On October 19, 1987, the Dow Jones Industrial Average index (“DJIA”) fell 508 points or 22.6%. The next year, the financial industry adopted a market wide circuit breaker (“MWCB”) system designed to “help promote stability in the equity and equity-related markets by providing for increased information flows and enhanced opportunity to assess information during times of extreme market movements.”[1]

The MWCB triggered for the first time on October 27, 1997 (the only time before 2020), when the DJIA fell 554 points or 7.2%, breaching both MWCB levels in place then. That time, there was consensus that the triggering “was needless at best, and inappropriately halted trading.”[2] The threshold levels were widened, with the first threshold level set at a 10% DJIA decline.

On May 6, 2010, the DJIA fell 9.2% during the “Flash Crash” incident, and the MWCB did not trigger (correctly, given the new 10% threshold). The consensus was that it would have been better if it had. The threshold levels were narrowed back, and the DJIA was replaced by the S&P 500 index (“SPX”). By that time, the SPX had become a better broad market index and a better basis for coordinating halts across cash and futures markets.

This March, amid market volatility caused by the coronavirus pandemic, the MWCB level 1 (7% threshold) triggered four times, as follows:

Did the 2020 market wide circuit breakers appropriately or inappropriately halt trading? Will the MWCB system be changed once more?

In this two-part series of blog posts, I gather some preliminary data to shed some light on these questions. I focus mostly on the first 3/9 MWCB event. In today’s entry, I discuss the triggering of a MWCB halt and price discovery on primary exchanges during the halt. In next week’s entry, I will discuss price discovery on secondary venues and across venues, as well as the end of a MWCB halt.

More work will be needed to understand the full impact of the MWCB halts on the volatile markets of March 2020. I do not aim to reach definitive conclusions about potential flaws or fixes here. However, some first take-aways will emerge. Here is a preview of the take-aways for both parts of the series:

- The MWCB functioned well. Halting and resuming trading was orderly. Trading venues and the Securities Information Processor (SIPs) operated very smoothly. A meaningful subset of traders appeared to have automated logic able to navigate MWCB scenarios. This level of readiness is remarkable for an event that had not happened in more than twenty years.

- SPX lags price discovery before and around the open. Real-time SPX is based on last sale trades. Some stocks do not have any last sale trade until many minutes after 09:30. This is particularly true for NYSE-listed stocks because the NYSE manual opening process can imply opening delays. For example, on 3/9, CMG (Chipotle Mexican Grill) had its first last sale trade at 09:31:24 on ARCA. YUM’s (Yum! Brands) first last sale trade was its NYSE open at 09:51:33. As a result, it took a few minutes for the official SPX index to reflect its “basket fair value” and trigger a MWCB halt at 09:34:13.

- There are nontrivial differences in MWCB rules across exchanges. For example, some exchanges close the books for the whole duration of the halt, while others keep orders live and accept order cancellations.

- There is a limited amount of price discovery on secondary trading venues. Price discovery during a MWCB halt happens mostly on the primary exchange. More work is needed to determine whether the contribution of secondary venues to market wide price discovery is helpful, neutral or harmful.

- Entering and exiting MWCB halts are fragmented events that leave room for latency races. Halting and resuming trading requires coordination across geographically dispersed venues. Information must travel from point A to point B. Fast private information networks provide an advantage. MWCB halts are no exceptions to this common rule of trading.

- Only proprietary exchange market data feeds provide real-time information during a MWCB halt. SIP data provides almost no real-time updates during a MWCB halt, whereas most proprietary feeds maintain their usual level of detail. The gap between SIP and proprietary feed data is another common rule of trading. It is exacerbated during a MWCB halt because there is no NBBO and no trades.

- Traders are in the best position to say whether a 15-minute halt is useful. Long halts are designed for humans — computers do not need 15 minutes to run an auction. Market data may reflect manual interventions that may not have been possible without a MWCB halt. Ultimately, this is a question best answered by traders.

