Buy-side Equity trading desks are experimenting with a strategy that would have been unthinkable just a few short years ago: outsourcing some trades.

Once considered a tool for start-up funds, Outsourced trading (OT) is now being adopted by established Buy-side trading desks as a means of supplementing internal capabilities.

Jesse Forster

Trading desks have spent the last decade learning how to do more with less. Traders are being asked to navigate more venues, more regulation, more data, and more technology—often with fewer bodies and thinner margins. That constant pressure has created a willingness to experiment with new types of providers and to veer from traditional approaches.

“The same logic that once drove the adoption of algos and Electronic trading is now being applied to Outsourced trading,” said Jesse Forster, Senior Analyst in Market Structure & Technology at Crisil Coalition Greenwich and author of Outsourced Trading in Equities: The third channel. “OT providers are being layered in to add capacity, coverage, and infrastructure while keeping strategic control firmly in house.”

Filling Gaps, Not Replacing Traders

Today, at least 15% of Buy-side traders say they augment their desks with Outsourced trading providers.

“Outsourced trading providers are brought in to address overflow and coverage gaps, not to redefine the role of the Buy-side trader,” said Jesse Forster.

Instead of expanding headcount or investing in new technology, firms using OT can convert parts of the trading function into a service cost. This model aligns with the Buy-side’s preference for variable operating expenses, particularly when performance fees are under pressure. Traders are selecting OT providers based on the quality of operational support, responsiveness, and the relationship management providers deliver.

“Outsourced trading is quickly becoming a strategic pillar for established Buy-side desks seeking resilience, flexibility, and operational excellence,” said Forster.

Outsourced Trading in Equities: The third channel draws on the results of a recent Crisil Coalition Greenwich study in which the firm interviewed U.S. Equity traders about their daily workflow, broker selection and evaluation, technology platforms, commissions, technology budgets, and business practices.

The report traces the evolution of OT on Buy-side desks, analyzes current usage and trading volumes, examines the criteria desks use in selecting OT providers, discusses the primary hesitations desks have about the approach, and explains how OT fits into trading desk operating models.

Recent findings from Liquidnet’s latest report suggest that broader regulatory developments, including possible changes to Consolidated Audit Trail (CAT) governance and evolving corporate reporting requirements, could have significant implications for market participants. Traders Magazine spoke with Jeff O’Connor, US Head of Market Structure and Sell-Side ATS Strategy at Liquidnet, about the growing calls for CAT reform, the potential impact on broker-dealers and investors, and what these developments could mean for the future evolution of U.S. market structure.

What are the key concerns driving calls for potential reforms to the Consolidated Audit Trail governance structure?

Jeff O’Connor

In theory, Rule 613 addresses a real problem, the need for a robust, centralized system to track and analyze market activity across what is an extremely fragmented U.S. marketplace. However, in practice, the original bureaucratic structure in which to implement the rule has led to much governance friction, cost overruns, delayed deliveries, and implementation challenges. Across the many SRO’s that make up the operating committee, there is often failure to reach consensus on areas or themes such as specifications, scope, funding allocation, etc. And in the current structure, attempts at improvement need to be effected through amendments to the CAT NMS plan, which is a lengthy administrative exercise in itself.

In April, the SEC issued a concept release to solicit public comment on a comprehensive review of the CAT. The concept explicitly states feedback on whether CAT should exist in it’s current governance structure (highly fragmented) or if the SEC should take full ownership. Which begs the important question, does the SEC have the ability to undertake a structural overhaul with this complexity and magnitude?

The deadline for comments on the concept release is June 22, 2026. There is a strong lobby for SEC ownership. While it will be difficult to course change so drastically, and also keep the SRO access, the current NMS Plan has failed to deliver on the original plan – ie an efficient, cost-effective, accountable audit trail.

How could changes to CAT governance affect market transparency, regulatory oversight, and data security?

While it was perhaps altruistic to have the trading community own and drive the tool designed to audit that same community’s business, the shared ownership between the Exchanges and FINRA has resulted in a model of conflicting interests, lack of common consensus and general mismanagement. Yet it’s the SEC who’s the ultimate arbiter of the NMS, and hence one the biggest (if not the biggest) stakeholders for the purposes of surveillance, guidance and overseeing the market’s integrity. The wedge between the primary stakeholder and the actual owners has resulted in an imperfect system, where perhaps neither party is content. Direct ownership by the SEC would provide the driver of regulatory oversight with the keys to accomplish such task. While the topic of data security is difficult to speculate on, the SEC has made it clear security is a pillar of the current administration. Specifically, Chairman Atkins has reiterated the need to “protect investors” and “ensure the U.S. remain the best and most secure place in the world to invest and do business”.

Do you expect potential CAT reforms to reduce compliance costs for market participants, and if so, where could the biggest savings emerge?

Messaging capacity and data storage are major implication on the broker/dealer side. Resources devoted to full compliance might include developers to code to CAT requirements, legal/compliance officers needed to interpret the guidance, support staff to fix or amend breaks/mismatches, or capacity and storage tech spend. For hardware solutions or utilization of the cloud, both options become very expensive very quickly. Each of these considerations harms innovation and limits strategy spend elsewhere. While some improvements have been made such as the elimination of personally identifiable information (PII), CAT reportable events are averaging 50 billion/day. Only exacerbated by the continued growth in volume both in equities and option markets, and that trend marks a structural shift in liquidity sourcing within the market – ie the volumes aren’t going anywhere. And the more the SEC aggressively interprets what must be reported to achieve CAT goals, the data collection will continue to grow exponentially, and the costs to collect & store this data will follow.

What implications could CAT governance reforms have for trading behavior and overall market structure in U.S. equities?

