in building a centralized Consolidated Tape (CT, similar but different than the US SIP), industry associations are opposing mandatory consumption of CT for BestEx quality assessment. The ESMA has stated, “these evaluations will not take the standardized shape of SEC Rule 605 or 606”. Addressable liquidity is a fluid concept in Europe. The UK Financial Conduct Authority has opted to shift away from it, particularly in the context of SIs and post-trade transparency reforms. The US should resist any impulse to emulate regulatory missteps observed abroad—it must lead, not follow, in setting robust market standards.

Factors attributed to the US advantages over other jurisdictions: (a) placing the burden on those who can afford it (e.g. Exchanges who rent seek from everyone, G-SIBs) and be practical to drive down costs for all market participants; plus (b) innovations. We acknowledge that it increases costs to connect with additional venues for BestEx compliance when those additional venues may add little or no real benefit. Canada introduced a 5% market share threshold to exempt dealers having to connect to new marketplaces with visible quotes that are under the threshold. That being said, such thresholds hinder innovations from smaller venues and deter new entrants to compete with their larger counterparts.

To NOT exacerbate the gap between the “haves” and “have-not,” the focus should be about incentivizing innovations to overcome the high switching and connectivity costs, as well as learning about nuances like trade-out, allocation, anti-gaming, adverse selection, pool vetting, etc. For example, Model Context Protocol (MCP) works like a USB-C connector to ease some of the API costs. MCP accommodates latency draft and can be used for cross-venue price discovery. AI agents reconcile fragmented quotes in conjunction with MCP’s context-rich orchestration that respect execution preference, data providers’ paywall integration, and how HFTs may monetize microstructure inefficiencies in real with MCP are to be wait-and-see.

No point in gutting OPR for Crypto Trading

It is an Animal Farm where every constituent wants to negotiate to be “more equal.” One size does not fit all. Mass customization and shared services unleash tremendous values that traditional property rights frameworks struggle to capture. Yet, we are concerned that when “everybody a trading venue, nobody a trading venue.” Opportunists will not abide by multilateral agreements when bilateral deals generate higher returns without compromising efficiency. If everybody trades or transacts on decentralized chains (distributed ledger technology), there may be no point in having any market.

The existence of markets is because there is a finite amount of goods and financial resources where effective valuations and delineate the exchanges of rights and obligations can occur efficiently. SEC Investor Protection should ONLY be applicable to countable securities (strict rule 15c3-3 around custody). The trading of those uncountable digital assets that akin to “non-cashable gambling chips” should NOT be subjected to investor protection over securities trading activities. CFTC is in a better position to regulate the trading of Spot Crypto Asset Contracts and Tokens sold via SAFT. Its authority under §2(c)(2)(D) of Commodity Exchange Act and COMEX Rule 7 help curb and mitigate situations such as the Monex case, retail metal fraud cases, and Silver Thursday event. Changes to the SEC’s OPR should steer clear of non-securities and non-exchange matters.

We do NOT desire the SEC to cross subsidize the cost to regulate crypto from equity trading. We suggest a stackable approach to create a “2-tier hierarchy” and periodically review the long-term betting odds at a securities exchange, an ATS, a Designated Commodity Market, or other Digital Assets Portals. Private activities should NOT induce harms to the public.

NMS reform needs to focus on: (i) the economics dynamics of “farmers” (asset maximizers), “hunters” (performance optimizers) and various intermediaries; (ii) reduce the need of regulatory enforcements or constant policing; (iii) to let the functioning of markets be self-managed with healthy competition, (iv) ensure the fairness and timely access to essential information where people can make educated choices, and (v) achieve sustainable grow of the overall pie.

To encourage limit orders and aggressive quoting, an “opt-out” from the trade-through rule for informed customers was previously considered but NOT adopted. Using Smart contract attestations for opt-out consent does NOT alleviate concerns about market depth. As I have said in the past, “artificially altering the queue (equal waiting line at all checkout counters, except leaving much room for the Exchanges to selectively use tier rebates and other perks to divide the cake with the elites in hurting the other “content” creators) may affect the “apparent”, NOT the real supply and demand for securities.” Depending on the SIPs/ competing consolidators increasing their bandwidth to cater for the additional data under MDIR and tick size regime, some degree of data fragmentation will happen under a decentralized consolidation model, and benchmark reference-price arbitrage will persist due to multiple-NBBOs.

It is inevitable that policy makers have to deal with capabilities differences of different trading venues. Tiered protection regimes based on investor sophistication and/or venue type is one of the possibilities, amid fragmentation would still persist, venues with lower protection standards may incentivize fleeting or non-committal quoting behavior, degrading the reliability of displayed prices. Audit trail ambiguity and timestamp arbitration would add costs and complexity to transparency and surveillance. We are concerned about its potential burden on broker-dealers.

Protection without constant policing and healthy grow of the overall pie

Our counter recommendations are as follow. Picture the Exchanges, ATSs, SIs, SDPs as different streaming platforms. Broker-dealers, and their algo developers/ traders are the content creators, like the “record labels/ publishers”, and “featured composers/ artists” in the music industry. STANDARDIZE the way different trading centers’ reward to “content creators” without pushing potential conflicts down or upstream nor rebate harvesting through phantom quotes. Let assume the existing copyright frameworks are applied to our capital markets. Order flows would be like “songs” streaming on different platforms. Broker-dealers would earn “performance royalty” on top of their trading revenue, whereas “performance royalty” in today’s term would be equivalent to access fee rebates or Payment for Order Flow (PFOF), except the incentives being standardized and available to all “content creators.” See this for further elaboration and a discussion about derivative work.

Consideration factors are: whether streamers are exploiting content creators with rent seeking behaviors; would aggregators opt for heightening prices to pass increased costs on subscribers or restricting access to cause information asymmetry. The opportunity here is – a substantial portion of traders and algorithm developers’ cost would be paid for by this Copyright mechanism, off-loading burden for participating broker-dealers.

