By Richard Johnson, Founder & CEO, Texture Capital

The events centered around trading in Gamestock ($GME) recently highlighted some serious flaws in equity market structure. It started as an online Reddit community of retail investors called WallStreetBets sharing stock picking ideas and led to a massive short squeeze wiping out $19bn in capital across numerous hedge funds including Melvin Capital. The events that followed were even more devastating for the reputation of US equity markets as hundreds of thousands of traders were systematically prevented from additional trading in certain stocks, leaving many feeling the market is rigged against them.

Let’s take a look at what happened, and I’ll explain how, in the future, it’s possible that a tokenized securities model can provide a better solution.

The Short Squeeze

Shorting refers to the practice whereby investors who have a negative outlook on a stock want to bet that the price will go down. To do this they borrow the shares from an investor who currently owns the stock, then they sell them in the market, hoping that they can buy them back in the future at a lower price and return the borrowed shares to the investor.

What happened with Gamestop was that so many hedge funds had taken short positions that the ‘short interest’ exceeded 100% – i.e. there were more shares sold short that the total amount of shares outstanding in Gamestop (naked shorting). This is clearly a problem – how can the market sell more shares than exist? Indeed, market regulations have been designed to prevent exactly this. Reg SHO requires market participants[1] to make an affirmative determination that they can borrow shares to cover their short position by settlement date. So in theory, every share sold short is matched up to a borrowed share. However, the problem is that the Wall St banks, custodians, and the DTCC all maintain separate databases of stock lending positions that are not synced up. This can lead to a borrowed share being shorted more than once.

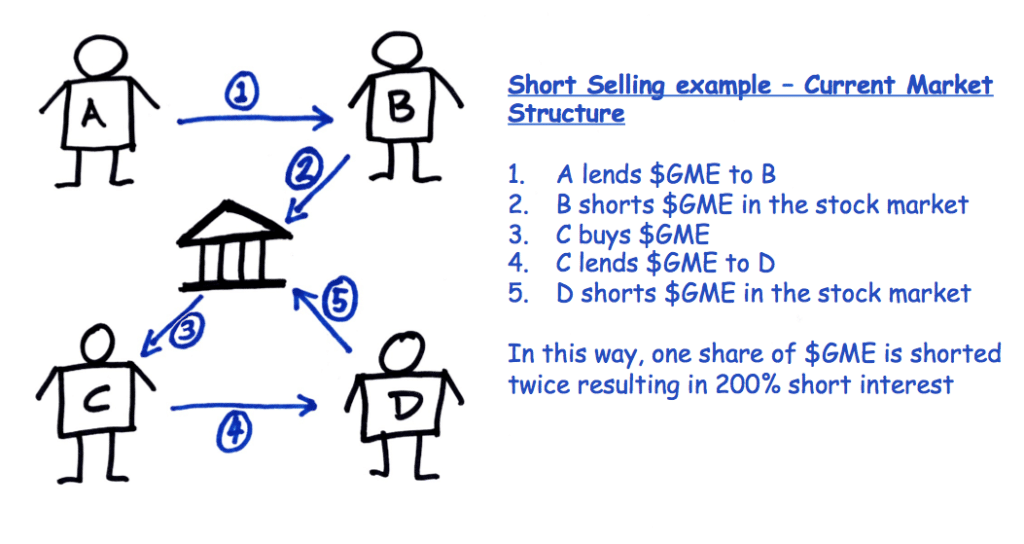

Consider this (simplified) example: Trader A lends $GME to Trader B who sells short to Trader C. Trader C now lends $GME to another Trader D who sells it short again.

This is how we can end up with short interest greater than 100%. And when the WallStreetBets traders, started buying $GME pushing the price up, hedge funds were forced to cover their short positions by buying back $GME stock further pushing the price up and so on. This is what is called a short squeeze.

How Tokenization Would Fix Naked Shorting

Recent innovations in DeFi (Decentralized Finance) have demonstrated the potential for tokenized solutions to provide a better market structure. Decentralized lending protocols, such as Maker and Compound provide an example of a new approach. With these DeFi protocols, participants can take out a loan by depositing a crypto-token as collateral. For example, in the case of Maker, the $ETH is deposited and locked up in the smart contract, and the stablecoin $DAI is borrowed at some rate of interest.