1) Entering a MWCB halt

There are currently 3 MWCB levels. When the SPX declines 7% from its previous day closing level before 15:25, markets are halted for 15 minutes. When the SPX declines 13% before 15:25, markets are again halted for 15 minutes. Finally, when the SPX declines 20%, markets are closed for the rest of the day. A given MWCB level can trigger only once per day. Only MWCB level 1 events were triggered in March.

The MWCB trigger is based on the official SPX value, which is computed and disseminated every second between 09:30 and 16:20 by S&P Dow Jones Indices. The SIPs receive the SPX data and tell exchanges when a level is breached. When a listing exchange receives the breach message from the SIPs, it immediately halts trading in its listed stocks and sends halt messages back to the SIPs (1 message per stock). The SIPs disseminate those halt messages back to everyone else and secondary trading venues halt trading. This dance is a bit wasteful (why would secondary trading venues not halt trading when the level is breached?) but largely harmless.[3] It does mean that some exchanges are still matching trades when the primary is halted. For example, ARCA (ARCX) matched a 100-share trade in EBAY more than 60ms after Nasdaq (XNGS), the primary, halted trading:[4]

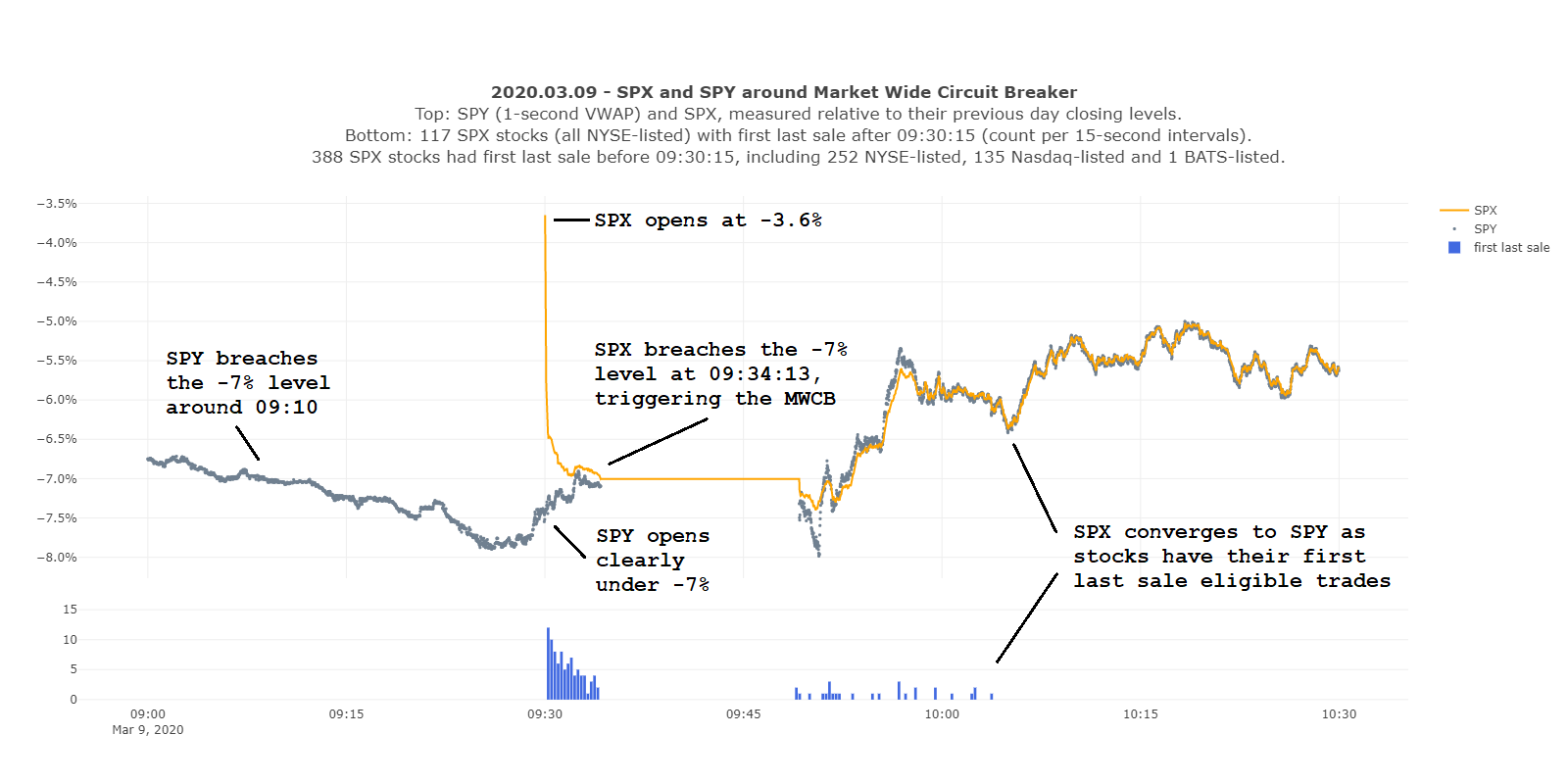

The official real-time SPX level plays a key role in the triggering of MWCB halts. But SPX does not reflect the day’s price of a constituent stock until the first last sale eligible print.[5] (Before then, SPX uses the stock’s previous day closing price, which is likely to be very stale in a MWCB scenario). Pre-open and odd-lots trades are not last sale eligible. There can be robust price formation in SPX stocks and SPX-tracking ETFs (such as SPY) for a significant amount of time before SPX reflects its “basket fair value”. Indeed, it took 4 minutes 13 seconds for the MWCB to trigger on 3/9, while the SPX “basket fair value” would have triggered a MWCB immediately at 09:30:01.