By no mean does our proposal take anything away from the Exchanges. All streaming platforms, including Communication Protocol Systems, ought to bear royalty payments before earning appropriate subscription fees. It uses existing funding resources such as Access Fee Rebates and PFOF to realign capabilities of different venues and how incentives are paid out – NOT by volume-based tiers, but are determined by contributions to the 4Vs. This is a simpler market structure. It will help weed out conflict-of-interest, curb rent seeking behaviors, and address issues of arbitrage or a particular type of trading venue at competitive disadvantage compared to other streaming platforms.

According to Hannes Datta, George Know, and Bart J. Bronnenberg in their empirical research, “adoption of streaming leads to: INCREASES in QUANTITY of consumption … INCREASES in VARIETY of consumption… INCREASE in DISCOVERY of NEW music … Streaming revenue are climbing not only because more consumers are adopting streaming, but because consumers’ OVERALL consumption of music is GROWING as well. Streaming creates a MORE LEVEL PLAYING FIELD for SMALLER artists… Streaming EXPANDS consumers’ ATTENTION to a WIDER SET of artists… Streaming INCREASES consumer WELFARE by reducing search frictions (e.g., ENHANCING DISCOVERY) and help users DISCOVER NEW HIGH-VALUE CONTENT.”

The authors measured volume based on the number of songs (order flow) each user consumes in a given period. They measured the breath of variety consumed by users, and concentration – popularity of consumed content and calculated the concentration ratio based on each user’s own favorite top song and genres, as a share of total plays. They measured repeat consumption share for both new and known artists, calculated the ratio of top new variety plays to top overall plays over a rolling period to access chance of new artists and/or songs being ‘discovered’. “Discovery” in the context of Capital Markets, can encompass veracity in price discovery, velocity in filling orders/ finding matches, as well as discovering unknowns. Rebates in the form of standardized copyright royalties encourage contents creation and help build communities. In short, the 4Vs are essential elements to contrive a New Paradigm, where there are bigger pieces for everyone.

The partnership comes amid increased IPO activity and an expected surge of public offerings. Analysts anticipate the fastest pace of deal activity since 2021, with 40 to 60 US IPOs expected by year-end.

Founders building world-class companies deserve a world-class path to IPO. With the IPO market showing clear signs of resurgence and a robust pipeline of private companies poised for their public debut, Carta has joined forces with the New York Stock Exchange (NYSE) in a strategic partnership that designates the NYSE as Carta’s preferred public listing venue.

The strategic partnership between the NYSE, the gold standard for going public, and Carta, the leading platform for private companies, offers ambitious growth and late-stage companies a comprehensive range of pre-IPO liquidity solutions. These solutions include company-sponsored tenders, IPO-readiness tools, and unparalleled access to IPO listing services.

The partnership comes amid increased IPO activity and an expected surge of public offerings in the coming months. So far this year companies have filed 183 IPOs, a 28.9% increase from last year. Analysts anticipate the fastest pace of deal activity since 2021, with 40 to 60 US IPOs expected to raise roughly $10 billion between now and year-end.

Carta is at the center of these trends, currently serving nearly 1,000 late-stage companies, including 84% of all U.S. companies with valuations exceeding $1 billion. This extensive reach positions Carta to facilitate this critical transition for a significant segment of the private market.

“NYSE is the gold standard for going public,” said Charly Kevers, Chief Financial Officer, Carta. “Partnering with the NYSE strengthens our IPO Advisory platform and helps companies navigate one of the most complex transitions in their journey: going from private to public. Our goal is to support startups from formation to IPO with the infrastructure and partners they need to succeed.”

Michael Harris, Vice Chairman and Global Head of Capital Markets at the NYSE, said: “The IPO market continues to provide a vital pathway for private stakeholders—from venture capital and private equity investors to employees and individual shareholders—to unlock substantial value. As the world’s largest exchange group, we are thrilled to partner with Carta in offering a range of services for companies across all phases of growth.”

For Carta customers on the pathway to a public listing on the NYSE, this partnership offers a distinct set of advantages.

Carta customers that list on the NYSE can expect:

Guided, white-glove transition: Each Carta-NYSE client is paired with a dedicated NYSE Relationship Manager to provide a single point of contact and ensure a seamless transition from private company to public listing.

Seamless liquidity solutions: Carta-NYSE clients will benefit from seamless capital raising solutions including pre-IPO tenders, secondary offerings, and IPO listings.

Exclusive peer network: Companies join an exclusive community of CFOs and GCs from leading Carta and NYSE companies—pre- and post-IPO—to exchange insights and best practices in curated forums along with access to an exclusive suite of service offerings such as Board Advisory Services, Global Policy Advocacy, and select investor-focused tools.

Premier value and visibility package: Carta-NYSE clients have access to a strategic NYSE package, built to amplify their listing day and beyond with access to market data, IR tools, and governance experts.

Companies choosing the NYSE as their public listing venue will benefit from the exchange’s unparalleled track record in supporting the world’s most influential and innovative public companies. The NYSE offers access to its deep investor base, robust capital markets infrastructure, and a dedicated issuer services team that guides businesses through every stage of the public company lifecycle.

With expert support for the listing process, ongoing compliance, and post-IPO visibility, the innovative companies listing on the NYSE can expect a streamlined transition to public markets, enhanced by a rich ecosystem designed to foster growth, credibility, and long-term shareholder engagement.

New Cboe Magnificent 10 Index (MGTEN Index) will measure a fixed set of actively traded U.S.-listed stocks

Planned cash-settled MGTEN Index options to allow for nearly 24×5 and shorter-dated options trading

Launch is latest push by Cboe to meet robust retail investor appetite for derivatives

Cboe Global Markets, Inc., the world’s leading derivatives and securities exchange network, announced plans to launch futures and options on the new Cboe Magnificent 10 Index, subject to regulatory review. The new product suite will offer investors a way to gain targeted exposure to several of the most actively traded AI technology-focused stocks through cash-settled index futures and options.

