Heads of the top 5 hedge funds earned more than $12 billion in fees for a year when they did not do much more than copy the market — their funds were buying stocks like Facebook, Microsoft and Alphabet — the same stocks that took the entire market up. This makes sense: if that is where the money is, they should be in.

Or should they?

Hedge fund’s goal is to earn income no matter where markets go. The most basic strategy of a hedge fund is long/short: buying (going long) stocks that it expects to rise and offsetting the cost by borrowing and selling (going short) stocks that it expects to decline in value. Regardless of whether markets go up or fall, long/short should earn the hedge fund money.

It makes a lot of sense that the first hedge fund — A.W. Jones & Co. — was created by a sociologist and writer. Hedge funds seek to benefit from market inefficiencies and gaps. They bet on human error and take positions that are contrarian to the wider market and the investor sentiment. Who better to do that than a sociologist?

The problem is that betting on the idea that the wider market is wrong can take a lot of time and money. Michael Burry, the hero of The Big Short lost a lot of his investors’ money bettings against the housing market before 2008. This was nearly fatal for his fund, until things turned around and he was proven right. He was lucky. It could have taken longer by which time all of his investors would have taken money out.

No more.

2008 saw some of the largest hedge fund gains in history. Fund managers like Bill Ackman and Steve Eisman caught world-wide attention by making billions in profits betting against the sub-prime crisis.

But the same event that gave rise to these colossal gains changed the world for hedge funds forever. The global meltdown of 2008 launched an era of easy money with tighter regulation and de-humanized financial markets.

De-humanization. Algorithmic trading and digitalization of finance, in general has led to a massive decline of human traders. To a large extent, the big face-offs between investors; the adventures described in the movie The Wall Street or in Michael Lewis’s books are no more. Financial markets are operated by autonomous systems, so there is less scope for human error that the hedge funds thrived on for so long.

Easy money. In an effort to save global financial system, central bankers put markets on narcotics. They pushed into the system more money than ever before. As a result, too much money is chasing too few opportunities. Debt yields are at historic lows. The only place to go for return are equities, and the best equities are U.S. technology large-caps, of course.

This makes sense: they are profitable companies that grow at a rate that vastly outpaces anything else in the market. And there is an element of excitement to them, too, so the story feeds on itself and the prices keep rising. The issue is that it takes too long. Markets have continued in this direction relentlessly for years now. Any contrarian investors will be proven wrong again and again. Hedge funds are either closing doors completely or changing to family offices as they cannot justify their fees with returns that lag the S&P 500.

The next big short.

The issue with the big short is that there is no big short. Unlike 2007, it is hard to put finger on anything that would be systematically wrong; anything that could be the trigger of the next recession. There is also no market bubble that would be comparable to the 2000, and there is certainly nothing as wide-spread as the regulatory failures that gave rise to the Savings & Loans crisis in the 1980s.

Instead, the relentless slow market melt-up is pushing everyone into same trades and increases the divide between the good and the bad stocks.

The size of the gap between U.S. large-caps (S&P 500) and pretty much anything else begs the question: could this be the contrarian bet of the current cycle?

The next big long.

