Equities Leaders Summit returns February 2025 (3–5), hosted at the beautiful JW Marriott Marquis in Miami!

As the leading buy-side-focused equities trading gathering in the U.S., Equities Leaders Summit is where strategies are shared, ideas are exchanged, and the future of trading is shaped.

Check out the agenda to see the hot topics we’re bringing to the forefront and the interactive experiences waiting for you this February.

Equities Leaders Summit 2025 Highlights:

Join senior buy-side attendees representing leading asset managers, hedge funds, pension funds, wealth managers, and investment banks.

Participate in buy-side-driven sessions led by 20+ heads of equities trading and trading analytics to gain actionable insights for evolving your execution strategies and future-proofing your equities desk.

Engage in unmatched face-to-face networking with 400+ attendees, including major buy-side, sell-side, and cutting-edge technology providers.

Key Topics Include:

Unlocking Alpha with AI: Transforming Equities Trading through automation and advanced analytics.

Liquidity Sourcing in the ever rapidly evolving financial landscape: Dive into the latest developments and emerging trends.

DE&I in Trading: The next phase in elevating impact and outcomes.

Global Macro Predictions: 2025 and beyond.

Don’t miss this opportunity to join the most influential voices in equities trading at the ONLY event that brings the entire ecosystem under one roof.

Buy-Side can attend the event for free.

Register here to secure your place at Equities Leaders Summit 2025!

Bloomberg survey of 200+ market participants reveals industry focus on automation and real-time data to drive front office efficiencies and manage complex market dynamics

NEW YORK, Dec. 11, 2024 /PRNewswire/ — Financial institutions are turning to new technologies to stay competitive amid growing geopolitical tensions and evolving market dynamics, according to a new survey conducted by Bloomberg. The survey polled over 200 senior industry participants during Bloomberg’s Managing Risk and Valuation six-part event series held throughout North America in the second half of 2024.

Fragmented risk assessments

Survey response from Bloomberg’s Managing Risk and Valuation event

As markets navigate an increasingly unpredictable global landscape, the survey showed geopolitical risk is a rising priority, with over one third of respondents (34%) deeming it their top concern in the next 1-3 years. Beyond immediate exposures, firms are broadening their attention to encompass secondary impacts, such as supply chain vulnerabilities (19%), while also gearing up to address emerging risks associated with AI and cybersecurity (19%).

While risk teams are keen to manage these complex emerging risks, the survey showed that many firms struggle to confidently assess traditional financial risks. For example, respondents are fairly divided on the current state of market liquidity, with nearly half (43%) saying overall market liquidity has not changed in the past six months, but 18% are stating it is worse and 23% are stating it is better. Similarly, firms are taking divergent approaches to enhance their credit risk frameworks in response to market events of the past few years. Nearly a quarter (26%) are still considering making changes, while another quarter are looking to automate manual tasks (24%), add additional early warning indicators (21%) and conduct scenario analysis (21%).

“Financial institutions face a diverse set of challenges: geopolitical uncertainty, inconsistent liquidity assessments and legacy credit risk frameworks. Like a sophisticated radar system, firms need data and technology that cut through the noise to deliver actionable insights.” said Zane Van Dusen, Bloomberg’s Global Head of Risk & Investment Analytics Products. “That’s why solutions like Bloomberg’s Liquidity Assessment solution (LQA) which uses explainable machine learning models, Default Risk (DRSK), and Market Implied Probability of Default (MIPD) are important tools not just for managing risks, but for driving smarter investment strategies in volatile markets.”

AI in the front office is coming into focus

With an eye toward automation, the survey found that nearly a third (32%) of respondents are utilizing AI in the front office, gaining an edge through automation and faster insights. This shift points to a growing competitive divide, with early adopters poised to capture new efficiencies and advance trading advantages – a reflection of AI’s escalating role in transforming the financial sector.

The survey also highlighted streamlining trading workflows as a priority, with over a third (36%) of respondents selecting better execution as their main reason for using real-time bond pricing, followed by portfolio and ETF trading (26%) and minimizing tracking error (21%).

“The rapid electronification of credit markets and the growing adoption of fixed income ETFs with custom baskets is revolutionizing credit markets. Consequently, the front office increasingly requires real-time pricing to drive credit algos, price and execute basket and portfolio trades, and assess real-time portfolio exposures and risk,” said Eric Isenberg, Bloomberg’s Global Head of Enterprise Data Pricing. “We developed IBVAL Front Office to address this need with pricing nearly every 15 seconds for approximately 45,000 bonds in the USD, GBP, and EUR credit markets.”

Together, these findings underscore a growing need across the industry for real-time data, AI-driven insights, and geopolitical risk management tools. As firms look to streamline workflows and mitigate risks, Bloomberg’s comprehensive suite of solutions are equipping industry participants with the capabilities to stay ahead in an era defined by complex global pressures and fast-moving markets.

To view the full results of the survey, please click here.

About Bloomberg Bloomberg is a global leader in business and financial information, delivering trusted data, news, and insights that bring transparency, efficiency, and fairness to markets. The company helps connect influential communities across the global financial ecosystem via reliable technology solutions that enable our customers to make more informed decisions and foster better collaboration. For more information, visitBloomberg.com/company orrequest a demo.