The Cboe Magnificent 10 Index, launching soon, is a thematic, equal-weighted benchmark designed to measure the price return of 10 U.S.-listed large-cap stocks of technology and growth-orientated companies. The current constituents include all the Magnificent 7 stocks (Alphabet, Apple, Amazon, Meta, Microsoft, Nvidia, and Tesla), in addition to Advanced Micro Devices (AMD), Broadcom, and Palantir. The value of the MGTEN Index will be available on the Cboe Global Indices Feed via the Cboe Global Indices Channel. Cboe intends to list futures and options on the Cboe Magnificent 10 Index that will trade on a nearly 24×5 basis, providing a comprehensive suite of tools for market participants seeking to manage risk, enhance yield, and express their views on the most dynamic segment of the U.S. equity landscape.

“Both institutional and retail traders are increasingly looking for smarter ways to gain exposure to the most influential, market-moving stocks – along with tools to manage their positions and hedge risk more precisely, both intraday and around the clock,” said Cathy Clay, Global Head of Derivatives at Cboe, at the HOOD Summit in Las Vegas. “With our new MGTEN Index futures and options, we’re bringing the best of Cboe’s indexing and derivatives expertise to meet this demand. These products deliver curated exposure to a select group of high-impact stocks in a single solution – rather than managing 10 separate positions – while helping to reduce the concentration risk that may come with trading individual stocks. In particular, as market participants increasingly utilize cash-settled index options for short-dated strategies, we believe MGTEN options will similarly be a powerful tool for implementing daily trading strategies around these in-demand stocks.”

MGTEN options will be cash-settled and European-style, eliminating physical delivery and the potential for early exercise, differentiating these from options on the stock components. Along with the standard monthly A.M.-settled expirations, Cboe plans to list weekly P.M.-settled options with expiries on each trading day, offering investors across the globe the ability to trade zero-days-to-expiry (0DTE) options on the index. 0DTE trading has grown significantly in recent years as investors seek the utility short-dated options can provide, including the ability to tactically hedge, more granularly manage intraday risk, and implement daily yield-generating strategies. MGTEN options will be listed and traded on Cboe Exchange, Inc. (Cboe Options).

The planned cash-settled MGTEN futures will be listed and traded on Cboe Futures Exchange (CFE). MGTEN futures will offer a capital-efficient way to gain exposure to the most influential tech stocks through a single tradable product. Futures provide a way to diversify portfolios with inherent leverage, empowering investors to take larger positions with smaller upfront capital, while offering the precise ability to hedge, speculate, or enter a short position. Both the MGTEN Index futures and options will be cleared by the Options Clearing Corporation (OCC), potentially allowing for margin offsets.

Cboe aims to launch the MGTEN Index monthly options and futures in the fourth quarter of 2025, with the weekly P.M.-expiring options to begin trading in the first quarter of 2026, all subject to regulatory review. At launch, MGTEN Index futures and options trading will be available during regular trading hours and Cboe plans to extend availability through its Global Trading Hours at a later date. For more details on the index and its tradable products, visit the pre-launch resource hub here.

On September 8, CoinShares International, a European digital asset investment firm with approximately US$10 billion in assets under management, announced its intention to become publicly listed in the United States through a definitive business combination agreement with Vine Hill Capital Investment Corp., a NASDAQ-listed special purpose acquisition company.

Upon completion of the transaction, CoinShares will be listed on the Nasdaq Stock Market via a newly formed parent company, Odysseus Holdings, in a move designed to support its global growth ambitions and give U.S. investors enhanced access to its expanding business—particularly within the U.S. market.

The deal implies a pre-money valuation of US$1.2 billion on a pro-forma basis, positioning CoinShares among the largest publicly traded pure-play digital asset managers in the world. Traders Magazine caught up with Jean-Marie Mognetti, CEO & Co-Founder of CoinShares, to learn more.

Jean-Marie Mognetti

Beyond access to U.S. capital, what strategic advantages does the U.S. market offer for CoinShares that the European market does not?

We believe that the U.S. represents the epicenter of global digital asset innovation and institutional adoption. What we’re accessing isn’t just capital — it’s the most sophisticated ecosystem for digital asset investment in the world.

There are at least five reasons to view the U.S. as the epicenter. First, the scale is fundamentally different. The U.S. market manages 50% of the assets under management globally. We’re talking about pension funds, endowments, and RIAs managing trillions of dollars in assets that are increasingly allocating to digital assets through regulated vehicles.

Second, our view is that the investor sophistication in the U.S. runs deeper. U.S. institutional investors have been pioneers in alternative asset allocation for decades. They understand complex investment structures, they’re comfortable with innovative products, and they have the risk management frameworks to engage meaningfully with digital assets at scale.

Third, the U.S. offers something Europe simply cannot, a unified market with consistent regulatory frameworks and investment approaches. The European Union, while sophisticated, is inherently fragmented across 27 different jurisdictions, each with distinct regulations, investment vehicles, cultural preferences, and market practices. In contrast, the U.S. presents a single, massive market with harmonized standards and consistent investor behavior patterns. This unified approach dramatically simplifies product development, distribution, and client engagement at scale.

Fourth, being active in the U.S. positions us at the center of regulatory and market standard development. When new frameworks emerge, when industry standards are set, when the future of institutional digital asset management is being shaped — that’s happening in the U.S. first. Our presence here enhances our ability to influence those developments across all jurisdictions where we operate.

Finally, there’s a network effect that’s unique to the U.S. market. The concentration of institutional players, service providers, regulatory bodies, and industry infrastructure creates opportunities for partnerships and product development that simply don’t exist at the same scale anywhere else.

Our opinion is that this move positions CoinShares to lead in the most strategically important market for digital assets while we continue serving our European investor base, which remains a core part of our global strategy. We’re not replacing our European operations, we’re expanding from a position of strength to capture the largest opportunity in our industry.

CoinShares is entering the U.S. market with a strong foundation — 34% market share in EMEA and ~70% adjusted EBITDA margins. How do you plan to translate this European playbook to a very different and competitive U.S. regulatory and investor landscape?

We’re not approaching the U.S. as a copy-and-paste exercise from Europe. In fact, our strategy is fundamentally different as we are deliberately trying not to replicate what has been done in Europe because the intention here is to play an entirely different game.