It’s less a question of CAT’s impact on market structure but more CAT’s impact on the broker dealers trying to comply with market structure. From onboarding new clients to introducing new products or features, broker dealers must consider the ramifications of CAT. Should there be uncertainty or complications around reporting obligations, the result might be lengthened onboards, or more severely, a decision to halt or scale back new initiatives. Onerous regulatory compliance limits innovation. If the SEC was to take ownership, which is a real possibility, Chairman Atkins will attempt to re-snap some obvious inefficiencies while also balancing regulatory oversight, market structure evolution, investor privacy, and cost management. All while still solving for what the original intent of the CAT was – ie the detection of layering or spoofing to manipulate markets.

On June 11 2026 the U.S Securities and Exchange Commission proposed rescinding Rule 611 of Regulation NMS, also known as the trade-through rule, which ensures that investors receive the best possible price regardless of which exchange executes their trade. The rule prevents trading venues from executing an order at a price that was worse than the best publicly displayed price on any other competing exchange.

Paul Atkins, chairman of the SEC said in a statement that although the central aim of Rule 611 was to incentivize displayed liquidity, trading activity has increasingly occurred off-exchange over the last two decades. Atkins said: “I am concerned that what the Rule rather incentivized was a proliferation of new trading venues, which in turn fragmented liquidity and created an increasingly complex, costly, and opaque marketplace for order execution.”

Joe Saluzzi, partner and co-founder of broker Themis Trading, said on X that the SEC has “sold out the retail investor so they could move forward with their tokenized Field of Dreams.”

This is not correct. If these disastrous rules are repealed, FINRA 5310 will become load bearing and the duty to ensure users get best execution will fall to the brokers. It is extremely easy to audit this because exeuction is very easy to measure.

Saluzzi suggested that the SEC the could have proposed modifications including introducing market share thresholds for protected quotes, adjusting SIP revenue formula to stop rewarding exchanges for fleeting quotes and adding depth of book protection. (The SIP, or consolidated tape, publishes the prevailing National Best Bid Offer (NBBO) for U.S equities. The NBBO is a composite of the highest bid and lowest offer across all U.S. equity exchanges in real time.)

Rather than eliminating Rule 611, modifications could have been suggested. I discussed this with @RepStephenLynch at last month's House Financial Services Committee meetinghttps://t.co/AOlyIP1k4Z

@TradingDutchman, who describes himself as an “HFT market maker turned HF market taker”, said:

Part of this “getting ready for tokenised securities “ is abolishing the trade through rule. Crypto exchanges tech is extremely crappy, and liquidity in these TS is even more crap. Part of the CLARITY act is a rule that “if you want to trade TS, you need to be regulated as an… https://t.co/VBSbxUtW06pic.twitter.com/lj0LapgfeL

— The trading Dutchman (@TradingDutchman) June 6, 2026

He said: “Part of the CLARITY act is a rule that “if you want to trade TS, you need to be regulated as an exchange and follow all the existing securities regulations, like reg NMS, reg T, reg SHO, etc

There is no way Coinbase , Binance, etc will be able to do that and compete with Nasdaq / Arca, BATS et all, and they would have to route all that flow away to the incumbents. To prevent that and keep the flow to themselves, it looks like they convinced the regulators to give up the price protection rules for investors.

I am worried there will be a lot of abuse of this exemption. (PFOF anybody?) Let’s wait and find out more detail of what exactly is the plan here.”

Alex Thorn, head of research at digital asset fund manager, agreed the trade-through rule is “one of the biggest structural barriers to tokenized US equities trading in DeFi [decentralized finance] today” as AMMs are not designed to comply with the rule. An (automated market makers (AMM) uses mathematical formulas and smart contracts to set prices and execute trades automatically rather than matching buyers and sellers in a traditional order book.

the Commission voted to propose rescinding Rule 611 (the order protection rule) and Rule 610(e) (locked/crossed market restrictions), plus related definitions. 60-day comment period. proposal, not final.. but the direction is unmistakable

this is one of the biggest structural barriers to tokenized US equities trading in DeFi today. an AMM cannot comply with 611 by construction. it executes against a bonding curve at whatever the pool price is, with slippage, at block-time granularity

610(e) is the same story. AMM prices drift continuously with flow and would routinely lock or cross the displayed NBBO, which venues are currently required to prevent

tokenized NMS stocks still face a host of other questions re: exchange/ATS registration questions, clearance and settlement, and many other rules not designed for defi or peer-to-peer trading. we hope many of these will be addressed in the SEC’s forthcoming “innovation exemption”

two decades of equity market structure built around a single rule, and the SEC wants to lift it, which is an important step in clearing the way for the next step of innovation in trading equity securities

Christopher Perkins, CEO of 250 Digital Asset Management, said:

Been waiting for this… Reg NMS/the NBBO has been one of the biggest challenges and obstacles to unlocking the benefits of tokenized equities. If rescinded, it’s a whole new ballgame. Major unlock for DeFi. Incumbents won’t be happy. https://t.co/zZos7Ka3QY

— Christopher Perkins 🦅🌎⚓️NYC (@perkinscr97) June 12, 2026

Tyler Gellasch, president and chief executive of Healthy Markets Association, said:

Rule 611 just prevents exchanges from executing at bad prices. So this expressly allows brokers, market makers, and exchanges to rip off investors. It is the first major example of repealing tradfi rules to enable currently-allowed crypto market abuses in tradfi. https://t.co/dvZBqWVe6p

Olivia Vande Woude, business development, tokenization at Ava Labs, argued that when an investor buys stock through a U.S. broker, they transact at NBBO or better, because of Reg NMS. She said: “That obligation is why retail investors can trust that the price on their screen is the real one. A token that claims to represent that same share should clear the same bar; anything less is a different instrument sporting the same ticker.”

the tokenized equity debate is missing a word: NBBO. If the token is the share, it should trade at the share's price, @ NBBO or better, accountable to a standard, not a venue's discretion. I wrote up a short piece on why: https://t.co/4QFS3jbImn

Vande Woude added: “The tokenization pitch for equities is access: a user anywhere in the world holding the same assets a U.S. investor holds. That promise is hollow if the price they get is worse, opaque, and accountable to nobody. True access means the same fill, at the same standard, and with the same protection behind it.