Leverages Nasdaq’s advanced and trusted platform to offer market participants an industry-leading trading experience

PEAK6 Investments is excited to reveal plans for the launch of Bruce ATS, an Alternative Trading System (ATS) aimed at revolutionizing overnight trading, operated by Bruce Markets LLC (“Bruce ATS”). This upcoming platform, subject to regulatory approval, offers investors reliable and secure access to U.S. markets after traditional trading hours. It is built using Nasdaq’s industry-leading technology to provide efficient, robust, and fair trading.

Bruce ATS™ emerges from collaboration with industry veterans and insights from early adopters who identified the need for an enhanced overnight trading solution. The founding team comprises senior leaders with extensive expertise across the trading industry, ensuring advanced technology that can provide an elevated trading experience.

“The launch of Bruce ATS is a game-changer in the trading landscape,” says Bill Capuzzi, PEAK6 Partner and CEO of Apex Fintech Solutions. “With decades of industry experience and well-established reputation for reliability, we are not just meeting the needs of today’s investors—we are setting the standard for tomorrow’s market experience. Our commitment is to open new doors, empowering investors with continuous, seamless engagement, and ensuring they can act on market movements anytime, anywhere.”

The new system is planned to be available for trading from Sunday through Thursday, 8:00 PM EST to 4:00 AM EST, with plans to expand availability in the future.

Key Features of Bruce ATS™:

Robust and trusted trading platform

Streamlined access via industry proven APIs for order management and market data

Expertise in managing corporate actions to reduce order cancellations, and minimizing trade failures

“There is growing appetite for longer trading hours amongst global investors, and we’re excited to collaborate with Bruce ATS to help establish and grow this important market,” said Magnus Haglind, Senior Vice President, Marketplace Technology at Nasdaq. “Our trading technology has long been used to support 24/7 trading in digital asset markets and we’re pleased to expand this service across a broader range of asset classes.”

Bruce ATS™ is not just changing timeframes, but also expanding possibilities for investors worldwide:

Servicing East Asian and South Asian markets: Offering morning access to U.S. markets for cities like Mumbai, Beijing, and Seoul

Appealing to a wide range of investors: Meeting the demand for non-traditional trading hours, appealing particularly to new investors

Aligning with crypto-based expectations: Moving towards enabling 24/7 availability that crypto traders expect as they shift to investing in traditional securities

“Seamless integration with Apex Fintech Solutions’ platform ensures users have a powerful and user-friendly trading experience,” says Connor Coughlin, Chief Commercial Officer at Apex Fintech Solutions. “With the upcoming launch of Bruce, we’re excited to announce that Apex clients will have day one access to this innovative trading platform, underscoring our commitment to providing our clients with cutting-edge financial solutions that enhance their trading flexibility and accessibility.”

Upon regulatory approval, Bruce ATS™ intends to set a new benchmark in after-hours trading by leveraging its deep industry expertise in brokerage, clearing, corporate actions, and compliance, supported by the stability of renowned entities capable of managing extensive trading volumes.

Bruce Markets LLC (“Bruce”) is a registered broker-dealer and member of FINRA and SIPC. Subject to regulatory approval, Bruce intends to operate an Alternative Trading System (ATS) which provides liquidity and execution services in NMS stocks during the hours of 8:00 p.m. to 4:00 a.m. ET. FINRA BrokerCheck report for Bruce ATS are available at: https://brokercheck.finra.org/firm/summary/300209

New AI Feature Provides Condensed Market Insights, Saving Time and Boosting Efficiency

GREENWICH, CT, December 11, 2024 – Interactive Brokers (Nasdaq: IBKR), an automated global electronic broker, announced the introduction of AI-generated news summaries to its News & Research offering. This advanced feature, available at no additional cost, enables clients to access concise summaries of news articles, streamlining insights from leading providers and making it easier for investors to stay informed.

Leveraging the power of AI, this tool extracts market-relevant information, allowing clients to quickly scan for important updates and giving them more time to make informed decisions and manage their portfolios. This, along with the ability to filter news related to stocks in portfolios and watchlists, makes it easy for users to stay updated on coverage directly impacting their investments.

“Artificial intelligence enables us to deliver valuable insights in seconds, helping our clients understand how breaking news may affect their portfolios,” said Steve Sanders, EVP of Marketing and Product Development, at Interactive Brokers. “Our AI-generated news summaries feature gives investors a powerful way to pinpoint the information that matters most, making research fast, accessible, and impactful.”

The AI-generated news summaries feature is available to eligible clients of the Interactive Brokers affiliates in Canada, the UK, Ireland, Hong Kong, Singapore, Australia, and Japan. Interactive Brokers is discussing with its regulators a potential expansion of AI-generated new summaries to clients of IB LLC.

In addition to AI-generated news summaries, Interactive Brokers enhanced its Hot News feed to utilize AI to tag articles as notable. This feature is available to all clients worldwide.

For additional information about the AI-generated news summaries, please visit:

Interactive Brokers’ news content and AI-generated news summaries are provided by an affiliate, Global Financial Information Services. Providers are gradually being activated.