In Europe, we succeeded by building the infrastructure for institutional digital asset access in a fragmented market. In the U.S., that basic infrastructure already exists through large asset management firms. They’ve done the heavy lifting on simple spot Bitcoin and Ethereum products.

Our advantage isn’t in competing with them on their terms, it’s in leveraging our decade of specialized digital asset expertise to deliver sophisticated products that we don’t believe they can build. We’re talking about advanced risk-managed indices, actively managed strategies, structured products, and yield solutions that require deep crypto-native knowledge.

The regulatory environment and investor expectations are indeed different, but that actually works in our favor in our view. U.S. institutional investors are more sophisticated in their appetite for complex alternative investment structures. They understand and demand the kind of innovative products that traditional asset managers will likely struggle to develop because crypto isn’t their core competency, as it is ours.

While big ETF firms have scale, they don’t have eleven years of crypto-specific research capabilities, operational infrastructure, or product innovation expertise that we have. We’re not trying to beat them at asset gathering, we’re creating products they cannot easily replicate because they lack our specialization.

Our European success provides the operational foundation and financial discipline, but our U.S. strategy is about being the digital asset specialists in a market dominated by generalists. We’re responding to market demand, building local partnerships, and ensuring full regulatory compliance, but we’re doing it to deliver sophistication that only a niche, purpose-built digital asset manager can provide.

The SPAC deal values CoinShares at a notable discount compared to peers like BlackRock and Grayscale, at 7.3x EV/EBITDA vs. 20.9x. Was this pricing a strategic decision to attract U.S. investors, or a reflection of macro uncertainty around digital assets?

This valuation represents a significant improvement from where we were trading in Sweden, which we believe to be substantially undervalued. The 7.3x multiple you’re citing actually reflects our strategic positioning rather than any discount to our intrinsic value.

In our view, ther undervaluation in Sweden is largely a function of the venue itself. The Swedish market relative to the US is a small, local market that isn’t particularly digital asset-friendly and, frankly, isn’t very suspportive of non-Swedish companies. The Swedish market simply doesn’t have a deep investor base or the institutional understanding of digital assets necessary to properly value a specialized firm like ours. The digital asset management industry is still in its early innings, and we are excited by the opportunity to introduce our capabilities and differentiated offerings to a broader base of investors in the U.S.

You’re targeting the U.S. market at a time when sentiment toward crypto is recovering and regulatory clarity is improving. What specific product launches or growth initiatives are planned post-listing to capitalize on this momentum?

We’re entering at an inflection point where the infrastructure work is largely done, and now it’s about sophistication and specialization. Our post-listing strategy focuses on three key areas where our digital asset expertise creates genuine competitive advantages.

First, we’re launching U.S.-domiciled products that go well beyond basic spot exposure. Think advanced risk-managed indices, actively managed strategies that can navigate crypto market cycles, and structured products that provide different risk-return profiles. These aren’t products you can build overnight, they require years of crypto-specific research and operational expertise that traditional asset managers simply don’t possess.

Second, we’re expanding into areas where we already have proven European capabilities but can tailor them specifically for U.S. regulatory and investor requirements: staking solutions, yield-generating strategies, and derivative products that provide leverage or hedging capabilities.

The key difference is that we’re not launching these products to compete with generalist asset managers’ spot Bitcoin ETF. Rather, we’re creating solutions for institutional investors who’ve already made their basic crypto allocation and now want more sophisticated exposure. When a pension fund wants to understand liquid staking derivatives or implement a systematic crypto rebalancing strategy, they need specialists who’ve been doing this for a decade.

The improving regulatory environment and market sentiment create the perfect backdrop for institutional investors to move beyond basic exposure into the more nuanced products where our specialization really matters.

Given your substantial recurring revenue and strong free cash flow, do you envision future M&A to accelerate your U.S. expansion, or will the focus remain on organic growth and product development?

Our approach will be both pragmatic and opportunistic. The SPAC transaction provides us with a committed institutional equity investment that supports our organic U.S. scale-up while maintaining significant firepower for strategic acquisitions that can accelerate our market penetration.

We’re not looking at M&A as a substitute for organic growth, it’s a complement to it. Our primary focus remains building our own U.S. operations, launching sophisticated products, and establishing direct relationships with institutional clients. That’s where our core competencies lie, and that’s what will drive sustainable value creation.

However, the digital asset management industry remains highly fragmented, particularly in the U.S. There are numerous smaller players with specialized capabilities, regulatory licenses, or distribution relationships that could significantly accelerate our market access. We’re specifically interested in targets that bring three things: expanded regulated distribution channels, complementary institutional infrastructure like custody capabilities, or specialized product development expertise that enhances our offering.

The key criterion is clear value creation for shareholders. We’re not interested in acquisitions for the sake of scale — we want deals that either compress our time to market, add capabilities that are difficult to efficiently build ourselves, or strengthen our regulatory positioning in ways that create lasting competitive advantages.

Our strong balance sheet and cash generation give us the luxury of being selective. We can pursue organic growth while remaining prepared to move quickly on attractive strategic opportunities. The U.S. market is large enough to support multiple approaches simultaneously — organic product launches, partnership development, and targeted acquisitions where they make strategic sense.

This balanced approach reflects our decade of experience building market-leading positions through disciplined capital allocation.

(FLASH FRIDAY is a weekly content series looking at the past, present and future of capital markets trading and technology. FLASH FRIDAY is sponsored by Instinet, a Nomura company.)

Robinhood is having a good week.

First, HOOD stock has gained about 20% on news that the retail brokerage will be added to the benchmark S&P 500 Index.

Second, Robinhood apparently had a successful HOOD 2025 Summit in Las Vegas. Traders Magazine has never attended the event (perhaps our invitation got lost in the mail?), but it seems like a mini-version of Berkshire Hathaway’s annual shareholder meeting in Omaha, Nebraska – i.e. a brand- and loyalty-building confab of people connected to one enterprise, all networking and talking shop under one roof.

At HOOD 2025, Robinhood announced various new trading products meant to improve the user experience of its core customers – active traders.

We found the most interesting product to be the first one announced: Robinhood Social. The company says Robinhood Social will be a community where users can follow other Robinhood traders, swap strategies, discuss market performance, and “trade with clarity.”