So the bar for the category should be simple & public: a tokenized equity should trade at NBBO or better. Ask any issuer whether theirs does, and what percentage of the time it lands inside the spread.”

Trading Technologies and ICE Data Services Reach Agreement for ICE Market Data and Reference Data to Power New TT® Fixed Income EMS

New platform to debut later this year, with preview for market participants at FILS

CHICAGO, June 15, 2026 – Trading Technologies International, Inc. (TT), a global capital markets technology platform services provider, announced today that it has entered into an agreement with ICE Data Services, which is part of Intercontinental Exchange (ICE), to use its foundational evaluated prices and reference data in TT’s new buy-side Fixed Income execution management system (EMS). Additionally, TT will offer ICE’s “Continuously Evaluated Price” (CEP) market data feed to TT clients.

Launching later this year, the new buy-side fixed income EMS will reside natively within the TT multi-asset platform and initially focus on USD Rates and Credit products. This integration allows clients to leverage the same familiar trading widgets and post-trade services they already use for futures, options and FX. Market participants can experience the new platform firsthand this week at the Fixed Income Leaders Summit (FILS) in Boston—a premier three-day conference attracting over 1,000 attendees from 300 companies.

Chris Heffernan, EVP, Managing Director, Fixed Income of TT, said: “The launch of our new buy-side fixed income EMS, powered by premier ICE data, marks a major milestone for the TT platform. By unifying fixed income, futures and FX on a single screen, we are giving clients direct access to the industry’s most sophisticated, award-winning execution tools, and unlocking unprecedented cross-asset trading possibilities.”

Mark Heckert, COO, Data Services, at ICE said: “We are pleased to work with TT to integrate our global, multi-asset class, fixed income reference data, End of Day Evaluated Prices, and CEP into their new buy-side Fixed Income EMS. Our fixed income evaluations and reference data on over 3 million instruments are used throughout the trade lifecycle and may become a valuable resource for users of the new platform.”

Heffernan said: “Navigating the constantly evolving fixed income market requires a platform built for modern complexities. We’ve dedicated extensive time, resources and expertise to engineer the TT platform for this exact environment, reinforcing our commitment to delivering innovative solutions to help define the next-generation, multi-asset EMS for tomorrow’s trading desks.”

About Trading Technologies

Trading Technologies (www.tradingtechnologies.com) is a global capital markets platform services company providing market-leading technology for the end-to-end trading operations of Tier 1 banks, brokerages, money managers, hedge funds, proprietary traders, Commodity Trading Advisors (CTAs), commercial hedgers and risk managers. With its roots in listed derivatives, the Software-as-a-Service (SaaS) company delivers “multi-X” solutions, with “X” representing asset classes, functions, workflows and geographies. This multi-X approach features trade execution services across futures and options, fixed income, foreign exchange (FX) and cryptocurrencies augmented by solutions for data and analytics, including transaction cost analysis (TCA); quantitative trading; compliance and trade surveillance; clearing and post-trade allocation; and infrastructure services. The award-winning TT platform ecosystem also helps exchanges deliver innovative solutions to their market participants, and technology companies to distribute their complementary offerings to Trading Technologies’ clients.

About Intercontinental Exchange

Intercontinental Exchange, Inc. (NYSE: ICE) is a Fortune 500 company that designs, builds, and operates digital networks that connect people to opportunity. We provide financial technology and data services across major asset classes helping our customers access mission-critical workflow tools that increase transparency and efficiency. ICE’s futures, equity, and options exchanges — including the New York Stock Exchange — and clearing houses help people invest, raise capital and manage risk. We offer some of the world’s largest markets to trade and clear energy and environmental products. Our fixed income, data services and execution capabilities provide information, analytics and platforms that help our customers streamline processes and capitalize on opportunities. At ICE Mortgage Technology, we are transforming U.S. housing finance, from initial consumer engagement through loan production, closing, registration and the long-term servicing relationship. Together, ICE transforms, streamlines, and automates industries to connect our customers to opportunity.

Trademarks of ICE and/or its affiliates include Intercontinental Exchange, ICE, ICE block design, NYSE and New York Stock Exchange. Information regarding additional trademarks and intellectual property rights of Intercontinental Exchange, Inc. and/or its affiliates is located here. Key Information Documents for certain products covered by the EU Packaged Retail and Insurance-based Investment Products Regulation can be accessed on the relevant exchange website under the heading “Key Information Documents (KIDS).”

Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995 — Statements in this press release regarding ICE’s business that are not historical facts are “forward-looking statements” that involve risks and uncertainties. For a discussion of additional risks and uncertainties, which could cause actual results to differ from those contained in the forward-looking statements, see ICE’s Securities and Exchange Commission (SEC) filings, including, but not limited to, the risk factors in ICE’s Annual Report on Form 10-K for the year ended December 31, 2025, as filed with the SEC on February 5, 2026.

