FLASH FRIDAY is a weekly content series looking at the past, present and future of capital markets trading and technology. FLASH FRIDAY is sponsored by Instinet, a Nomura company.

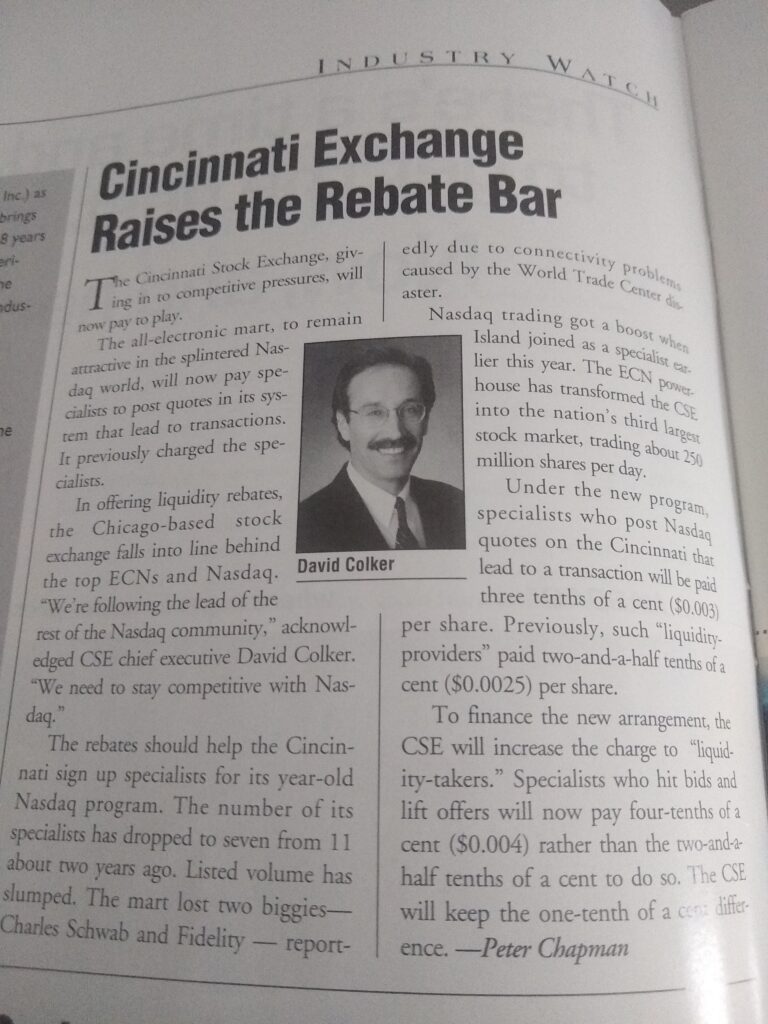

When last sighted in the pages of Traders Magazine, David Colker was Chief Executive of the Cincinnati Stock Exchange, discussing a new plan to offer liquidity rebates in a January 2003 article.

We caught up with David from his home in Evanston, Illinois to learn more about his career and see what’s new in 18 1/2 years.

How did you get involved with the Cincinnati Stock Exchange?

The CSE Chairman at the time (Jim Anderson) was a partner in the Cincinnati law firm with which I was practicing (Taft, Stettinius & Hollister). I had developed a friendship with Jim, and, when I decided that practicing law in a large firm was not for me, Jim invited me to work for CSE, where I started as a staff attorney in January 1984.

What was the exchange’s competitive advantage?

In 1984, CSE was a few years into the process of becoming the country’s first fully computerized stock exchange. The elimination of our physical trading floor and its replacement with a fully electronic model created an enormous cost advantage for CSE because of the elimination of expenses associated with a physical trading floor. This innovation allowed CSE to offer instantaneous, low-cost executions at the national best bid or offer.

What was the 2003 debate on liquidity rebates about?

Debate about liquidity rebates has been around forever, and it continues today with Robinhood receiving liquidity rebates from Citadel Securities. Order flow has value, and so exchanges and broker-dealers compete for it by compensating providers of order flow in some fashion. In 2000, CSE decided to take advantage of its operational cost efficiencies by offering to share its market data revenue – which only exchanges could earn – with customers who brought their order flow to the Exchange. This allowed us by 2003 to capture 35% of all trading in Nasdaq-listed issues. We regulated the activity to ensure that, despite such compensation, the ultimate customer always received the best possible execution price.

What were the highlights from your time at CSE?

I am most proud of two things: (1) completing and continuously improving the transition of CSE to the country’s first fully automated stock exchange, which allowed the public customer to receive, for the first time, an instantaneous low-cost execution at the national best price; and (2) creating the opportunity – through the liquidity rebates mentioned above – for the public customer to receive, for the first time, real-time professional-quality market data.

How did the exchange business change during your 23 years there?

See above. To put this change in context, when I started working for CSE in 1984, the NYSE had a monopoly on the exchange business, processing 85% of all trade activity in its listed issues. Nasdaq had been formed only a few years earlier, and both CQA/CTA and ITS had just begun (there being no consolidated national quote or trade information or intermarket trading vehicle to ensure best execution pricing before this time). In addition, with no automated settlement infrastructure, trade settlement took five days. Only the NYSE specialist had knowledge of limit book orders, and the law mandated a $0.125 minimum bid/ask spread. Executions on the NYSE were extremely slow, poorly priced, opaque, and enormously expensive. And the NYSE often had to completely shut down if there was activity that today would be less than 1% of the volume normally handled. Imagine a world of paper order tickets and physical stock certificates that had to be delivered each night. And think about the catastrophic economic disruption that we would have experienced during the recent pandemic had this world still existed.

Which securities firms were most influential during your CSE days?

The most influential firms at CSE were major Wall Street firms that were looking to become specialists in NYSE-listed issues and to adopt electronic trading. Examples included Paine Webber, Schwab, Fidelity, Pershing, Prudential, and Timberhill.

Why did you leave CSE?

I chose to leave the Exchange in 2007 because I was physically and mentally exhausted. I’m sure you can imagine the toll taken by competing in the exchange world for 23 years.

What have you been doing since 2007?

After taking a couple of years to regain my health and travel with my wife, I tried to create a music venue that integrated in one room a concert hall, recording studio, and video sound stage. I also partnered with an investment banker and securities technology leader to try and create a new real estate index which would have superseded Case-Schiller and provided investors with a new and better trading vehicle for investing in the real estate market. Finally, I partnered with some major Wall Street players to attempt create a more open, fair, and transparent platform for the public investor to participate in IPOs.

Do you keep in touch with many folks?

I still maintain contact with my staff: CFO, Marketing, Public Relations, Systems, and Executive Assistant. Plus Jim Anderson.

What is your take on the exchange business today?

I wish I had something intelligent to say here, but I really have not kept up with all the changes in that world. However, as I said above, I am proud of my contribution, and I am thankful that the exchange business is so wonderfully efficient now that it could continue to underpin our financial system during the pandemic.