But wait. Online social networks for stock trading have been around for a long time, since the advent of the internet really. Yahoo! message boards were all the rage in the late 1990s / early 2000s when the stock market was hot and retail traders were piling in.

So the concept is the same. But the difference between Yahoo! Message boards and Robinhood Social can be expected to be as vast as the difference between trading 25 years ago and trading now.

The Traders Magazine Editor is old enough to remember the Yahoo! boards, and even being persuaded suckered into buying a dinky biotech stock named Cytogen (CYTO), which some posters insisted was the next big thing. (The bad news I got hosed; the good news is I was in my 20s and my risk capital was maybe a few thousand bucks.)

A 2021 Yahoo! Finance article recounts those days. Yahoo! and other boards “served as open forums for investors to anonymously float ideas during the dot-com bubble that popped in 2000. And just as the myriad of dot-com stocks included stories of fraud, so did posts on message boards, where some furious posters met their fates with the Securities and Exchange Commission (SEC).”

Trust and credibility were lacking, to understate it, 25 years ago. That’s one of the aspects that will be way different with Robinhood Social, where users can “Check 1 year and daily P&L, profit rate, and dive into past trades for the people you’re most interested in … you can trust that every customer profile belongs to a real person, verified through KYC.”

To be sure, Robinhood Social is hardly the only offering of its type – Reddit and StockTwits are just two of the established stock-trading networks. But those firms aren’t brokers – Robinhood has the advantage of being a one-stop shop for traders looking to trade and to exchange information. So Robinhood Social will have a built-in network of potential users when it rolls out next year.

Since its founding in 2013, Robinhood has expanded its customer base to 27.4 million funded accounts, of which 75% are Gen Z or Millennials. So the company has a blueprint for success, and if Robinhood Social were its own standalone stock, Traders Magazine would rate it BUY.

Doug Petno, co-chief executive of the commercial & investment bank at JP Morgan, expects markets and investment banking revenues to increase in this quarter.

Petno spoke to analyst Jason Goldberg at the Barclays Global Financial Services Conference on 9 September 2025 in New York. The commercial & investment bank business includes global markets, payments and security services, and was nearly half, 43%, of group revenues and 46% of net income in the first half of this year, according to Goldberg. The division generated $19.5bn in revenues just in the second quarter and does business with more than 90% of the Fortune 500 in over 60 countries.

Goldberg said: “That would be the fifth largest bank in the United States if that was a standalone company, and would be bigger than both Goldman Sachs and Morgan Stanley’s entire operation.”

Petno argued this gives the bank a “tremendous” lens on the wholesale market and economy and clients are trying to see through the fog of geopolitical, market, trade, legislative and regulatory uncertainty. He highlighted that it was positive that most of the bank’s clients are either innovating, navigating, evolving or adapting to the volatility created by uncertainty around global trade and some of the fog is lifting.

As a result clients are thinking about accelerating capital investment and Petno said that is manifesting itself in the bank’s credit performance and credit costs, and market activities across capital markets and M&A.

Doug Petno, JP Morgan

“Our markets team is doing extremely well,” added Petno. “They are on track to have a terrific year and the momentum from the first half of this year is extended into the third quarter.”

The bank is seeing broad-based strength across equities and fixed income, commodities and currencies. In addition, the initial public offering market, which Pento described as “completely on its back” in 2022, has come back and JP Morgan has a lot of primary issuance in its pipeline. He expects equity capital markets to continue to be robust, and said the technicals in debt capital markets are “really strong” as spreads are historically tight, so clients are taking advantage of open credit markets.

There are a few weeks left in the third quarter and Pento estimated that markets revenue will increase in the high-teens percentage rate. Goldberg said: “That would put 2025 at a record level for markets revenues.”

M&A

Investment banking is having a “pretty good” year with one of the busiest summers, including the busiest August in a long time, according to Pento. Based on the bank’s pipeline, he expects investment banking revenues for the third quarter to rise by a low double-digit percentage.

“Anything can happen but we feel there’s a lot of animal spirits at the moment,” said Pento. “Big M&A is back as there is a strategic imperative to be global, big, diversified and integrate operations. There is also a sense that you have a finite window to complete large M&A before the regulatory sentiment may shift back.”