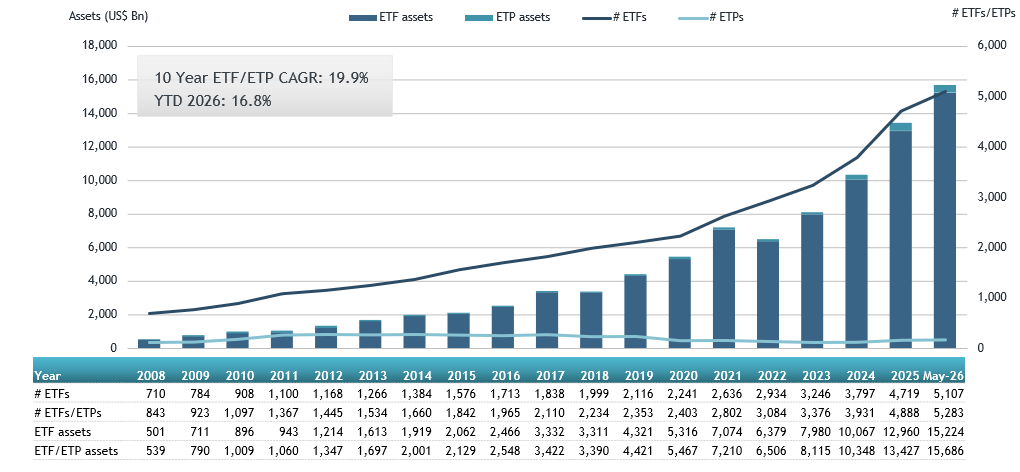

LONDON — June 12, 2026 — ETFGI, reported today that assets invested in the ETFs Industry in the United States reached US$15.7 Trillion milestone, driven by record US$837 billion in YTD net inflows. During May, the ETFs industry in the United States gathered net inflows of US$189.01 billion, bringing year-to-date net inflows to US$837.35 billion, according to ETFGI’s May 2026 US ETFs industry landscape insights report, the monthly report which is part of an annual paid-for research subscription service. ETFGI, is a 14 year old leading independent research and consultancy firm renowned for its expertise in subscription research, consulting services, 6 annual ETFGI Global ETFs Insights Summits, and ETF TV on global ETF industry trends. (All dollar values in USD unless otherwise noted.)

Highlights

Assets invested in the ETFs industry in the US reached a new record of $15.69 trillion at the end of May, surpassing the previous high of $14.87 trillion in April 2026.

Assets have increased 16.8% year-to-date, rising from $13.43 trillion at the end of 2025.

The industry gathered $189.01 billion of net inflows in May.

Year-to-date net inflows of $837.35 billion mark a new record, exceeding $443.32 billion in 2025 and $399.10 billion in 2021.

The ETF industry in the US has now recorded 49 consecutive months of net inflows.

“The S&P 500 rose 5.26% in May and is up 11.27% year‑to‑date in 2026. Developed markets excluding the U.S. gained 5.20% during May and are up 15.33% year‑to‑date, with Korea (+28.71%) and Luxembourg (+20.50%) delivering the strongest returns among developed markets for the month. Emerging markets increased by 3.77% in May and are up 11.44% year‑to‑date, led by Taiwan (+16.95%) and Peru (+11.75%), which recorded the highest gains among emerging markets in May.” According to Deborah Fuhr, Managing Partner and founder of ETFGI.

Growth in assets in the ETFs industry in the United States as of the end of May

Source: ETFGI data sourced from ETF/ETP sponsors, exchanges, regulatory filings, Thomson Reuters/Lipper, Bloomberg, publicly available sources and data generated in-house. Note: “ETFs” are typically open-end index funds that provide daily portfolio transparency, are listed and traded on exchanges like stocks on a secondary basis as well as utilising a unique creation and redemption process for primary transactions. “ETPs” refers to other products that have similarities to ETFs in the way they trade and settle but they do not use a mutual fund structure. The use of other structures including grantor trusts, partnerships, notes and depositary receipts by ETPs can create different tax and regulatory implications for investors when compared to ETFs which are funds.

The ETFs industry in the United States has 5,283 ETFs, assets of $15.69 Tn, from 488 providers on 3 exchanges at the end of May.

The ETFs industry in the US continues to be highly concentrated competitive, with iShares and Vanguard effectively tied for leadership by assets, holding 28.9% and 28.6% market share respectively, while State Street SPDR remains third with 13.2%. Although iShares has the largest number of ETFs at 487, Vanguard has achieved nearly the same asset base with just 115 products, underscoring the strength of Vanguard’s scale and product concentration. State Street SPDR, with 179 products, maintains a significant position.

From a net flows perspective, Vanguard stands out as the strongest gatherer of net new assets, attracting $54.4 billion in May 2026 and $233.8 billion year-to-date, both ahead of iShares at $34.3 billion in May and $155.9 billion YTD. State Street SPDR remains a major player in trading activity, with $59.8 billion in average daily volume, net inflows have been more modest at $10.7 billion in May and $54.3 billion YTD.

Net Inflows

The industry gathered $189.01 billion of net inflows in May.

Year-to-date net inflows of $837.35 billion mark a new record, exceeding $443.32 billion in 2025 and $399.10 billion in 2021.

Equity ETFs attracted $78.62 billion over the month, bringing year-to-date net inflows to $378.22 billion, significantly higher than the $148.51 billion recorded at this point in 2025.

Fixed income ETFs recorded $41.50 billion of net inflows in May, with YTD inflows reaching $151.55 billion, well above the $93.67 billion gathered by the end of May 2025.

Commodity ETFs saw modest net inflows of $147.9 million in May, but remain in net outflow territory year-to-date at $2.99 billion, compared to $14.18 billion of net inflows at the same stage in 2025.

Active ETFs continued to attract strong demand, with $75.95 billion of net inflows in May, bringing YTD inflows to $329.09 billion, significantly exceeding the $177.01 billion recorded over the same period in 2025.

