The International Securities Exchange will launch its ISE Gemini options exchange at the end of June, pending Securities and Exchange Commission approval.

“We are ready to go,” Gary Katz, ISE president and chief executive officer, told Traders Magazine during the options industry’s annual conference in Las Vegas. “Everything is in place.”

Gemini is intended to complement ISE’s flagship marketplace—and not compete with it—by appealing to a broader group of liquidity providers.

Because ISE does not pay a rebate, except in certain isolated cases, most quoting there is done by dealers hungry for large slices of incoming orders. ISE typically charges both liquidity suppliers and takers.

By contrast, Gemini will pay liquidity suppliers a rebate, according to Katz. That is expected to make it a more attractive venue on which to post quotes for professional traders and retail brokerages.

Despite the switch to maker-taker pricing, Gemini will not alter its order allocation model. It will keep the traditional pro-rata model that rewards traders who quote in size. It will not adopt time priority.

Pro-rata order allocation involves allotting the largest slice of any incoming order to the trader quoting the greatest size. It typically benefits market makers who possess the requisite skills and capital to quote options frequently and in size.

The model contrasts with the time-priority methodology which allocates orders on a first-come first-served basis. That can benefit non-dealers, but results in smaller quotes. It is also unpopular with some of the larger market makers that are trying to trade against specific orders sent to the exchanges by their customers.

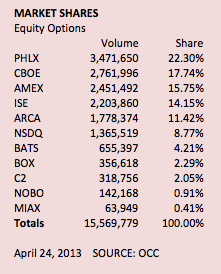

Combining maker-taker pricing with pro-rata allocation is not unusual. The Nasdaq OMX PHLX options exchange pioneered the model a few years ago, paying rebates to dealers in some of the more active names. and has boosted its market share.

Pro-rata order allocation involves allotting the largest slice of any incoming order to the trader quoting the greatest size. The model contrasts with the time-priority methodology which allocates orders on a first-come first-served basis.

With Gemini, Katz still expects most of the liquidity to be provided by dealers, but also sees professional traders, retail and institutional brokerages and their customers posting as well.

“The idea is to attract resting flow,” Katz said. “You will see firms resting proprietary orders. You will see [brokerages’] customer orders resting there.”

ISE chose to stick with a market-maker friendly pro-rata model and not adopt a price-time allocation model because the former leads to larger quotes.

A pro-rata structure forces dealers to compete on size.

“Size is the best advertisement to attract business,” Katz said.

{kind=link}