The Best Informed Investors Choose Interactive Brokers

About Interactive Brokers Group, Inc.: Interactive Brokers Group affiliates provide automated trade execution and custody of securities, commodities, and foreign exchange around the clock on over 150 markets in numerous countries and currencies, from a single unified platform to clients worldwide. We serve individual investors, hedge funds, proprietary trading groups, financial advisors and introducing brokers. Our four decades of focus on technology and automation has enabled us to equip our clients with a uniquely sophisticated platform to manage their investment portfolios. We strive to provide our clients with advantageous execution prices and trading, risk and portfolio management tools, research facilities and investment products, all at low or no cost, positioning them to achieve superior returns on investments. Interactive Brokers has consistently earned recognition as a top broker, garnering multiple awards and accolades from respected industry sources such as Barron’s, Investopedia, Stockbrokers.com, and many others.

EDX Markets deploys Eventus’ Validus platform for trade surveillance on its institutional digital assets marketplace

NEW YORK, Dec. 10, 2024 – Eventus, a leading provider of comprehensive, at-scale trade surveillance and financial risk solutions, and EDX Markets, a leading digital asset technology firm that combines an institution-only trading venue with a central clearinghouse, today announced that EDX has deployed the Eventus Validus platform for trade surveillance on its marketplace.

Backed by a consortium of prominent Wall Street firms, EDX was founded in 2022 to facilitate secure and efficient institutional digital assets trading. EDX Markets went live in 2023, providing clients with access to better liquidity that minimizes risk through its marketplace and central clearinghouse. With EDX on board, nearly 20 digital asset venues across the globe now rely on Eventus for their trade surveillance.

EDX Markets CEO Tony Acuña-Rohter said: “We selected Eventus for this important technology due to the firm’s deep experience in digital assets. The Validus platform is widely accepted by regulators around the globe and was seamless to integrate into our marketplace thanks to its cloud deployment and flexible connectivity capabilities.”

Josh Hoffberg, EDX Head of Market Operations, said: “It’s extremely important that we get trade surveillance right. Eventus onboarded our engineers and integrated their trade surveillance capabilities onto our marketplace well ahead of the launch of our New Matching Engine. The Validus platform also provides us with a strong solution that is easy to use and has intuitive market visualization tools that provide us with a comprehensive view of overall activity. We look forward to leveraging the automation tools and extended surveillance capabilities Validus offers as we continue to scale and grow.”

Eventus CEO Travis Schwab said: “EDX has created an experience for institutional investors that mirrors what they have in traditional finance. Minimizing risk is a key part of that experience, and we’re pleased to equip EDX’s marketplace with our surveillance tools, further reinforcing the integrity of the platform.”

About Eventus

Eventus provides state-of-the-art, at-scale trade surveillance software across all lines of defense. Its powerful, award-winning Validus platform is easy to deploy, customize and operate across equities, options, futures, foreign exchange (FX), fixed income and digital asset markets. Validus is proven in the most complex, high-volume, and real time environments of Eventus’ rapidly growing client base, including tier-1 banks, broker-dealers, futures commission merchants (FCMs), proprietary trading groups, market centers, buy-side institutions, energy and commodity trading firms, and regulators. Clients rely on the platform, coupled with the firm’s responsive support and product development, to overcome their most pressing trade surveillance regulatory challenges. For more, visit www.eventus.com.

About EDX

EDX is a digital asset technology firm that combines an institution-only trading venue with a central clearinghouse. EDX Markets, our flagship marketplace, is designed to emulate the world’s most sophisticated exchanges, with deep liquidity, firm prices and low trading costs. Non-custodial and non-conflicted, EDX has structured its business to minimize risk for its members while providing a diverse array of operational and capital efficiencies. Backed by some of the world’s leading trading and venture capital firms, EDX is actively developing new features and expanding its geographic presence to deliver trusted, liquid and efficient crypto trading experiences for all institutions. To learn more, visit edxmarkets.com.

Disclaimer: EDX Markets products are available only to institutions in the U.S. and certain other jurisdictions. This communication is directed solely at investment professionals with experience in matters relating to investments. Any investment activity to which it relates, including services or products described, is available only to such persons. Persons who do not have such professional experience may not rely on it.

By James Hiester, Ervinas Janavicius and Bhavik Domadia, Capco

Tokenization uses blockchain technology to create digital representations of traditional financial instruments and real-world assets. By operating against a distributed ledger with embedded smart contracts, these products allow transparent, nearly instantaneous, and highly automated execution of complex transactions across organizations. This offers many benefits over legacy approaches for both investors and issuers promising to create more secure, faster, and accessible markets.

Tokenization has been steadily progressing towards widespread adoption in financial markets. After many proof-of-concepts and incremental innovations, major financial institutions are bringing real platforms and products to market, suggesting that tokenization may be close to achieving a significant milestone in terms of maturity.

Benefits of tokenization

Unlike crypto, where most advocates focus on benefits such privacy and resistance to censorship, tokenization offers a better set of rails that enhances the existing financial system through operational efficiency and other benefits:

Fractionalization: By enabling investors to purchase a portion of the asset, capital requirements are no longer such a significant barrier to entry.

Real-time settlement: Blockchain transactions can be completed in seconds while including automatic compliance checks, asset transfers, and other events.

Transparency: Tokens are tracked on an immutable ledger providing verifiable proof of ownership as well as an auditable history.