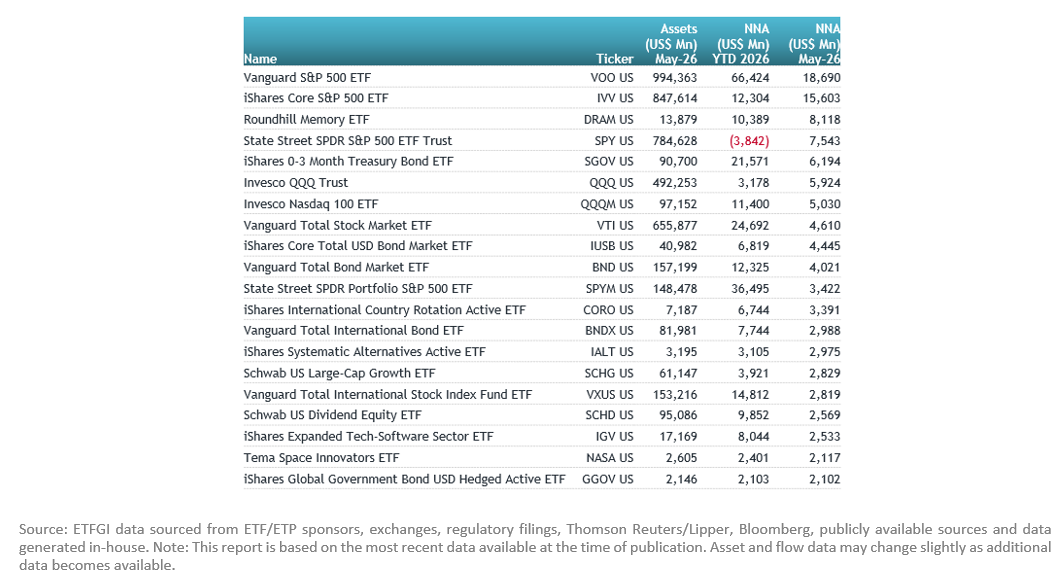

Substantial inflows can be attributed to the top 20 ETF’s by net new assets, which collectively gathered $107.92 Bn in May, the Vanguard S&P 500 ETF (VOO US) gathered $18.69 Bn alone.

Top 20 ETFs by net new assets May 2026

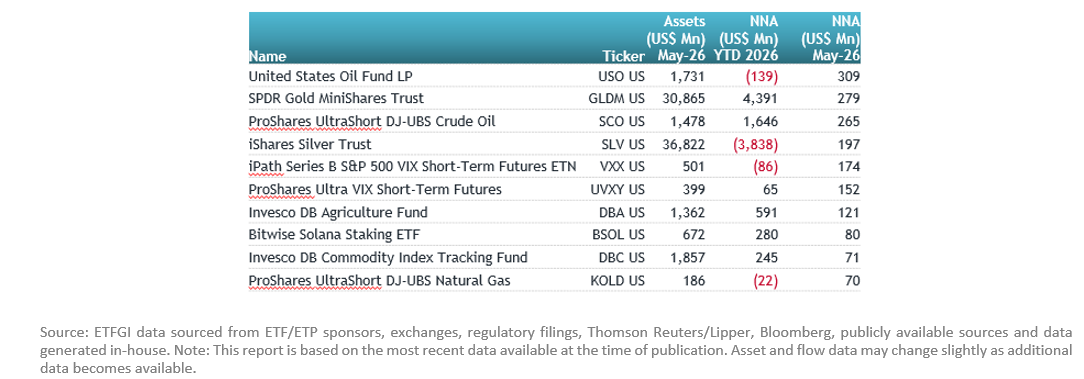

Substantial inflows can be attributed to the top 10 ETP’s by net new assets, which collectively gathered $1.72 Bn in May, the United States Oil Fund LP (USO US) gathered $309.00 Mn alone.

Top 10 ETPs by net new assets May 2026

Investors have tended to invest in Equity ETFs during May.

Contact deborah.fuhr@etfgi.com if you have any questions or comments on the press release or ETFGI events, research or consulting services.

Backpack US has announced the appointment of Dr. Michael S. Piwowar to its Board of Directors. Piwowar brings deep expertise in securities regulation, capital markets policy, and market microstructure. He currently serves as Executive Director of Georgetown University’s Psaros Center for Financial Markets and Policy. Previously, he served as Executive Vice President of Finance at the Milken Institute. He was appointed by President Obama and served as SEC Commissioner from 2013 to 2018, and was later designated Acting Chairman by President Trump.

Ondo has appointed John Hoffman as Managing Director, Head of Product Portfolios, to develop Ondo’s onchain asset portfolios business, according to a press release. Hoffman joins from Grayscale Investments, where he served as Managing Director, Head of Distribution and Partnerships. Before Grayscale, he spent nearly two decades at Invesco, most recently as Head of the Americas, ETFs and Index Strategies.

Mark Militello

Fort Washington Investment Advisors has named Mark Militello vice president and co-portfolio manager of the Small Company Equity strategy, according to a press release. Militello has more than 30 years of industry experience. He will report to Jason Ronovech, CFA, vice president and senior portfolio manager. Militello will be based in the firm’s Albany, NY, office. Militello rejoined Fort Washington after spending four years at Thrivent Asset Management, where he served as senior portfolio manager on the SMID Growth Equity team. In addition, the firm has named Michele E. Hargis as vice president and head of Family Office Services within the firm’s Private Client Group. She will report to Tracey Stofa, managing director and head of Fort Washington’s Private Client Group (PCG).