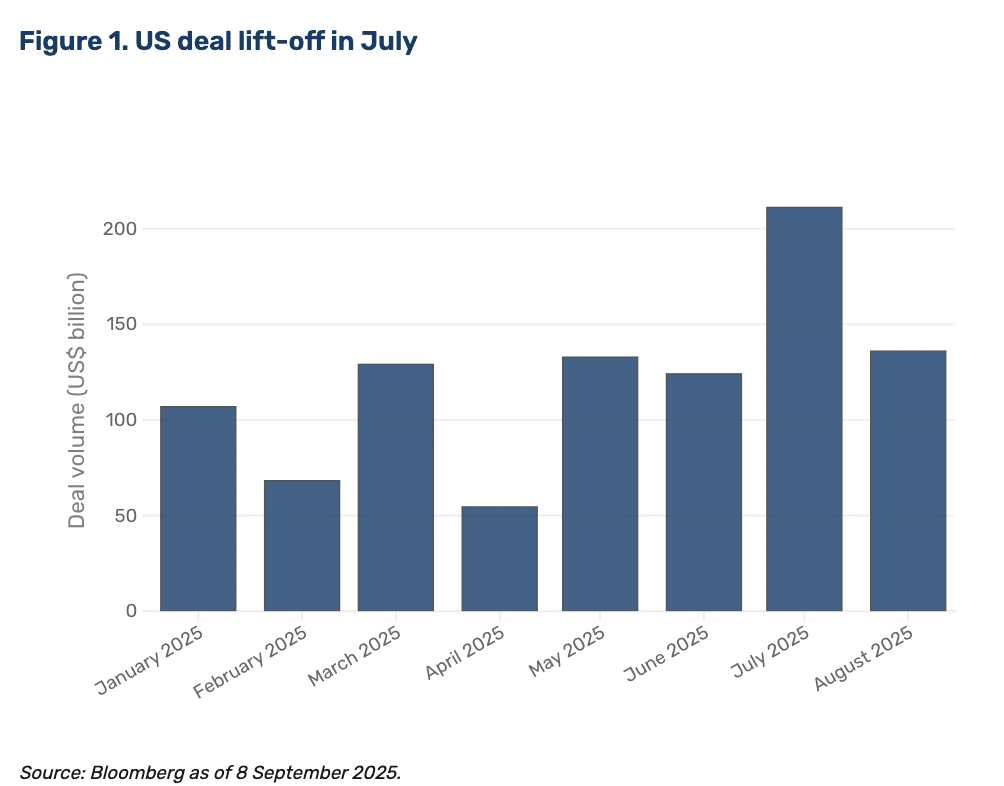

Nick Wilcox, managing director, discretionary equities at hedge fund Man Group, said in a blog that there are finally tangible signs that the long overdue acceleration in M&A is finally underway.

“Global M&A has hit over $2 trillion year-to-date, an increase of more than 30% from last year,” he added. “July alone delivered North America’s strongest month since September 2021, and the third-strongest July on record.”

Source: Man Group

Wilson said that while industrials and technology led the initial charge, dealmaking is now spread across most industries and geographies. In addition, a higher percentage of deals are attracting competing bids, fewer deals are facing shareholder opposition and antitrust risk is lower under the current U.S. administration.

He expects deal momentum to continue absent major macroeconomic disruptions as companies have built up cash reserves and strategic rationales during the quiet years and private equity firms are sitting on record levels of dry powder.

“Crucially, the regulatory and political backdrop has shifted in favour of dealmaking,” said Wilson. “The M&A machine appears to finally be hitting its stride.”

Private credit

Pento described private credit as a “tremendous market” that has grown dramatically in the last several years to a multi-trillion dollar market, which is over half of commercial and industrial lending. However, he warned that banks that have grown loans at over 20% for an extended period of time tend not to do well.

“There will certainly be winners and losers in this asset class over time,” Pento added.

He argued that JP Morgan is not so worried about the outstanding players in private credit as many are clients of the bank. However, secondary and tertiary players have not been through a hard recession so may suffer idc there are two or three quarters with a tough economic climate.

Jim Zelter, Apollo

Jim Zelter, president of Apollo Global Management, a provider of alternative assets and retirement solutions, also spoke at the Barclays Global Financial Services Conference on 9 September 2025 in New York. Zelter agreed that not all alternatives managers will be successful.

In order to compete, Zelter said firms need broad distribution, to be able to price products, low operating costs, a highly rated counterparty balance sheet and “massive” origination.

“There are lots of folks who have entered the marketplace who think they will be able to sustain a mid-teens return on equity, and we scratch our heads a little bit,” adde Zelter. “The success of a few of us means there are a lot of imitators, but that does not mean they are going to have success over time.”

He continued that he does not want to say there is an arms race, but people see the benefits of scale players, which is why Apollos is “very confident” on delivering its five year plan. Zester said: “We have a lot of momentum behind our back.”

Zelter also agreed with Pento on the macroeconomic environment and as a result, he said M&A is having its second best year on record.

“If someone landed from Mars today, and notwithstanding all the headlines, said let’s take a look at the macro economy, you have got a major capex cycle,” added Zelter. “Personal and corporate balance sheets are in pretty good shape.”

Zelter said that since he arrived at Apollo 20 years ago, private credit has become a permanent allocation in portfolios.

“We just see more defined contribution plans, global wealth plans, wanting to diversify their exposure,” he said.

He gave the example that Apollo has been working with State Street Investment Management to expand investor access to private market opportunities. In February this year the two firms launched SPDR® SSGA Apollo IG Public & Private Credit ETF (PRIV), the first ETF to offer exposure to both private and public exposures in one fund.

On 10 September State Street Investment Management said in a statement it had launched the State Street Short Duration IG Public & Private Credit ETF (PRSD). The fund is an actively managed short-term core bond solution, primarily allocating to investment grade debt securities through public and private credit instruments, seeking to maximize risk-adjusted returns alongside current income for investors.

Anna Paglia, State Street Investment Management

Anna Paglia, chief business officer of State Street Investment Management, said in a statement that private credit is one of the fastest-growing segments of the market but has historically been an underutilized allocation in portfolios.

“That changed earlier this year when we launched PRIV – a core bond fund offering exposure to a combination of investment-grade public and private credit ETF,” she added. “Now, PRSD builds on the launch of PRIV and continues the convergence of public and private markets by expanding our lineup to include a short-term bond strategy that can be used to pursue potential excess returns while managing duration risks.”

Apollo believes that the traditional 60/40 portfolio allocation of 60% equities and 40% fixed income will change to include alternatives. Zelter added: “We are going to have a bigger seat at the table.”

In fixed income, Zalter said investors have allocated to a narrow definition of private credit – direct lending to non-investment grade sponsors. However, Apollo sees the the largest area of institutional as well as insurance company activity into private credit as the whole asset-based finance business due to corporates’ capex needs and the changes in how banks are using their balance sheets.

“In terms of scale of market opportunity, I suspect that the direct lending marketplace will be surpassed three or four times over by the end of this decade by private credit in the asset-based world,” added Zelter.

Apollo has estimated that the private credit universe is a $40 trillion opportunity with the investment grade segment becoming “massive” multiples of the non-investment grade side of the business. In addition, most scaled origination has occurred in the non-investment grade segment but over the next decade investment grade industries, such as AI and data centres, who have massive capex needs.

Jamshid Ehsani, Apollo

For example, Apollo said in a statement on 8 September 2025 that it had agreed to commit €3.2bn of equity to a newly established joint venture with RWE, Germany’s largest power producer and a global leader in renewable power generation.

Jamshid Ehsani, partner at Apollo, said in a statement: “This partnership reflects Apollo’s commitment to strong, lasting partnerships across both the private and public sectors. Looking ahead, we expect to further accelerate our investment activity in Europe, with a particular focus on Germany, France, Italy and the UK.”