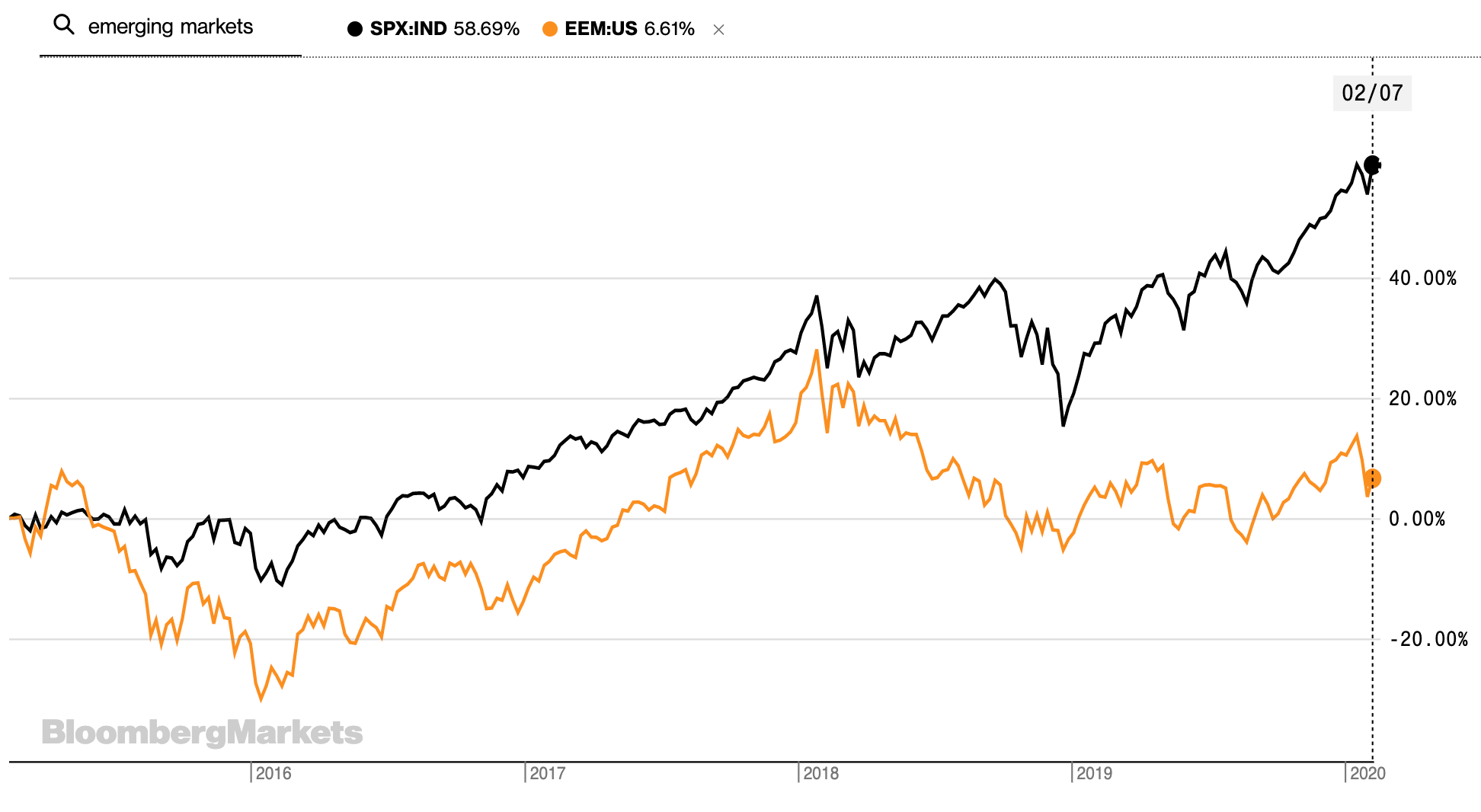

Emerging markets have underperformed U.S. equities for years now. This is strange. If you believe that emerging markets should be the motors of economic growth (rapidly growing middle class, cheap labour) then the markets should reflect that. There are valid reasons for this underperformance. Perhaps somewhat counterintuitively, U.S. trade war is making U.S. dollar stronger and emerging markets weaker as the flight to safety sees capital flowing to U.S. treasuries.

The outperformance of the U.S. large-caps (and the FAANG-complex in particular) even further accelerated in 2019. Large market correction in December 2018 made everyone worried. Once again, central banks came to the rescue and cut rates. The markets saw a massive turnaround, with most money being sent right back to the safest bets — U.S. large-caps, which have left everything else behind, including the smaller U.S. businesses. Throughout 2019, Russell 2000 significantly under-performed S&P 500. The main cause for this could be that the performance of smaller businesses is strongly tied to economic growth, which remains weak even in U.S.

The most gaping divide — the place which equities outperform the most — is in commodities. The outbreak of the coronavirus has made this even more extreme, with both copper and oil — two commodities that go most in tandem with the economy — sent sharply down. There are valid reasons for the weakness in commodities (lower demand due to more efficient global economy, slower global economic growth after 2008 or stronger U.S. dollar pushing naturally all commodity prices lower since they are denominated in the greenback), but the current market prices may have gone beyond them.

Oil is particularly difficult. Many oil hedge funds were forced to close down in recent years, as they were proven repeatedly wrong betting on the reversal in oil prices. Andy Hall — the so called oil trading “God” — shut his Astenbeck Master Commodities Fund II Ltd. in 2017. Northlander Commodity Advisors LP suffered a 50.6% fall last year, and Andurand Commodities Fund suffered annual loss of 7.1% in 2019 even as the oil price surged towards end of the year amid Middle East tensions and other macro factors.

Traders and analysts have been calling for a reversal in the oil super-cycle for years now. Technical analysts like to make the observation that commodities tend to have an inverse relationship to equities. This makes sense: when equities outperform, no one buys commodities, but when things turn for worse, commodities surge.

There are, of course, fundamental reasons for the lower oil prices. The rise of the hydraulic fracking turned U.S. to world’s largest oil producer, and drastically transformed the global oil market. This is not only due to larger oil supply, but more importantly because U.S. shale producers can respond to market price signals much more swiftly than other sources of supply. U.S. is not only the major producer, but is expected to overtake Russia and Saudi Arabia as world’s largest oil exporter in 2024.

The market is trying to process this expectation of larger global oil supply at a time when the EVs are believed to transform the auto industry and Tesla stock gains bitcoin-like price momentum. Yes, there are valid fundamental reasons for the oil weakness, but it is also fair to say that the investor sentiment is negative, and that the market’s pendulum swung away from oil.

Small investor.

The only advantage that we — small investors — have against Wall Street is that we can afford to take a position for the very long-term. Time and again we have seen hedge funds fail in this historically unique market environment. History demands that there be a market reversal at some point.

{kind=link}