BlackRock has expanded the responsibilities of Louise Kooy-Henckel, who announced on LinkedIn that she has been appointed Global Head of Sustainable and Transition Solutions. Kooy-Henckel has served as EMEA Head of Sustainable and Transition Solutions since January 2025 and has been with BlackRock since the beginning of that year. Prior to joining BlackRock, Kooy-Henckel spent nearly seven years at Wellington Management as Managing Director and Investment Director for Sustainable and Impact Investments in EMEA.

David Perkins has been promoted to Executive Vice President, Sales & Strategic Growth and will serve as Head of Sales at Genesis, according to a press release. Since joining Genesis, he has played a key role in expanding the firm’s market presence and strengthening relationships across the industry. Shahin Askari has been promoted to Chief Technology Officer. Askari joined Genesis in 2023 and previously served as Chief Platform and Architecture Officer. Michael Henson has been promoted to Chief Delivery Officer and joins the Executive Committee. Henson previously served as Vice President of Forward Deployed Engineering. Jay Taylerson has been promoted to Executive Vice President, Engineering Excellence.

If you have a new job or promotion to report, let me know at alyudvig@marketsmedia.com

Galaxy Digital, the digital assets fund manager, said prediction markets are the future of event-driven markets for institutions as it launched its first over-the-counter (OTC) offering in the space.

The asset manager’s global markets trading desk hosted a webinar on 10 June to discuss the growth in prediction markets and the increasing interest from institutions. Zane Glauber, global head of distribution at Galaxy, said on the webinar that prediction markets are the future of event-driven markets for institutions.

There was more than $44bn of trading across prediction markets in 2025, according to Galaxy research, predominantly on Polymarket and Kalshi. Glauber said: “Prediction markets have gone from niche to mainstream, and the velocity of growth has been quite remarkable.”

As a result the firm launched its first institutional OTC prediction markets offering from its global trading desk with the aim of bringing liquidity, risk management, and institutional scale to event-driven markets. The OTC transactions are between Galaxy and the counterparty, where they each take credit risk, and involve trading economic substitutes for shares on contracts markets that are not fungible with those that could potentially trade on Polymarket or Kalshi.

Galaxy’s offering covers instruments referencing non-sports event contracts traded on Kalshi and Polymarket, including economic, political, geopolitical, and other event-driven markets, with plans to expand to additional platforms.

Zane Glauber, Galaxy

“We think this is a powerful tool to pair with equities, commodities and other hedges for our counterparties,” Glauber added.

Jason Urban, global co-head of digital assets at Galaxy, said in a statement that event-driven markets are becoming core to how sophisticated investors express macro views. Urban said. “We’re giving clients a principal counterparty that can warehouse risk, build hedged strategies across asset classes, and execute at sizes and scale that actually matter to their overall portfolios.”

One example of this strategy is the new desk’s execution of a $10m trade with crypto-native hedge fund Arca, on whether the CLARITY Act for digital asset market structure will be passed by the U.S. administration.

Mike Harvey, head of franchise trading at Galaxy, said on the webinar that the most important reason for institutions to care about prediction markets is for event-driven exposure and hedging. He added: “An age-old problem in macro trading is the construction of the perfect hedge for your view.”

Gil Wassermann, head of prediction markets at Galaxy, commented on the webinar that prediction contracts allow investors to be “hyper-specific” about the exposure they are trying to hedge. He said: “The specificity makes this very different from everything else in financial markets.”

Gil Wassermann, Galaxy

Urban added that prediction contracts allow hedging with “surgical” precision. Galaxy gave a purely hypothetical example of a movie studio launching a major film and wanting to have a floor on their investment by using a prediction market contract to hedge against the film making a certain amount of money on its opening weekend. Wassermann described this type of transaction as a similar risk transfer that is carried out today by a traditional bank’s exotic derivatives desk.

“A client wants to hedge a very specific exposure that is warehoused by the dealer and hedged in vanilla proxies,” Wassermann added. “Clients can trade the outcome and leave all headache of managing risk to us.”

Clients can also hedge against events around macroeconomic outcomes, such as whether a central bank will raise interest rates or whether an asset reaches a certain price. Glauber added that event contracts are surgical tools for corporates to hedge risks to their business, which may not just be FX or interest rates.

Clients have been having conversations with Galaxy about using prediction markets related to macroeconomic and geopolitical events, according to Wassermann. He said: “It has been really interesting to think about how we want to hedge that creatively from our side.”

Hedging is important for Galaxy as it is warehousing binary contracts. Once the outcome is determined, the contract held by the winning party pays out, while the other side loses everything.

Harvey continued that futures are available as alternatives to some event contracts, such as those based on the direction of interest rates. However, he argued that some clients may prefer to use prediction contracts as they receive a defined payout, or they not have access to futures, or they may want a more bespoke hedge.

Wassermann said the new desk had a “reasonably sized” book. He added: “One of things that has been cool is the partnership as a lot of times the conversation starts out with a discussion of the client’s worries. If it is better to just trade this in the vanilla space, we will let them know.”

ETFs

Harvey added that some asset managers have been in discussions about launching prediction market ETFs, but these would need permission from the U.S. Securities and Exchange Commission.

In February this year Roundhill filed with the SEC to register six ETFs investing in event contracts, including which political party wins the presidency and control of either house of Congress. This was followed by similar applications from other issuers, including GraniteShares and Bitwise.

Paul Atkins, chairman of the SEC, said in a statement on 20 May 2026: “Novel products raise novel questions, and I appreciate the willingness fund sponsors have shown in delaying the effectiveness of a number of novel ETFs, including event contract ETFs, while we consider the implications. To ensure we do this in a transparent and thoughtful manner, I have instructed the staff to seek input from the public on how the Commission should respond to recent market changes.”