Eliminate intermediaries: Smart Contracts allow transactions to be executed automatically and transfer funds when conditions are met.

Accessibility: As many of the associated operations are automated, digital assets can be traded 24/7 across a variety of exchanges.

Bundling: Tokens allow different assets to be bundled together in baskets, creating greater diversification and new product opportunities.

Automation: Activities that have typically been cumbersome and labor intensive – such as distributing dividends and other lifecycle events – can be automated using Smart Contracts.

Where is the shift happening?

The financial Services industry has centered around a core set of tokenization use cases that stand to benefit most with greater economic viability.

Alternative assets continue to be a primary target for tokenization. With the ability to fractionalize assets like artwork and real estate, tokenization promises to lower barriers to entry and significantly increase liquidity for asset classes that have historically been highly illiquid. For example, a leading permissionless blockchain group recently announced a deal to tokenize over $500 million worth of real estate in Dubai.1 Even for certain assets that have been liquid, such as gold, tokenization can improve efficiency by providing transparent proof of ownership and real time settlement while abstracting away the complexity of physically holding the asset. Tokenized gold has reached a market cap of over $1 billion according to a leading tokenization data company.2

Established financial players appear most focused on products such as money market funds that can maximize the benefits of tokenization while avoiding areas that might be more challenging from a regulatory perspective. A leading global wealth manager recently announced the creation of a money market fund strengthening the trend of large financial institutions offering similar products. Tokenized money market funds make it possible to operationalize the asset as collateral for derivative trading and repo markets.3 Additionally, they allow investors to receive the yield of the underlying assets, a feature stablecoins lack. The leading global tokenization data company estimated the value of tokenized treasuries to be almost $2.4 billion prior to the global wealth manager announcement.

Given the option for 24/7 trading, it only makes sense that the bond and equity markets would be seen as a natural next step in terms of tokenization. However, most institutions are moving cautiously and focusing on security products for institutional investors. Additionally, integrating DLT into existing equity markets would involve massive integration efforts and displacement of deeply entrenched systems.

Roadblocks for adoption

Regulatory compliance – the biggest challenge for tokenized assets is a fragmented, and in some cases antiquated, regulatory structure. From a global perspective, regulation of digital assets has been caught in a patchwork of regional regulation such as the E.U.’s Markets in Crypto Assets (MiCA) regulation, the EU DLT pilot regime (see our insights on this topic in the ‘Related Content’ section at the end of this article), the US Securities Act and Regulation D. Ambiguity around certain aspects of tokenization including staking can add elevated risk for firms looking to introduce novel products.

Legacy infrastructure – especially impacts large, incumbent industry players. Firms continue to depend on legacy systems that lack the capability for real-time processing. The integration of new technologies with these outdated systems presents significant complexity and cost challenges.

Defining maturity of tokenization

Below, we evaluate the maturity of tokenization based on its adoption across different products as well as integration with core systems and processes. If tokenization truly delivers on its promises of operational cost efficiency and automation, we expect it to be a core part of banks’ product offering, technology stack, and operating model.

Maturity Indicator

Achieved Maturity?

Custody Options Widespread availability of reliable digital asset custody options, including financial institutions offering custody of their tokenized assets with their bank of choice.

Not yet – Financial institutions and fintechs have partnered with custody and wallet vendors such as Anchorage, Fireblocks, and Coinbase to support in-house offerings but few offer options for digital asset custody directly to their customers.

Risk & Regulatory Harmony Token protocols align with compliance rules. Regulations have addressed new challenges and issues raised by digital assets.

Not yet – While regulations like MiCA and friendly regulations in some jurisdictions exist, the uncertainty around staking and other SEC action shows there are still gaps and significant questions around the US and global approaches.

On-Chain Insights Analysis of blockchain data allows enforcement action for financial crime measures.

Yes – Vendors like Chainalysis are routinely able to identify wallets and track funds. FBI and other government agencies use existing laws to seize illicit funds.

Core Systems Integration Blockchain operations are deeply integrated with other core systems in institutions to enable frictionless transaction.

Not yet – Financial institutions have yet to deeply integrate their blockchain products with their core systems. While some are creating roadmaps and strategies, production seems far from reality.

Interoperability Assets are interoperable across blockchains and platforms. Assets issued by an institution can be managed on third party platforms.

Not yet – While progress is being made in terms of bridging common token standards, most product launches are limited to ‘walled garden’ platforms.

What’s Next?

The frequency of major product announcements from major financial players clearly demonstrates that tokenization is making major progress. Yet as explored in this article, we have not seen Day 1 for tokenization in the financial services industry. As tokenized products gain foothold in the wider financial system, we expect the surrounding ecosystem to continue to mature.

While we cannot say for certain when the breakout will occur, the availability of tokenized products is consistently accelerating. Financial services firms should have a clear strategy that aligns business opportunities with the technical capabilities of tokenization to capitalize on these trends. Firms should continue to work with the regulatory community to ensure safe, transparent and accessible products, and modernize their legacy infrastructure to reap benefits and accelerate maturity.

Ervinas Janavicus is passionate about innovation and growth, and helps financial services organizations design and implement growth, technology and cost takeout strategies. As a Managing Principal with a proven track record in the US and UK, he has led teams, launched initiatives and new products/offerings, supported COO/CIO client teams, and explored opportunities across geographies, markets and sectors.