The World Federation of Exchanges (WFE), the global industry group for exchanges and clearing houses, has published a paper analysing the implications of lengthening equity market hours. It assesses both the opportunities and the operational, technological, and regulatory challenges this shift requires, especially as you get closer to round-the-clock trading.

The paper, titled “Policy and Market Impacts of Extended Trading”, traces the evolution of trading hours and presents near round-the-clock trading as a whole new model, with several issues to consider. Extended trading hours – typically 22/5 or 23/5 as opposed to 24/7 – is technologically feasible and in some cases aligns with investor demand. Nevertheless, its adoption must be carefully calibrated to preserve market integrity, investor protection, and systemic stability.

Key considerations highlighted in the paper:

Investor demand: Local and overseas investors are seeking access beyond traditional hours. The greatest demand is currently for major US stocks during Asian hours.

Market considerations: Extended trading may affect liquidity which should be disclosed to retail investors. Market operators should consider how to maintain market controls overnight. Markets will still likely require a closing or reference price for benchmarks, settlements, and corporate actions.

Operational demands: Exchanges, clearing houses, and brokers must adapt systems for high availability, real-time risk controls, and continuous surveillance.

Post-trade requirements: Market participants must adapt systems to handle 24/7 data feeds and post trade processing, strengthen supervisory frameworks, and manage risks associated with low-liquidity periods. Real-time margin recalculation and funding access outside normal banking hours are required.

The WFE concludes that:

Extended trading is not inevitable nor universally desirable. Different markets will adopt different models depending on their liquidity, structure, and participant needs.

It is important to consider something that is too easily forgotten: the needs and wishes of issuers of securities. 22/5 or 23/5 models offer a pragmatic path forward. They allow exchanges to meet rising demand while testing operational readiness before moving toward continuous markets.

True 24/7 trading would represent a system-wide transformation. It requires the re-engineering of post-trade processes, governance frameworks, and supervisory oversight.

Inaction carries risks. Regulatory inertia could cause investors to migrate to less transparent, unregulated venues, undermining market integrity and investor confidence.

Nandini Sukumar, CEO of the WFE, said, “This paper is not a prescription for 24/7 markets, but a blueprint for how to get there if markets choose to. The shift to extended trading is technologically feasible and already aligned with investor behaviour in other asset classes. The real question is how markets evolve in a way that protects investors, supports integrity, and strengthens global competitiveness. Any shift must be ecosystem-wide, coordinated across custodians, settlement banks, brokers, and regulators.”

Richard Metcalfe, Head of Regulatory Affairs, said, “Flexibility and diversity in trading models should be encouraged, with trading hours remaining the responsibility of market infrastructures. Regulators should focus on enabling innovation while maintaining the fundamental principles of fairness, transparency, and systemic stability.”

The full paper can be read here. The WFE continues to work further on this topic and will soon be publishing a research paper.

As the U.S. financial markets continue to adapt to the accelerated T+1 settlement cycle, market participants are turning to automation and innovative workflows to meet the new demands.

Val Wotton

“The U.S. move to a T+1 settlement cycle was enabled by extensive industry-wide preparation and advanced automation including the adoption and use of CTM, DTCC’s automated central trade matching platform,” said Valentino (Val) Wotton, Managing Director and Global Head of Equities Solutions at DTCC.

On September 9, 2025, The Depository Trust & Clearing Corporation (DTCC), announced that BNP Paribas and J.P. Morgan have joined CTM’s automated tri-party matching workflow for prime brokers.

This solution streamlines trade communications between hedge funds, prime brokers, and executing brokers, bringing “greater levels of efficiency” to the global markets— as the UK, EU, Switzerland and Liechtenstein prepare for the move to T+1 settlement by October 2027, according to DTCC.

Today, many prime brokers often receive trade details from hedge funds in various formats and at different times which can extend to T+1, causing delays in post-trade processing, according to DTCC.

According to Wotton, DTCC’s CTM tri-party matching workflow is currently only available in non-U.S. securities markets.

“However, U.S.-based hedge funds that trade in international markets will see the benefits of this automated workflow having been adopted by their non-U.S. based prime brokers, in this case BNP Paribas and J.P. Morgan,” he said.

“The workflow leverages CTM’s automated central matching functionality and provides prime brokers with a golden copy of transaction details when a trade match between a hedge fund and an executing broker takes place, bringing real-time standardization and automation to the trade allocation process,” he added.

By leveraging CTM’s automated central matching functionality, the workflow provides prime brokers with a “golden copy” of transaction details when a trade match takes place between a hedge fund and an executing broker, Wotton said. This “golden copy” becomes the shared, validated version of the trade, eliminating inconsistencies and enabling real-time transparency across all stakeholders.

“Today’s post-trade environment is still heavily fragmented, especially when it comes to trade allocation and communication between hedge funds, executing brokers, and prime brokers,” Wotton explained. “Our tri-party workflow solves this by synchronizing and automating trade communications in real time, ensuring all parties are working off a golden copy of the trade.”

The CTM platform also directly supports straight-through processing by integrating with front-, middle-, and back-office systems, as well as downstream solutions like DTCC’s ALERT database of over 16 million golden source Standing Settlement Instructions (SSIs).

Wotton said that one of the most critical needs in a T+1 environment is same-day affirmation (SDA), the process where trade details are affirmed by all parties within hours of execution—on trade date (T+0). According to Wotton, CTM’s Match to Instruct (M2i) workflow was designed specifically to address this requirement in the U.S. market.

“M2i simplifies what was traditionally a multi-step, manual process,” Wotton explained. “It connects allocation matching in the middle office with confirmation affirmation in the back office, effectively enabling auto-affirmation. Our clients using M2i are consistently hitting nearly 100% SDA rates.”

The impact of automation on post-trade processing has been transformative. “The U.S. move to a T+1 settlement cycle was enabled by extensive industry-wide preparation and advanced automation, including the adoption of CTM,” Wotton said.

“Since the transition, we’ve seen a $3 billion reduction in the clearing fund, a 98% netting efficiency rate, and fail rates that remain consistent with the prior T+2 environment,” he told Traders Magazine.