Jeffrey Ptak, managing director for Morningstar Research Services, said in a blog that the SEC should reject contract market ETFs. He argued that ETFs have been a relatively cheap, reliable gateway to global capital markets, creating trillions in wealth and advancing important goals for investors such as funding college or retirement.

“These proposed products seem like the antithesis of that,” said Ptak. “They’re zero-sum and serve no economically productive purpose, such as facilitating capital formation and spurring innovation. They’re likely to be costly and push investors’ buttons to their detriment.”

Oracle risk

Wassermann highlighted that there are some risks that are very specific to prediction markets, including oracle risk as some of the wording of prediction contracts can be unclear in certain edge cases. He said: “The market is great at pushing to those edge cases and really like testing out this oracle mechanism.”

Jeff Dorman, co-founder and chief investment officer at Arca, said in a blog that the firm is a big believer in prediction markets, as shown by its trade with Galaxy, but that the oracle problem is a huge risk. Dorman wrote in a blog that “Polymarket ruined prediction markets.”

Dorman highlighted a contract on Polymarket that was: “MicroStrategy sells any Bitcoin by May 31, 2026,” for which there was $400m in bets.

In a regulatory filing on 1 June Microstrategy, the bitcoin treasury company, said that the firm did sell bitcoin between 26 May and 31 May, but the contract did not pay out “YES.”

Dorman said “Polymarket posted “additional context” (at 1 p.m. ET Monday 1 June): “no MSTR filing, on-chain data, or credible reporting had confirmed a sale within the market’s timeframe, and confirmation achieved outside that window doesn’t qualify.”

He argued that this does not make sense, as the contract could traded after 31 May and cited a research note from Will Owens at Galaxy Digital who agreed that Strategy sold Bitcoin before that date.

“Everyone who bought YES predicted the future correctly, and the market told them they were wrong,” said Owens. “A prediction market is supposed to price what will happen; when resolution diverges from what actually happened, the product is merely pricing how the platform will read its own rules after the fact. That’s worthless.”

Dorman continued that this will be an interesting case study in “the persistence of negative public opinion that is almost unanimously against Polymarket, the outcome, the oracle, and the UMA protocol’s voting mechanism.”

Washington, D.C., June 11, 2026 – SIFMA today released the following statement from president and CEO Kenneth E. Bentsen, Jr. on the Securities and Exchange Commission’s (SEC) proposed amendments to rescind Rules 611 and 610(e) of Regulation NMS:

“SIFMA appreciates the due diligence the SEC performed ahead of today’s proposed amendments to Regulation NMS, including rescinding Rule 611 on trade-through prohibitions, Rule 610(e) restricting locking and crossing quotations, and related defined terms in Rule 600. We look forward to commenting on the proposal and appreciate Chair Atkins’ intention to ‘simplify market structure and reduce costs for market participants while allowing competition, innovation, and other market forces to shape the continuing evolution of our equity markets’.

“We are encouraged that the proposal includes making conforming changes to other related provisions. SIFMA has long stated that market structure involves many moving, interconnected pieces. Before making any changes, it is important to identify and analyze interconnected market structure elements and study what corresponding impacts could stem from any intentional change, as well as the cumulative net effect of changes. Our markets are the envy of the world. Investors – both retail and institutional – enjoy narrow spreads, low transaction costs, fast execution speeds, high levels of pre and post trade transparency, and strong investor protections. It is important to continue to analyze what changes could mean for all investors. This is particularly true today, as the landscape for modern securities markets is under consideration in conjunction with extending trading into overnight hours and the incorporation of tokenized securities.”

SIFMA is the leading trade association for broker-dealers, investment banks and asset managers operating in the U.S. and global capital markets. On behalf of our industry’s one million employees, we advocate on legislation, regulation and business policy affecting retail and institutional investors, equity and fixed income markets and related products and services. We serve as an industry coordinating body to promote fair and orderly markets, informed regulatory compliance, and efficient market operations and resiliency. We also provide a forum for industry policy and professional development. SIFMA, with offices in New York and Washington, D.C., is the U.S. regional member of the Global Financial Markets Association (GFMA).

BestEx Research Launches AMS One, Enabling Banks and Brokers to Build Algorithmic Execution Businesses Across Global Equities and Futures Markets in a Single, End-to-End Platform

June 11, 2026

STAMFORD, Conn., June 11, 2026 /PRNewswire/ — BestEx Research Group LLC, an independent provider of high-performance algorithmic execution and trading analytics, today announced the launch of AMS One, an end-to-end algorithmic trading platform that allows banks and brokers to build and run their own execution business across global equities and futures markets.

AMS One provides a plug-and-play trading infrastructure that enables banks and brokers to compete with tier-one institutions, bringing together the four components necessary to run a competitive algorithmic execution enterprise. The platform includes high-performance execution algorithms, the tools required to build branded algorithms and tailor them to each client’s objectives, a fully integrated transaction cost analytics module that supports execution consulting, and a consistent experience across global markets and all asset classes traded. AMS One spans equities in the US, Canada, Europe (15 markets), and APAC (4 markets), plus futures contracts across 21 global exchanges, so platform users can launch and grow their business from day one.

“Our clients aren’t looking to buy software. They’re trying to build a business that wins and attracts more order flow,” said Hitesh Mittal, Founder and CEO of BestEx Research. “Most vendors in this space are software companies that focus only on the technology side of electronic trading and leave market structure and product design unattended. The result is execution that doesn’t match what a tier-one institution would deliver, and clients are left to maintain the infrastructure themselves. We built AMS One so banks and brokers get everything they need in one fully managed platform, without the eight-figure build.”