Bhavik Domadia is a Principal Consultant at Capco based out of New York City, and he has over 13 years of extensive experience in consulting for executive clients across the Capital Markets, and Wealth and Asset Management domains.

Bhavik’s diversified consulting experience encompasses Enterprise Payments, Investment Banking, Digital Transformation and Blockchain Engineering driven by his ability to conceptualize and identify alternatives, selecting efficient technical and business solutions, improving business processes as well as managing and delivering complex applications.

He also holds Master of Science in Information Systems (MSIS) from Pace University, NY, and is also a certified Product Owner/Product Manager.

James Hiester is a Principal Consultant with Capco who possesses nine years of experience. He possesses extensive in blockchain and as a web developer, building web and cloud-based solutions. James has worked with large financial institutions and energy companies to deliver high performance applications that combine blockchain and cloud technology. James also plays a key role in the digital assets practice at Capco, spearheading the development of prototypes focused on different use cases including tokenization, digital identity, and ESG.

OneChronos, an operator of smart markets that matches trading counterparties using mathematical optimization, has applied for regulatory approval to launch equities trading venues in the European Union and the UK, but also has plans to expand into fixed income and foreign exchange.

In the US, the OneChronos alternative trading system (ATS) runs periodic auctions that seek optimal matches across all orders, instead of matching orders one-by-one based on speed. Each auction looks for the configuration of “winning” orders and per-security clearing prices that will result in the most price improvement dollars cleared, taking into account all the orders’ constraints.

Richard Suth, OneChronos

Richard Suth, co-founder at OneChronos, told Markets Media that the firm has submitted a regulatory application for the UK, and is about to submit for a multilateral trading facility (MTF) in the European Union, which it is aiming to launch in the middle of next year.

Suth said: ”In Europe we are going to compete directly in the periodic auction space, which is about 4-6% of the overall market. We are not just looking to take market share from the incumbents but looking to grow the overall periodic auction space.”

He argued that OneChronos is fixing some of the market structure problems that exist in Europe to allow more order flow to come into periodic auctions, which will result in better execution, less information leakage and less adverse selection. As a result, OneChronos’ design should help promote liquidity throughout the trading day in Europe, instead of everyone waiting for the closing auction.

Since launching in 2022 the OneChronos ATS has become the fastest-growing off-exchange US equities trading venue, according to the firm, and facilitated more than $500bn in institutional securities transactions. In November this year the ATS facilitated an average of more than $4.5bn in daily trading volume according to OneChronos, across roughly 5,000 different stocks per day that are diverse across large, mid and small caps and even sub-dollar stocks.

Suth said the OneChronos ATS now executes roughly 600 block trades a day, which is up from 100 at the end of last year. Volumes are up six to seven times from the end of last year and that growth trend is continuing , he added.

“We are really proud that our performance has not deteriorated even though volume has grown significantly, and that is a very good highlight for our broker partners and the buy side,” said Suth.

He continued that OneChronos ATS is participating in a broader range of algo strategies so fill rates continue to climb, which attracts more flow.

“Our sell-side and buy-side clients have said that when firms trade with us, the market stays relatively flat,” Suth added. “That shows that information is not leaking, so they can put in larger trades at more aggressive prices, which promotes liquidity.”

He continued that almost every major bank and broker is connected to the venue, and after accumulating data and measuring performance, they make OneChronos ATS part of the default routing.

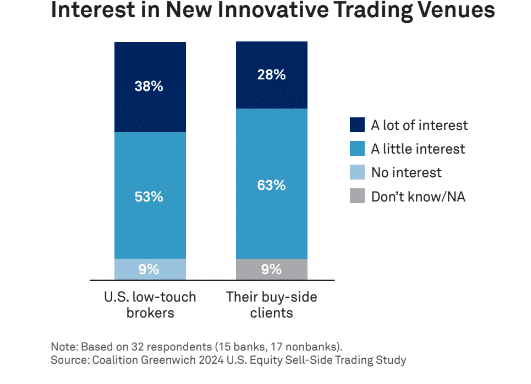

Consultancy Coalition Greenwich identified the OneChronos ATS as one of the innovative ATSs in US equities, alongside IntelligentCross and PureStream in a report, The Innovators: How and Why Alternative Trading Systems Succeed.

Jesse Forster, Coalition Greenwich

Jesse Forster, who leads equity market structure research for the market structure and technology team at Coalition Greenwich, said in the report: “It’s not just a fleeting infatuation—they have won over the hearts of market-savvy buy- and sell-side firms that want to minimize market impact costs.”

The OneChronos ATS runs 10 to 15 randomized auctions a second and Suth said the goal is to level the playing field for all participants, whether they are fast or slow, sophisticated or not sophisticated.

“Execution quality is not a function of speed but of price and quantity as many different order types and strategies can come into the marketplace at the same time to match up in a benign way,” Suth added.

As a result, ATSs execute about 16% of U.S. equity volume according to the Coalition Greenwich study. Nearly half, 40%, of the study participants also expressed a lot of interest in having more innovative trading venues to choose from, as do their buy-side clients, due to the focus on execution quality.

Forster said the trading ecosystem is more open to non-traditional solutions than ever before.

