Over the past 12 months, participants in the wholesale foreign exchange (FX) market have welcomed the launch of the FX Global Code, and its set of six over-arching principles that promote the integrity and effective functioning of the market. What makes the Code unique is that it encourages FX market participants to publicly acknowledge their adoption of the Code. Indeed, since it was released in May 2017, over 100 institutions have joined Pragma and committed publicly to it.

Alongside banks, brokers and technology vendors, a number of buy-side and non-financial institutions have signaled their commitment. Adoption amongst the latter group, which includes corporates and treasury departments, is significant for a number of reasons.

Firstly, non-financial institutions are active and sizable market participants, trading approximately USD127 trillion a year[1].

Secondly, when the Bank for International Settlements (BIS) established the Foreign Exchange Working Group to begin writing the Code in July of 2015, the Code was primarily directed at those firms providing trading services to asset owners, like corporations. A corporate treasurer that commits to the Code sends a public message to its service providers – banks, brokers and vendors – of the behavior it expects from them – creating a positive ripple effect across the market. This opens and encourages new ways of doing business, and, in particular, advocates for greater use of algorithmic trading and TCA.

Trading electronically in FX has been commonplace for years through Request-For-Quote (RFQ) or click trading. However, the increasing fragmentation of liquidity, accelerating speed of ECN matching engines and market participants, coupled with the proliferation of new trading tools, has created a whole host of fresh challenges and opportunities for corporate treasury departments.

One of the Codes six principles is Execution, which provides a set of principles clarifying what traders should expect from their service providers. It also outlines the processes and policies they should have internally around trading in order to promote fair and orderly markets.

Algorithms set the benchmark for best execution

Corporates signing up to the Code will rightly expect their banks and brokers to demonstrate compliance with these principles as well as to continue to provide trading tools, like algorithms, that support adherence to the Code. While early execution algorithms were limited to automating relatively straight-forward trading instructions and traded on one venue, the technology and logic underpinning algorithms has advanced significantly over the past decade as the FX market has evolved.

Today the speed of trading, coupled with the number of venues and increasing variety of order types, make it impossible for a human trader to replicate algorithmic behaviour on one order, let alone if the trader has multiple orders to trade simultaneously.

A high performing execution algorithm will assess the current market situation, the available sources of liquidity at a given point in time and execution strategies available. After analysing this information, it will select the optimal routing decision and execute a trade in the most efficient manner while minimising market risk – all without the involvement of a human.

In a recent study by Greenwich Associates, 58% of traders (including corporates) found that algorithms materially reduced overall trading costs.[2] Additionally, Greenwich found that over a quarter of FX traders believed algorithms enabled them to have more time to spend on complex orders.

Thus, in addition to improving execution quality on an order by order basis, algorithms have the indirect potential to improve performance on more complex orders by allowing corporate treasurers to spend more time on them.

Utilising transaction cost analysis to measure execution quality

The Code is also leading to greater demand from corporates to measure and evaluate execution quality. One way of achieving this is through the use of transaction cost analysis (TCA) tools.

Algorithmic trading lends itself well to TCA because the entire order chain, from the first order sliced to the market to the last order slice, is logged in databases and can be easily extracted in order to analyse the orders performance vs. the quotes in the market.

Historical trading data can also be reviewed against a number of metrics and factors, such as price benchmark, trade duration, venue traded, currency pair and trade size. This enables corporates to measure and understand if they are achieving high-quality execution on trades and where they can improve their trading processes.

Thus, algorithmic trading results can be easily measured and analysed in order to better understand ways to improve. This feedback loop can be more difficult and challenging to obtain using trading methods outside of algorithmic trading.

A trading technique to suit institutions of all sizes

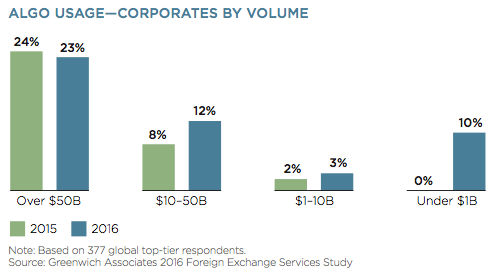

As the market becomes increasingly electronic, algorithmic trading continues to increase in popularity. Currently, it represents only 10% of dealer-to-client FX volume, but one in four of the largest institutions use algorithms where it can represent 25-30% of their volume.[3] These statistics cover both asset managers and corporates, but its clear that algorithms are a tool of growing importance.

It is noteworthy that the strongest increase in algorithmic trading comes from smaller institutions trading less than USD1 billion a year, according to Greenwich Associates.[4] This meaningful increase in both penetration and the proportion of algorithmic trading flow executed by corporates demonstrates that algorithmic trading tools are not just for the biggest, most sophisticated investors.

The evolution of FX trading that has led to the use of execution algorithms will continue to gain momentum. The execution quality and the degree of transparency available to traders through algorithmic trading are in line with the spirit and letter of the FX Global Code, and provide a useful framework for corporate treasurers to demonstrate best practices.

Curtis Pfeiffer is Chief Business Officer at Pragma Securities

[1] Bank of International Settlements Triennial Central Bank Survey of foreign exchange and OTC derivatives markets in 2016

[2] Greenwich Associates, The Evolution of FX Algos: From Nice to Have to Need to Have Q1 2018

[3] Greenwich Associates, The Evolution of FX Algos: From Nice to Have to Need to Have Q1 2018

[4] Greenwich Associates, Long-Term Investors embrace FX Algos Q2 2017

Curtis Pfeiffer is Chief Business Officer at Pragma Securities

{kind=link}