AMS One pairs global reach with depth in every module. Strategy Studio, a no-code customization tool, provides over 150 configurable parameters that govern every decision an algorithm makes, controlling how it schedules and places an order, manages urgency, adapts when ahead or behind schedule, and handles volume constraints and order completion. That gives desks granular control at every level of execution. The platform also delivers the industry’s first fully flexible smart order routing infrastructure, with control over venue selection and prioritization, order types, pegging logic, resting duration, and refresh behavior, whether an order is passive, hidden, dark, or conditional. Strategies can be tailored to individual clients and assigned in a few clicks, or built from scratch with differentiated intellectual property and rolled out as custom, branded algorithms.

“Our clients will be judged by the fills they provide, not the platform behind them, so we built AMS One to be the platform our sell-side clients would aspire to build themselves,” said Nigam Saraiya, Chief Product Officer of BestEx Research. “It is grounded in algorithmic trading expertise, with market structure at its core, and supported by robust technology written in C++ and co-located globally, so our clients don’t have to compromise on performance.”

The platform is built to support a large buy-side client base, with component modules that allow banks and brokers to exceed client expectations with the level of service they provide. Real-time monitoring tracks thousands of live orders at once, with configurable alerts and notifications, and lets a trader work alongside the algorithm to provide a high-touch experience to their clients. Built-in A/B testing supports comparison across strategies, and Meta Strategies automate algorithm assignment based on order characteristics as orders arrive, so each client’s orders are handled according to their specific needs. Every order rolls into the platform’s TCA module, designed by the same team that builds the algorithms, where execution quality is measured at the parent-order and fill levels and used to refine strategy.

Its predecessor, AMS, went live in 2019 and has already executed trillions in notional value for institutional investors. To schedule a demo or learn more, visitwww.bestexresearch.com/sell-side/ams. For complete market coverage, click here.

About BestEx Research

BestEx Research Group LLC provides independent, research-driven execution algorithms, trading technology, and trade analytics for equities and futures that aim to reduce trading costs for institutional investors. For more information on BestEx Research’s mission and products or request a demo, visitwww.bestexresearch.com. Connect with BestEx Research on LinkedIn.

Webull has launched a Model Context Protocol (MCP) server, enabling clients to interact with its OpenAPI using natural-language AI commands without requiring programming knowledge.

Anthony Denier, Group President and U.S. CEO of Webull, said the development reflects a broader shift in how investors access financial markets.

Anthony Denier

“The shift in market access over the past decade has consistently been about reducing friction for investors, from zero commissions to fractional trading. We see AI as the next evolution of that trajectory,” he told Traders Magazine.

Denier described MCP as part of what he called a “next interface layer” for investing, where natural language becomes the entry point into trading systems.

“MCP is part of what we would describe as the next interface layer for investing, where natural language becomes the bridge between investors and increasingly sophisticated trading infrastructure,” he said.

“The goal is accessibility, making advanced tools usable for investors who may not have the time or technical background to engage with APIs or traditional automation frameworks,” he added.

According to Denier, since its initial rollout in April, early users have been interacting with core platform functions through MCP, including market data queries, account information, position monitoring, and order execution via conversational prompts.

Denier said the early adoption has changed how users engage with trading workflows.

“What stands out is the way MCP changes how investors interact with the platform,” he said.

“Rather than navigating multiple screens or workflows, users can engage with key trading functions through a more intuitive interface that simplifies access to information and tools.”

The company emphasized that MCP is not designed to remove user oversight in trading decisions.

“MCP is designed to simplify access to trading tools, not remove investor control,” Denier said.

“Investors remain responsible for reviewing and verifying order details before execution.”

Webull said standard brokerage safeguards remain in place, including margin requirements and risk controls.

According to the company, users can also configure how MCP functions within their accounts and determine which features are enabled.

“In addition to standard account protections, margin requirements, and brokerage-level risk controls, users have the ability to configure how they interact with MCP and control which functionalities are available to them,” Denier said.

“This helps ensure investors can tailor the experience to their own preferences and risk tolerance while maintaining visibility into their trading activity.”

The firm positioned AI as a structural shift in retail investing, particularly in how investors monitor markets and manage portfolios over time.

“AI represents a structural change in how investors interact with markets,” Denier said.

“Many investors do not have the time to actively monitor markets throughout the day due to work, family, and other commitments.”

“AI enables a way to stay engaged with a portfolio in a more continuous way, without needing to be constantly in front of a screen,” he said.

“AI tools act as an always-on layer that can help investors track markets in real time. It effectively reduces the friction created by time constraints while keeping investors in control of their own decisions.”

Denier said the company views current adoption as early-stage, with use cases still evolving.

“We are still in the early stages of how these tools will be used in practice, and we expect use cases to continue evolving as adoption grows,” he said.

Webull also pointed to the challenge of balancing accessibility with transparency and control as AI becomes more embedded in trading workflows.

“The biggest challenge is balancing accessibility with transparency and control,” Denier said. “Historically, many advanced trading tools have required a significant level of technical expertise to use effectively.”

“One of our goals has been making these capabilities more accessible without sacrificing clarity around how the technology works or the actions being taken on behalf of the investor,” he added.

“As these tools become more intuitive, it’s important that investors still understand the information being presented and maintain full visibility into their account activity.”

Looking ahead, Webull said it will continue refining the MCP system and expanding availability beyond the U.S.

“Our focus is on continuing to refine the user experience and making AI-powered investing tools more accessible and intuitive for investors,” Denier said.

“We view MCP as part of a broader evolution in how investors interact with financial markets, and we will continue evaluating ways to improve functionality, usability, and the overall experience as adoption of AI tools continues to grow.”

The system is currently available to U.S. clients, with additional markets expected to follow.