“Whether buy or sell side, it’s crucial for traders to stay on top of the innovative and diverse solutions venues that emerge,” Forster added. “Those that do will capitalize on opportunities that others cannot see.”

The sell-side and buy-side have encouraged OneChronos to expand into equities in Asia, according to Such. After covering equities globally, Suth said the firm will have a footprint to look at other asset classes and products.

Source: Coalition Greenwich

Fixed income

In November this year OneChronos said in a statement that it had raised $32m, led by venture capital firm Addition. Suth said the firm decided to take this extra cash so it has a pretty big war chest for some aggressive expansion goals, both within and outside capital markets.

Andrew Miskiewicz, Addition

Andrew Miskiewicz, partner at Addition, said in a statement that OneChronos has shown remarkable growth in traditional capital markets, and with this additional funding, the company will be able to expand into new markets where significant value can be generated.

“We tremendously value the partnership with Addition, who are great to work with,” added Suth. “They are long-term investors, which aligns with how we are looking to build this business for the next 15 to 20 years.”

Expansion plans include moving into other asset classes, including fixed income in the US, once the firm has regulatory approval.

“We think there are multiple entry points and that we can bring a real step change to improve how some fixed income is traded and give more control over transaction costs,” said Suth.

He claimed that US equities is probably the hardest asset class to get into because it operates at speed and scale, so OneChronos can do something even more powerful in fixed income by running its optimizations and offering tools for expressive bidding.

A lot of automation in fixed income has been in pre- trade and post-trade through automating the messaging between the buy side firm and trading desks, rather than coming up with smart matching mechanisms according to Suth. As a result, fixed income markets are 10 to 15 years behind in terms of electronification so OneChronos can provide a “ton of value.”

”The entrance of expressive bidding into fixed income will be a huge game changer,” added Suth. “It has been proven to work in other industries around the world, is much more efficient than traditional auctions and operates at a fraction of the cost.”

OneChronos aims to expand trading opportunities in fixed income for all participants through improved efficiency, and providing better control risk and the transaction costs going into a trade.

“They currently don’t know these things until the trade is done and that is the real game changer,” said Suth.

Foreign exchange

FX currently has either a continuous limit order book or bilateral streams. However, Suth said the market is increasingly becoming more algorithmic so it fits very well into OneChronos’ strategy.

“We think spot FX is going to launch at the end of the first quarter of next year,” said Suth. “We would like to get into FX derivatives as the next product launch within that space.”

As the year closes, Lynn Strongin Dodds looks at important dates on the 2025 financial regulatory calendar. Ironically many are not new but the latest update of existing legislation.Read on for our financial regulatory roundup for 2025.

EMIR 3.0

Clearing has been a bone of contention for years but Brexit in 2016 opened the door for the European Union (EU) to finally design rules to shift traders’ allegiance from London to the bloc. From the end of this year, they will have a six-month period to implement the latest iteration of the European Market Infrastructure Regulation (EMIR) – 3.0.

The cornerstone is the so-called active accounts which cover all categories of derivatives subject to clearing, identified by the European Securities and Markets Authority (ESMA) as being systemically important. Currently, these are euro denominated OTC interest rate (IRD), Polish zloty and short-term interest rate derivatives (STIR).

An active account is defined by three operational criteria, the first dubbed “permanently functional” which means that it should have the necessary IT connectivity, internal processes, and legal documentation. Second, it has to be sufficiently resilient to allow clearing of large volumes of derivative contracts at all times and finally, the infrastructure should accommodate new business at any time.

There is also the representativeness requirement which is tied to the size of a firm. It requires organisations to mirror to some extent the portfolio they have in the UK on the continent. For example, those that exceed €100bn of outstanding notional clearing volume will need to clear at least five trades at a maximum of fifteen subcategories per month which is equivalent to 900 trades per year.

There are some exemptions. For example, it will not apply to counterparties with a notional clearing volume outstanding of less than €6bn in respective derivative contracts or to client clearing services. It will also be scaled down to one trade for European pension schemes because many only make a limited number of concentrated long-term IRD trades. In addition, counterparties which already clear at least 85% of their trades in systemically important derivative contracts at an EU central counterparty (CCP) will be immune.

ESMA will be in charge of monitoring implementation efforts via a newly established Joint Monitoring Mechanism (JMM) which will also evaluate the effect on the overall exposure to Tier 2 CCPs as well as the fees charged by CCPs in general for setting up the account and for clearing.

The regulator will also look at other developments in clearing which can affect EU CCPs such as cross-border client clearing relationships, concentration risks due to integration of EU financial markets, and cross-border risks.

The new regime is in response to a December 2023 consultation under the Wholesale Markets Review (WMR), which found that the existing transparency framework in these markets lacked significant impact on price formation and imposed high operational costs. The revised rules will replace the Financial Instruments Transparency System (FITRS) with a simpler, timelier post-trade transparency regime.

Currently transparency requirements apply only to bonds admitted to trading on a venue and to derivatives subject to a clearing obligation. The new rules eliminate public trade reporting requirements for OTC trading of non-specified instruments conducted by investment firms. Trading venues will need to meet updated standards for transparency, while recognised investment exchanges will have to follow high standards similar to those used for exchange-traded derivatives such as futures.