With tokenized securities, we can take this example and build a better system to stock lending and shorting. Security tokens (securities recorded on blockchain) can be lent out in a similar way to the DeFi protocols described above. The security token would be locked up in the smart contract and held as collateral for a margin loan. In this kind of model, the distributed blockchain ledger would represent a shared ‘source of truth’ of securities ownership and transaction history. And the lending protocol itself, when developed, would be able to programmatically prevent the security token from being lent out more than once. Naked shorting could be easily prevented in a tokenized system.

Clearing & Settlement

In the second half of the week, popular online brokerages started preventing their customers from adding to their positions in Gamestop and other affected securities. Many folks decried this as unfair discrimination of smaller retail traders to protect the hedge fund fat cats. The reality has nothing to do with class warfare and everything to do with the antiquated plumbing underpinning today’s equity markets.

Today, nearly all trades of equity securities flow through the DTCC and are settled delivery-vs-payment (DVP) within two business days. This means that shares are not delivered to the buyer, and payment is not delivered to the seller until two days after the trade takes place. Now, if the buyer doesn’t have the money to pay for the shares they purchased the trade could fail. And if the seller doesn’t receive the money they were expecting from the trade, they may be unable to pay for other securities they have purchased… and so a cascading knock-on effect could occur, causing trade fails through the system. To mitigate this, the DTCC requires member firms to post collateral to cover settlement through the two-day cycle. The collateral calculation is based on the notional value of trades to settle and their volatility.

Tying this into the events of last week, as $GME was so volatile and there was so much activity in the stock, the risk and impact of a failed trade increased sharply, causing the DTCC to increase collateral requirements for this stock and certain others. This jacked up costs for online brokers who cut off new trading in these names to avoid paying higher collateral obligations.

How Tokenization Would Fix the Settlement Cycle

In tokenized markets it’s not just the securities that are tokenized, but also the payment asset. There exist already a number of ‘stablecoins’ – these are tokens that are recorded on blockchain and are pegged to the US dollar on a 1:1 basis. (Additionally, the Digital Dollar Project[2] seeks to drive forward a Federal Reserve backed U.S. dollar token).

With both securities and cash represented on a distributed blockchain ledger, DVP settlement would take place instantaneously in between buyer and seller directly rather than relying on a centralized clearing counterparty. An investor who wishes to sell their securities would submit them to a trading engine smart contract. Similarly, a potential buyer would submit cash, as a stablecoin, to the trading engine smart contract. Should a trade occur, the smart contract would instantly and automatically transfer shares to the buyer and payment to the seller.

In this way, we believe, it is possible to build a market that enables real time gross settlement without the need for centralized clearing and the associated collateral requirements that stymied the market last week. In the Gamestop scenario, this means brokers wouldn’t have had to restrict trading to manage risk through the settlement cycle, because settlement would have been instantaneous.

Final Thoughts

This commentary has described a new market structure leveraging blockchain and tokenized securities – this is a vision that firms like Texture Capital are striving to build in private markets. This won’t happen overnight, and it is important to note that retro-fitting today’s public equity markets would likely not be a viable solution – legacy technologies, intermediaries, and business processes are too ingrained to simply be swapped out. (The Australian Stock Exchange (ASX) if an informative example, here; they began the project for a DLT settlement system back in 2016 and go-live is now delayed until 2023.) In addition, a tokenized marketplace may introduce other, new risks into market structure, that will need to be mitigated (consider, for example, the numerous hacks and errors in DeFi that have costs investors millions of dollars in lost capital).

As described here, we believe a tokenized securities model offers a new way of designing market structure. This is not the complete picture though; to fully rebuild markets using this technology, there are many other processes and mechanisms that will need to be re-designed. We are still in the very early innings of the transformation, but the pieces are beginning to fall into place; broker-dealers and ATSs that specialize in tokenization are coming to market; the SEC, after a period of cautious examination, are becoming more open to this technology; and now, an unlikely Reddit user group has highlighted the need for ongoing innovation within capital markets.

[1] Except market makers

[2] https://www.digitaldollarproject.org/