According to Wotton, currently, U.S. markets are experiencing SDA rates of 95% or more—higher than under T+2—and fail rates between 2–3% in both CNS and non-CNS environments. These results suggest that the combination of centralized matching, automation, and validated trade data is critical to maintaining stability under tighter timelines.

The benefits of CTM extend beyond the U.S., particularly as international markets prepare for T+1 adoption. The tri-party workflow will eventually introduce central clearing capabilities in the U.K. and E.U., unlocking similar netting and clearing opportunities already available in the U.S, he noted.

“As trading volumes grow and global markets move towards shortened settlement cycles, scalability and resilience in post-trade operations will become even more critical,” Wotton said. “Our tri-party workflow lays the groundwork for central clearing capabilities in international markets. We’re working toward introducing netting and clearing opportunities in the U.K. and EU that mirror those in the U.S.”

CTM’s role in creating a more resilient global infrastructure is particularly timely, Wotton noted. With the golden copy acting as a single source of truth for all trade counterparties—and SSIs automatically enriched via ALERT—firms can reduce operational friction, eliminate last-minute reconciliation, and speed up processing from execution to settlement, he said.

“In today’s environment, the margin for error is shrinking while the volume of trades continues to grow,” Wotton said. “By eliminating manual handoffs and standardizing trade data at the point of execution, we’re giving the industry the tools it needs not just to adapt—but to thrive in a T+1 world and beyond,” he added.

Wotton sees the tri-party workflow not just as a short-term solution, but as a critical foundation for the future of global post-trade operations. “T+1 is just the beginning. We’re building solutions that not only meet today’s regulatory requirements but position the industry for a more automated, efficient, and scalable future,” he concluded.

37% have experienced losses due to unhedged FX risk

Over half are increasing hedging ratios and lengths to manage dollar volatility

London, 10th September 2025 – A new report from advanced FX and cash management solutions provider MillTech, has revealed that amid rising dollar volatility, the vast majority (85%) of North American fund managers now hedge their forecastable currency risk, up from 79% last year and 72% in 2023.

The MillTech North American Fund Manager CFO FX Report 2025 analyses the findings from a survey of 250 senior finance decision makers at funds across the US and Canada, revealing how they are changing their hedging strategies in response to politically driven dollar volatility, and leveraging AI and automation in their FX processes.

The dollar experienced its worst first-half performance since 1973, weighed down by aggressive US trade policies, rising fiscal concerns, and expectations of Fed rate cuts, posing significant uncertainty for fund managers. While 99% said their returns had benefited from these politically driven swings, over a third (37%) say they’ve suffered losses due to unhedged FX risk, and 99% report concerns over the impact of dollar volatility on foreign market exposure. Of those currently not hedging, 70% are now considering doing so due to current market conditions, a huge increase from only 16% in 2024.

Despite the increase in the number of funds hedging, the mean hedge ratio dropped to 45% from 55% in 2024, while hedging lengths shortened to 5 months from 5.4 months. However, in response to rising volatility, 54% are increasing their FX hedging ratios, while 52% are extending hedging lengths. These are both defensive moves to protect a larger part of their exposure and lock in certainty for longer.

Nearly all (99%) of fund managers surveyed reported huge increases in the cost of hedging, with 58% reporting cost increases of between 50% and 100%, and 5% saying their costs had risen over 100%. The average increase was 57%. Two in five (41%) funds that don’t hedge cited costs as the primary reason for opting out.

Other key findings include:

Biggest tariff concerns – Counterparty risk in hedging transactions (41%), the impact of policy changes on currency values (35%) and increased volatility (34%) were the top US tariff concerns.

Increased option adoption – Nearly every fund surveyed (95%) has increased its use of options, showing that they are finding new ways to manage the increasingly volatile dollar.

Shifting priorities – Automation of manual processes and transparency of costs were the top priorities for North American corporates (40%), as opposed to the credit ratings of FX counterparties (36%) and uncollateralised hedging (39%), which were top in 2024.

Top products for hedging FX risk– Currency swaps (53%) and FX swaps (52%) were the top products used for FX hedging, followed by spot transactions (48%) and options (42%).

Key challenges in 2025 – Fund managers’ biggest challenges when handling FX operations in 2025 were fragmented service provision (36%), securing credit lines (35%) and demonstrating best execution (34%).

Key processes outlined for automation – Fund managers were most keen to automate settlement (49%), price discovery (47%) and risk identification (46%).

Fierce appetite for AI – North American fund managers are rapidly adopting AI, with 42% already using the technology and 35% aggressively looking at how AI can create efficiencies.

Outsourcing – All (100%) fund managers surveyed were outsourcing some part of their FX processes, with the main motivations being access to specialised expertise (36%), risk management and compliance (34%), and scalability and flexibility in operations (32%).

“The good news is that for many fund managers, FX risk management has moved to the top of the agenda. There is now broad recognition that well-executed hedging strategies can protect margins and cushion against unexpected losses. At the same time, outsourcing FX operations to experienced providers offers access to specialist expertise, greater efficiency, and full transparency. In a market where a single currency move can erase months of gains, proactive FX management is no longer optional; it is essential to preserving performance and investor trust.”

MillTech provides advanced FX and cash management solutions to increase market access, reduce costs and automate manual workflows.

With a focus on automation, integration and connectivity, MillTech has pioneered an independent risk management and liquidity solution for fund managers, institutions and global corporates, which is purpose-built to deliver best execution at scale.

MillTech provides an end-to-end operational workflow that enables automation, standardisation and cost transparency on all FX transactions and cash movements.

Its highly secure platform centralises all client FX to enhance oversight whilst increasing control, all at no additional cost. It offers quick onboarding routes, multi-bank best execution and hedging management services.

Headquartered in London, the world’s largest FX hub, MillTech provides services to clients in the United Kingdom, United States, Canada, Switzerland, Belgium, Denmark, Ireland, Luxembourg, Norway and Liechtenstein. MillTech is authorised and regulated by the UK’s Financial Conduct Authority (FCA FRN 911636) and registered with the USA’s National Futures Association (NFA).