This translates into reducing instances where transactions that do not contribute to price formation are reported to the public as well as improving the content of post-trade reports and the correct identification of derivatives. Liquidity determinations will also no longer rely on prior calculations but instead, a set of proxies will be employed to categorise an instrument as liquid.

Other changes include revising the definition systematic internalisers (SI) from a quantitative to a qualitative approach, though the regulator does not expect this shift to affect which firms are designated as SIs. At the moment the FCA is consulting on the future of the SI regime for bonds and derivatives, with feedback invited until 10 January 2025. It aims to introduce more substantive changes to SI obligations alongside the new definition, with both changes expected to take effect at the end of next year.

DORA

Given the amount of air time devoted to the EU’s Digital Operational Resilience Act (DORA), market participants should be well prepared. It kickstarts 2025 on 17 January with aim of creating a more coherent and comprehensive framework from an often disjointed, patchwork set of rules scattered across different sectors and EU countries.

The regulations is looking to bolster the IT defences of the region’s financial service firms in the event of a serious disruption such as a cyber-attack, The main focus will be on five key areas – ICT risk management, ICT related incidents, digital operational resilience testing, third party risk and information sharing.

DORA is also part of a wider global legislative agenda that pension funds need to be cognisant of even if they are not directly impacted by it. This includes the Critical Entities Resilience Act (CER), Network and Information Systems Security 2 Directive (NISD2) and Data Governance Act. Last year also saw an agreement reached on the Cyber Resilience Act, the first set of global cybersecurity rules for digital and connected products that are designed, developed, produced and made available on the EU market.

As a recent white paper by Broadridge in consultation with consultancy Firebrand notes, DORA is widely regarded as the most comprehensive and stringent regulation for operational resilience globally, requiring detailed self-assessment and planning. The rules also have extraterritorial reach which means information technology and communications (ICT) third party service providers within as well as outside the European Union will be in scope.

The paper notes not complying can result in a fine as the national competent authorities can impose sanctions of up to 2% of a firm’s total annual worldwide turnover. Moreover, ICT third-party service providers that are designated as “critical” by the European Supervisory Authorities (ESAs) may face penalties of up to €5m.

There are though unresolved issues regarding the DORA requirements for subcontracting ICT services. The FIA shared its position recently calling for “proportionate and risk-based approach to supply chain risk management that should be based on materiality and not subcontractor rank.” The trade body asserts that such an approach would ensure firms “are able to focus and continue to monitor material risk across the entire supply chain.” In the recently published regulatory technical standards, ESAs asserted “remaining RTS on Subcontracting will be published in due course.”

The most recent reiteration of the EU anti money laundering (AML) legislation represents a significant and structural change in the region’s approach since the first directive was issued in 1991. Effective 1 July 2025, the new AML package reshapes the regulatory, institutional and supervisory framework.

The reforms establish a single AML rulebook as well as an AML Authority (AMLA) that will provide supervisory oversight over high-risk financial entities, harmonising standards for AML in the region. The Authority will also foster improved cooperation and information-sharing. This should lead to not only improved risk assessment but also protection against emerging financial crime risks such as those relating to cryptocurrencies and digital assets.

In terms of preparations, market participants need to update risk assessment methodologies, to ensure their procedures align with the new regulations and that all aspects of the single rulebook are incorporated. In addition, more stringent customer verification and monitoring systems will need to be implemented particularly for high-risk clients and to meet the new enhanced due diligence requirements.

Firms should also establish protocols for accessing and reporting to centralised bank account registers as well as conduct comprehensive training programmes to help employees get up to speed with the new AML world order.

Basel endgame?

In a speech delivered to the Brookings Institution on 10 September 2024, Federal Reserve Board vice-chair for Supervision Michael Barr indicated he planned to dilute the capital impact of Basel III Endgame and Global Systemically-important Bank (G-SIB) which was set to become effective July 2025.

Under the planned proposals, GSIBs would have 9% higher common equity Tier 1 capital requirements in the aggregate, and other large banks would face an estimated 3% to 4% increase in capital requirements, This was far less onerous than the original Basel endgame which have had a 19% increase for the largest firms and 6% for the next group. This received strong pushback from banks, industry groups and members of Congress on both sides of the aisle.

For cleared derivatives, Barr will recommend that the Financial Stability Board adjusts capital treatment by lowering the level of capital that clearing banks are required to hold against the client-facing leg of a client-cleared derivatives transaction. “This change would better reflect the risks of these transactions, which are highly collateralised and subject to netting and daily margin requirements,” he adds. “This also would avoid disincentives to client clearing…”

However, given change is afoot in the US with the impending Trump administration in 2025, the jury is out as to whether these watered-down proposals would get the requisite seal of approval from the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC). There is a view in some investment banking quarters that the restrictions will be further eased or scrapped altogether.

CME Group, the world’s leading derivatives marketplace, announced that as of November 29, more than 3 billion Micro E-mini Equity Index futures traded across all four indices.

“With over three billion of these contracts traded in less than five years, our Micro E-mini Equity Index futures continue to establish themselves among the most actively traded and deeply liquid index products,” said Tim McCourt, Global Head of Equities, FX and Alternative Products at CME Group. “As investors continue to navigate ongoing market uncertainty, index choice is as important as ever. Our breadth of products across every major U.S. index allow clients of all sizes to more nimbly scale index exposure up or down.”