NYSE’s opening mechanics play a central role in these delays. Opening auctions are typically last sale eligible. Nasdaq’s opening auction is fully electronic. On 3/9, all Nasdaq-listed SPX stocks had had a last sale eligible open before 09:30:02. NYSE’s opening auction has a manual component. NYSE-listed stocks can take minutes or more to open. As a side-effect, it can take minutes or more before their first last-sale eligible trade. For example, CMG (Chipotle Mexican Grill) had its first last sale trade at 09:31:24 on ARCA (all markets can generate last-sale eligible trades starting at 09:30). YUM’s (Yum! Brands) first last sale trade was its NYSE open at the 09:51:33 post-halt reopening auction. This is one of the main take-aways of this blog series. Below is a chart that illustrates this phenomenon:

The top part of the chart plots SPY trades (VWAP for each 1-second intervals, grey) and SPX levels (orange) measured relative to their respective previous day closing values. SPY breached the -7% level around 09:10 in pre-open trading. It opened clearly under -7%. SPX opened at -3.6% at 09:30:01, and declined quickly to -5.6% at 09:30:03. By then all 135 Nasdaq-listed and 1 BATS-listed SPX stocks had a last sale eligible trade, but only 200 out of 369 NYSE-listed did.

The bottom part of the chart counts the number of SPX stocks that had their first last sale eligible trade after 09:30:15 (all NYSE-listed), by 15-second intervals. SPX slowly converged to the SPY value in the first minutes of trading, and finally breached the MWCB threshold at 09:34:13, which triggered the MWCB halt. After the 15-minute halt, 28 NYSE-listed SPX stocks still had not had their first last sale eligible trade. SPX was not immediately in line with SPY. The last NYSE-listed SPX stock had its first last sale eligible trade at 10:03:44 (UDR, United Dominion Realty Trust). SPX and SPY ended up back in line.

2) Price discovery during a MWCB Halt: on the primary venue

During a MWCB halt, exchanges do not match orders. The primary exchange for a stock maintains its continuous order book, accepting orders and disseminating real-time information via standard market data updates in exchange proprietary data feeds. In parallel, the primary exchange also builds an auction order book and provides some limited level of real-time transparency on that book via imbalance and other auction messages.

