In this post Ill investigate the key drivers of the unrelenting cryptocurrency/cryptoasset markets, and explain why they arent likely to go away soon. In particular, I will focus on the incentives which cause rankings sites to uncritically include junk exchange volume in their data.

The major stakeholders in this market are exchanges (naturally), altcoin/cryptocurrency/fork issuers, and coin ranking sites, who mutualistically work together to extract value from one group: retail investors. Unwitting investors juice the whole operation with infusions of capital. While none of this is particularly groundbreaking, I felt that it was worth exposing these relationships so investors might understand the nature of the game that theyre playing.

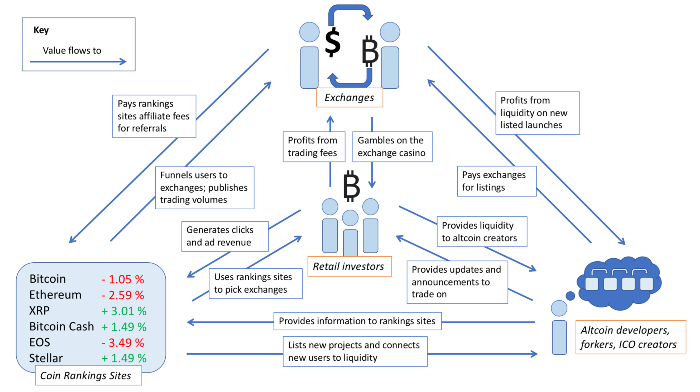

The below graphic summarizes the essence of the relationships between the four groups.

This might be a bit difficult to parse, so Ill explain each group in turn.

Exchanges

You have two broad sorts of exchanges in this industry: the fiat onramps, and the altcoin casinos (Ill leave aside p2p exchanges or DEXes for now). The fiat onramps tend to be regulated, comply with KYC/AML, may even surveil trading, and generally behave like full-reserve banks. Coinbase and Gemini are the archetypes. This piece isnotabout those exchanges?-?they generally play by the rules and are in the midst of a pivot towards regulator friendliness.

The other exchanges, the ones Im writing about here, are the altcoin casinos. They tend to be un- or lightly regulated, domiciled in exotic places like the BVI or the Seychelles or Malta, and may hop around from jurisdiction to jurisdiction to avoid the watchful eyes of regulators. Binance is the archetype. They tend to have a devil-may-care attitude to compliance, KYC/AML, wash trading, and reporting. They may not even deal in fiat at all?-?traders typically have to use BTC and ETH to get access to the rest of the casino.

Actually using these exchanges is quite difficult in many cases. The great unmentionable in the industry is that no one interested in a utility token and the resources it might provision habitually uses these exchanges. These are not individuals that these exchanges target as end users. Getting BTC at a fiat onramp, getting registered at a crypto-to-crypto exchange, sending the BTC, navigating the orderbook, making the trade, and juggling private keys and wallets; this is impenetrable to most neophytes. Instead, end users at these exchanges are day traders and gamblers who want access to the global, 24/7 altcoin casino. Some whales naturally trawl the markets but the majority of participants are retail investors looking for a 100x. Nothing new here.

Altcoin developers and teammembers

Exchanges have a mutualistic relationship with altcoin developers and marketers (issuers). Generally speaking, creating an altcoin is not technically challenging. Many, many altcoins over the years were created withforkgenor any of the numerous ERC20 generators (123). The main challenge for the folks on the altcoin team is not technical, but rather social. This is euphemistically calledcommunity building. This of course refers to broadening the set of buyers for the token or coin, and getting existing buyers to become more fanatical in the support of their chosen coin.

Community building is another word for marketing. This happens through many channels and is the subject for another, more expansive post. However from the developers perspective, it is a delicate game of creating just enough innovation (or more realistically, the illusion of innovation) so that investors believe that the project is progressing at a reasonable pace towards its stated goals. Developers are encouraged to hype up partnerships, new releases, new objectives, and a drip feed of news and announcements. Each unanticipated piece of information is a positive shock which encourages investors to keep buying and justifies their prior purchase.

The most exciting events for investors are new exchange listings. Since exchanges are fragmented pools of liquidity, and everyone wants to trade new launches, the sudden listing of an asset on an active exchange may in fact cause rapid price appreciation. It is an open secret that altcoin developers and marketers pay (read: bribe) exchanges to list their project. Many projects have pooled budgets drawn from a premine which are earmarked for listings fees. Binance made its business model out of shaking down developer teams for listings. But how does the exchange make the case for itself as the recipient of a fat listing fee? Simple: by posturing as a liquid and active trading venue.

After all, issuers are generally the largest holders of their coins, and they also benefit from a listing pump. Often, a large listing on an exchange like Binance will be an opportunity for the team of insiders to divest their holdings and reach a successful exit. So it is in the interest of altcoin developers/promoters to pony up and pay a large fee (these can cost issuers hundreds of thousands of dollars, usually paid in BTC), and its in the interest of exchanges, especially second-tier exchanges, to project an image of deep liquidity.

Coin RankingsSites

This is where the rankings sites come in. They occupy a fted position in the industry. Ostensibly, they perform a useful service to investors and receive little in return aside from ad revenue. But the under-reported reality is more sinister. Rankings sites are squarely at the center of the extractive game that siphons money from retail investors and deposits it into the pockets of altcoin creators and exchange operators.

What is the business model of the coin rankings sites? Sites like CoinMarketCap, CoinGecko, CoinRanking, Cryptoslate, CryptoCoinRankings, CoinCodex, CryptoCoinCharts, (et al.) sell ads, and in some cases, insert affiliate links to the exchanges. Some of them will sell blended pricing APIs to more sophisticated traders who want a reliable price feed. Many if not most exchanges have affiliate schemes, and referral links (reflinks) can be a lucrative source of revenue if you are the intermediary between active traders and exchanges.

