George Metrou was only an intern. But he found himself in the right place, at the right time.

The firm he had joined was growing. The portfolio manager, one Michael Corbett, was looking to hire. So, after graduating from DePaul University in 2005, Metrou joined Perritt Capital as an analyst.

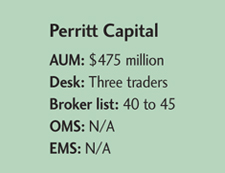

He was the third analyst. And all three-Metrou, Matthew Brackmann and Brian Gillespie-remain in their posts today.

Perritt focuses on companies it finds that are being ignored by almost any other asset manager or research house. Its MicroCap Opportunities Strategy Fund takes stakes in companies with a market worth of no more than $500 million. Its Ultra Microcap Strategy Fund looks for companies with market worth of no more than $150 million.

Metrou and his fellow analysts are largely generalists in the hunt for little-known companies they believe can deliver the “small firm effect”: where investors, over time, get higher returns from small-cap stocks than their higher-cap brethren, statistically speaking.

“We’re playing at the very small end of the small cap,” said Metrou. “What we’re looking for, generally, are underfollowed, under-researched companies, finding things before the Street does.”

Once a potential investment is identified, Metrou or one of the other analysts will meet with management teams. Quality of management is a top priority-and once it’s found, maintaining a relationship with them is paramount. Initial interviews are followed up with additional calls, particularly after earnings results come in. If the teams don’t respond, that becomes “a red flag and something we won’t tolerate too long.”

But most management teams are responsive and provide their direct lines for follow-up conversations.

Then there’s the financial analysis. Each firm is put through a nine-factor test, which examines fundamental income statement and balance sheet metrics-gross margin, return on assets, profit and cash flow that exceeds profit, for starters.

With so little trading in these small firms, Metrou does not rely on algorithmic trading at all, because he is interested in block trades-trades of more than 10,000 shares and typically around 25,000 shares.

He networks with 40 or 45 brokers on a regular basis, to overcome the lack of liquidity. And a fair amount of “appointment” trades.

The brokers also act as a source of alpha, because often, Perritt is the only place where a broker can work a big trade for a small company.

Assets of the two firms’ funds sat at $100 million at the start of the century, hit $700 million in 2007 and now are around $475 million.

Block trades account for 35 percent of all Perritt trading. And the firm does not rely on electronic markets that specialize in large blocks, such as the Liquidnet dark pool.

Metrou and his fellow analysts trust their network of 40 to 45 brokers across the country and rely on to send it indications of interest every day in stocks it holds positions in. And then it responds, with “voice negotiations.”

“We can’t just slam something through an algo and think it’s going to, you know, get us best execution,” Metrou said. “So, it’s been kind of a symbiotic relationship with brokers that has resulted, with them providing us more blocks and indications as we’ve gained their trust. We’ve taken advantage of that more and more, and then that reinforces the trust. So the block trading has grown over time.”

Here, according to Metrou, are the building blocks it uses to trade in large blocks, when the company involved itself is small.

1. Publish the portfolio, for all to see.

The firm manages two main funds, with $475 million in assets between them:

Perritt MicroCap Opportunities Strategy Fund (PRCGX), which invests in companies that are listed in the bottom 20 percent of major stock exchanges as ranked by market cap.

Perritt Ultra MicroCap Strategy Fund (PREOX), which invests in companies that are listed in the bottom 10 percent of the major stock exchanges as ranked by market cap.

At any given time, the firm holds roughly 150 “unique positions.” The holdings are disclosed in 13F filings with the Securities and Exchange Commission, every quarter. Only a handful of other names draw interest, which can be communicated directly to the broker network.

The firm expects that any broker that plans on doing repeat business with it will familiarize itself with those positions, because those are the stocks in which it will entertain propositions to buy or sell large blocks.

2. Adhere to the 100:1 rule.

Perritt asks its network of brokers to send indications of interest every day, consistently.

But it doesn’t send out indications of interest, itself, very often. The ratio of incoming IOIs to outgoing is about 100 to 1.

“We have worked to make the ratio of inbound indications and outbound indications on natural liquidity highly in our favor,” Metrou said. “We want for opportunities to arise and be presented to us to respond to.”

Each morning, its investment team reviews a half dozen to a dozen indications of interest that come in from its network.

And responds only when it makes sense. Perhaps once or twice a week.

3. Leverage the human factor.

Because it gathers indications of indication through its own group of trusted brokers, you could say Perritt runs its own dark pool.

It gathers information about market interest on its own. But does not disclose its own intent.

Until it calls back and negotiates a deal, person to person.

“So much of our order flow is handled with voice-negotiated block trading,” Metrou said. “That personal relationship is very virtual. Building that trust, getting to know someone quite well.”

4. Make it clear to brokers that consistency matters.

The top 10 brokers in Perritt’s network get 75 percent of its business. “Those are the guys who get it,” Metrou said. “They understand how I am trying to go about this.”

The more often you send IOIs to Perritt, the greater the chances of a cross. Pure and simple, said Metrou.

“The more often you indicate to me,” he said, “your odds of getting a cross go up.”

5. Identify ghosts.

Trust, sure.

But if you get an indication of interest, watch like an eagle to see if the fill actually happens.

“If I respond and say I am willing to sell that security,” he said, “the frequency of falling down on a trade is very low.”

It’s one of the oldest rules in the book. But if the indication isn’t real, then trust is misplaced.

A broker that sends a false indication gets put on probation. And if it happens again, it is dropped from the network.

(c) 2013 Traders Magazine and SourceMedia, Inc. All Rights Reserved.

http://www.tradersmagazine.com http://www.sourcemedia.com/

{kind=link}