“Nasdaq and CME Group have been providing investors with access to the Nasdaq-100 Index® through innovative products for more than 25 years, including the Micro E-mini Nasdaq-100 Index, which offer investors greater flexibility as they manage their portfolios,” said Emily Spurling, Senior Vice President and Head of Global Index at Nasdaq. “We extend our congratulations to CME Group on achieving this milestone and look forward to our continued collaboration to deliver products that give investors more exposure to our Nasdaq-100 Index® ecosystem, which has included the most groundbreaking and innovative companies in the modern economy for nearly 40 years.”

“S&P Dow Jones Indices congratulates CME Group for reaching another significant market milestone,” said Tim Brennan, Global Head of Capital Markets at S&P Dow Jones Indices. “This latest milestone reinforces the ongoing strength of both the S&P 500 Index, widely regarded as the best single gauge of the U.S. equity market, and the Dow Jones Industrial Average, one of the world’s most watched and widely cited benchmarks.”

“FTSE Russell congratulates CME Group on reaching this significant milestone of three billion contracts traded across its Micro E-mini derivatives complex,” said Shawn Creighton, Director of Index Derivatives Solutions for FTSE Russell. “As our valued, long-term partner, we are proud to have supported CME Group in such an achievement and look forward to continuing our collaborative work on growing the Russell 2000 product suite. Since its introduction in 1984, the Russell 2000 Index has been widely viewed as the leading benchmark for small cap performance, serving as the basis of investable products. The Micro E-Mini Russell 2000 futures provide investors access to a highly liquid and efficient U.S. small cap equity risk management tool.”

Micro E-mini Equity Index futures became available for trading on the S&P 500, Nasdaq-100®, Russell 2000 and Dow Jones Industrial Average in May of 2019, becoming one of the most successful new product launches in CME Group’s nearly 180-year history. In addition, Micro E-mini S&P MidCap 400 and Micro E-mini SmallCap 600 futures joined the Micro E-mini futures suite in March 2023.

Due to ongoing client demand, and the strong support of index partners, brokers and the intermediary community, these contracts have continued to grow. Additional highlights include:

2.5 million contracts in average daily volume in 2024-to-date

19% of volume outside of U.S. trading hours

More than 700 firms and 620,000 unique accounts have traded these contracts in the last year

TECH TUESDAY is a weekly content series covering all aspects of capital markets technology. TECH TUESDAY is produced in collaboration with Nasdaq.

Emerging technologies such as artificial intelligence and cloud are driving compliance and operational strategies for capital markets firms – and it’s equally important for firms to invest in people, i.e. the data scientists and related specialists who make it all work.

Those were key highlights of the Nasdaq 2024 Global Compliance Survey, which collated responses from 94 compliance professionals within capital markets.

Now in its ninth year, the annual survey provides insights on the ever-evolving surveillance and compliance landscape, through the eyes of surveillance and compliance professionals – high-level decision-makers as well as those directly managing processes. The aim is to provide valuable insights while also serving as a guide for navigating change in this critical business area.

This year’s survey was conducted between May and July 2024 and covered a broad cross-section of the industry globally, prominently including sell-side firms (28%), corporate-retail banks (17.2%), and market infrastructure providers (16.1%).

The survey showed that protecting a company’s brand and managing reputational risk continues to be the most important function of compliance, with 32.8% of respondents saying so. “The consistent emphasis on managing reputational risk underlines just how critical reputation is to an organization’s overall success,” the report stated. Second was complying with regulatory reporting requirements – a new field in the ninth annual compliance survey – which garnered 23.9%.

Broadly speaking, change agents in compliance departments are twofold: increased regulatory scrutiny that is forcing firms to improve processes, and technological advances such as AI that are enabling firms to clear the higher regulatory bar. The survey indicated firms are increasingly adopting a forward-looking approach that helps them stay ahead of regulatory demands while managing an ever-expanding array of data sources.

Capital markets firms are continuing to deploy “healthy” investment into compliance operations, with surveillance technology, communications monitoring, and additional compliance staff cited as key areas. Regarding hiring, the survey showed priorities are shifting from bolstering operational support and administrative processes, more toward data science and technology expertise.

“Firms are increasingly investing in the underlying data infrastructure that is essential for managing, integrating and analyzing data efficiently and effectively,” the report stated. “And there is now more emphasis on advanced technology capabilities, including the use of sophisticated tools and systems for real-time monitoring and predictive analytics.”

Going forward, one-third of survey respondents said understanding and implementing technology capabilities was their biggest compliance-related concern for the coming year. Granularly, firms are looking to technology to reduce false positives, better handle huge data volumes, and improve cross-product monitoring capabilities.

“The evolving compliance landscape underscores the critical role of technology in modern financial firms. As regulations become more intricate and data-centric, the ability to understand, implement, and leverage technological advancements is paramount for effective compliance,” the survey concluded. “By prioritizing technological integration and innovation, financial firms can better position themselves to tackle the dynamic compliance landscape, ensuring resilience and compliance in an increasingly complex regulatory environment.”

Click here to access the full Nasdaq 2024 Global Compliance Survey.

Creating tomorrow’s markets today. Find out more about Nasdaq’s offerings to drive your business forward here.