Sometimes rankings sites win doubly by accepting payment for banner ads for exchanges or trading venues, and then including their own affiliate links in the ad itself. Its good money if you can get it. Investors go to these sites to find links to exchanges where they can trade their coins of choice, especially if they are smaller projects and do not have many points of liquidity. Since the rankings sites are the ports of call for investors, they have an almost captive audience and can easily monetize with an affiliate link. CryptoCoinCharts and CoinCodex have direct affiliate links to exchanges from their sites. Some aggregators will allow you to trade cryptocurrency directly from the rankings site itself.

This doesnt just stop with exchanges. Anyone who visited CoinMarketCap from April-November 2017 will recall their everpresent BitConnect banner. BitConnect was an infamous ponzi scheme with heavy affiliate elements?-?it survived based on new users from reflinks, and in turn paid affiliate partners handsomely. Not content to stop at BitConnect, CoinMarketCap ended up hosting banner ads for a multitude of other scams. Luckily myself and the BCC Ponzi account documented this and held them to task.

CMC also made a killing from banner ads with reflinks to Bitpetite, a BitConnect clone.

Those are six-figure monthly revenues for directing traffic to a now-defunct ponzi. Yes, this is the same CoinMarketCap that millions of users and dozens of funds trust with their exchange data. The wrinkle goes further. The BitConnect ponzi relied on exchanges like CoinMarketCap uncritically posting exchange data showing massive appreciation in the BCC token. Of course this was illusory, and there was nothing behind the curtain. The vast majority (95%+) of BCC volume derived from a single exchange,which was hosted on bitconnect.co.By uncritically listing this volume with no caveats, CoinMarketCapdirectly enabledthe BitConnect scam, which ended up siphoning around $100m from investors (my estimate).

So not only was CoinMarketCap, the largest and most popular aggregator, guilty of enabling scams by accepting payment for banner ads, in some cases they monetized them withaffiliate links within the banner ads themselves.

Aside from enabling and directly profiting from scams, CoinMarketCap is a largelyamateur operationrun from an apartment in Long Island City, and has proven itself generally unable to make sophisticated judgments about exchange liquidity. If youll forgive my digression, lets get to the broader problem at hand.

The con

So whats the issue here? The chief problem has to do with the interplay between rankings sites, exchanges, and issuers, especially as it relates to exchange volume. It goes like this:

- Issuers want to list on liquid markets and exit or pump their positions

- Exchanges want to advertise themselves as liquid, so issuers will be more amenable to paying listing fees

- The altcoin casino exchanges are mostly unregulated and unmonitored, and can thus get away with virtually anything

- Many exchanges thus engage in wash trading to make their volumes appear greater and improve their perceived liquidity profile

- Rankings sites monetize through reflinks and ads, and lack the resources to monitor each exchange, and hence uncritically publish exchange data

- Wash trading exchanges gain in the rankings on the rankings sites, successfully marketing themselves

- Exchanges profit, rankings sites profit, issuers profit, all at the expense of investors (who may win in the short term)

The negligence of the coin rankings sites is the primary reason Im writing this post. The other aspects are well documented. While fiat-onramps are professionalizing and working to assure regulators of their integrity, markets at the altcoin casinos are widely understood to be deficient. While arbitrary changes to the ranking sites methodology is known to be a risk, especially after theKorea debacle, the sheer amateurish nature of these rankings sites is under-reported. LPs for crypto hedge funds might be horrified to find that many funds were marking their positions against CoinMarketCap data, which aggregates deliberately fudged data from the altcoin casinos. The primary issue is the uncritical presentation of data derived from exchanges which is clearly fictitious?-?Sylvain Ribes hascovered the fake volume plague well. CryptoExchangeRanks used an innovative methodology?-?comparing claimed exchange volume to their relative web traffic?-?tofind particularly egregious offenders.

Investors looking for reliable data at present are left with few options. They can either selectively trust exchanges, aggregating data themselves, or use a more discriminating source like the Blockstream/ICEdatafeed. The market is professionalizing, and hopefully extractive and negligent operations like CoinMarketCap will be a creature of the past.

The future of thismarket

The problem with the [altcoin casino|altcoin issuer|rankings site] troika is how neatly intertwined all their incentives are, and how poorly-educated users are about each. In many cases, exchanges is a misnomer. These things are more akin to the bucket shops of the 20s, the boiler rooms of the 80s, the unregulated poker sites of the early 2000s which ran fractional reserves or granted insiders special access to the hole cards of unwitting players, or the unregulated forex or binary options venues that popped up in the last decade.

Quite simply, most of the crypto-to-crypto exchanges have nothing in common with exchanges like the NYSE or the NASDAQ. While some investors are aware of this, many mistakenly believe them to have integrity, even storing their coins on those exchanges for extended periods. The exchanges, in turn, market themselves with rampant, and indeed obvious, wash trading. But they are difficult to shut down or regulate?-?after all, clearing and settlement occurs on the uncensorable Bitcoin and Ethereum networks.

Thus, while there is still demand for global, 24/7 casinos to gamble on altcoins, these shady exchanges will still exist.And while investors use the amateurish rankings sites for information on trading venues, exchanges will be incentivized to market themselves by posturing as more liquid than they actually are.And if these exchanges continue to list hype projects and give issuers their exit, issuers will continue to be incentivized to play the marketing game and generate spurious roadmaps and dupe investors. Investors should be wary of these entities and make informed decisions before diving in.

Nic Carter is the cofounder ofcoinmetrics.io, a free on-chain data source, and a partner atCastle Island Ventures, a fund which takes seed stage equity stakes in operating businesses building services for, and on top of, public blockchains.