At the end of the halt, the primary brings together the continuous and auction order books to run the reopening auction. This is very similar to standard opening or closing auctions. However, a major difference comes from the fact that orders are not matched during the pre-auction period (the halt). This means that arbitrage between the continuous and auction order books cannot happen the way it does in the minutes before standard opening or closing auctions.

What kind of price discovery happens during a MWCB halt? Let’s take a look.

Price discovery primarily happens on the listing exchange during a MWCB halt. Listing venues maintain their continuous-trading order book throughout the MWCB halt almost as if there was no halt. Add, cancel and replace orders are accepted. Order book updates are disseminated in real-time through exchange proprietary feeds. A very important difference, of course, is that there is no matching of orders. Another difference is that there are no SIP updates. Traders have to consume proprietary feeds if they don’t want to be flying blind. Finally, listing exchanges also build an auction book during the halt, in order to organize the reopening auction. Auction books are dark, but partial information is disseminated via the proprietary feeds.

Here is the count of new continuous-book displayed orders received during the 3/9 halt by Nasdaq (XNGS) and ARCA (ARCX), counted by second (log scale):

A couple of things are apparent in this chart. First, there is some meaningful amount of activity, with traders adding new orders to the order books throughout the halt. Second, differences between MWCB exchange rules are reflected in the data. The 09:44:13 peak on Nasdaq corresponds to the first Nasdaq imbalance message. By contrast, ARCA starts disseminating imbalance messages right away and there is no particular peak of activity.

Because the primary exchange accepts new orders but does not match orders, its order book can, and frequently does, become crossed. The price discovery picture can be fuzzy in crossed order books. As an example, below is the shape of the QQQ Nasdaq order book just before the reopening auction around 09:49:13. The best bid is $205, the best offer is $187, and there are around 25,000 shares to buy and 25,000 shares to sell crossed on each side of $193:

The original design of MWCB halts was to “provid[e] market participants with time to restablish an equilibrium between buying and selling interest” and to help “to ensure that all market participants have a reasonable opportunity to become aware of and to respond to significant market price movements”.[6] Trading has become automated to a very large extent since the MCWB system was created or since the last time it triggered. Do algorithms benefit from a 15-minute halt, and/or do 15 minutes allow for meaningful manual intervention?

It is hard to answer this question with the data I have access to. Some actions do bear the signature of a potential human-driven intervention. For example, there are times when many orders are suddenly canceled together, with nothing else happening in the market that I can see. Ultimately, the usefulness of a 15-minute halt and extent to which it allows some level of human judgement and intervention are questions best answered by traders.

In next week’s second and final entry of the series, I will describe price discovery on secondary venues and across venues, discuss the end of a MWCB halt, and reiterate a few main take-aways.

[1] Release №34–26198; File No. SR-NYSE-88–23; 53 FR 41637; https://tile.loc.gov/storage-services/service/ll/fedreg/fr053/fr053205/fr053205.pdf

[2] Release №34–39846; File No. SR-NYS-98–06; 63 FR 18477; https://www.govinfo.gov/content/pkg/FR-1998-04-15/pdf/98-10027.pdf

[3] Some exchanges may already be halting trading based on the initial level breach SIP message — timestamps suggest that the 4 CBOE exchanges do.

[4] Comparing and interpreting timestamps across different clocks can be tricky, in general and particularly in the middle of an extreme market event like the MWCB of 3/9 which can cause many kinds of unusual delays. Still, differences of the order of 10ms or more remain usually meaningful. This caveat applies to all timestamps in this blog post.

[5] S&P Dow Jones Indices: Equity Indices Policies & Practices, p.45, available at https://us.spindices.com/documents/methodologies/methodology-sp-equity-indices-policies-practices.pdf

[6] Release №34–26198, see footnote 1

The views represented in this commentary are those of its author and do not reflect the opinion of Traders Magazine, Markets Media Group or its staff. Traders Magazine welcomes reader feedback on this column and on all issues relevant to the institutional trading community.